“China is a big country, inhabited by many Chinese.”

— Charles de Gaulle

Prefer to read today’s QuiCQ in PDF? No prob, download it here, but don’t you dare complain about the formatting!

Chinese (equity) marktes remain closed in observation of their National Holiday(s), however, we have a proxy via the Hong Kong market, where the Hang Seng index finally put in a second negative day since the announcement of the stimulus bazooka eleven sessions ago. Still, two percent down after 30% is not too shabby …

And, observing that long lower shadow on the last candle we note that the HSI is already up three percent from intraday lows … who knows where it will end with still two hours to go in the today’s session.

In Europe and Wall Street markets closed flat yesterday, with little macro news to move the market. This probably ahead of today’s jobless claims and ISM number in the US, but especially in expectation of tomorrow’s non-farm payroll (NFP).

Four out of the eleven sectors closed higher, with Energy (+1.1%) leading and Consumer Staples (-0.8%) lagging. The number of stocks advancing and those declining on the day was pretty even, though 34 stocks reached a new 52-week high, whilst only four hit a new one year low.

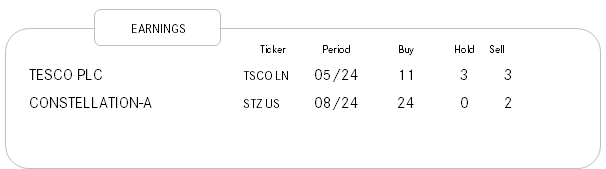

Corporate news titled to the negative side, with Conagara, Nike and Humana all dropping heavily (see laggards table above) after their earnings respective trading updates.

Oil continues to be a focus of course. With the black gold off its intraday highs of yesterday, the geopolitical premium is at danger of getting wider over the coming days, depending on Israel’s retaliation to Iran’s recent attacks.

The US Dollar is another macro instrument (safe haven) where these geopolitical fears are expressed. The Greenback (DXY) now trades at its highest since mid-August and very clearly off its key support just above 100 we were so closely watching.

The below is just one of many fascinating charts NPB’s Q4 outlook will offer you as TAA and accompanying chartbook are released tomorrow Friday or latest Monday.

It shows you all equity market years (via the S&P 500) since the turn of the Millennia (grey lines), the “average path” (black line) and this year’s development (red line). Ergo, as per the end of September, the stock market has seen its best first nine month of the past 25 years …