QuiCQ 05/09/2024

Happy Birthday to the youngest Princess of the clan

“We should not confuse information with knowledge.”

- T.S. Eliot

Prefer to read today’s QuiCQ in PDF?

Yesterday’s investors focus was rather on the macro landscape and the (interest) rate environment, rather then the stock market. The S&P closed ever so slightly in the red, but 6 out of 11 sectors closed higher and the number of advancing stocks was equal to the one of declining stocks. The 22% drop in Dollar Tree, a US discount retails, caught our attention, as it implies that the poorer xx% (fill in your own number) of US households is suffering.

Rates were clearly the focus, especially after the JOLTS opening report was substantially weaker-than-expected. Even though it is a volatile and outdated (July) datapoint, it was enough to increase expectations for a 50 bp FOMC rate hike in September higher and push the short end of the curve lower, which in turn lead finally to the “uninversion” of the yield curve, some 793 days later.

Another focus in yesterday’s session were currencies, with the US Dollar falling against all other G-10 currencies. But especially the Yen strength (+1.4% vs. the Greenback) caught our indication, indicating the carry trade unwind is maybe not fully completed.

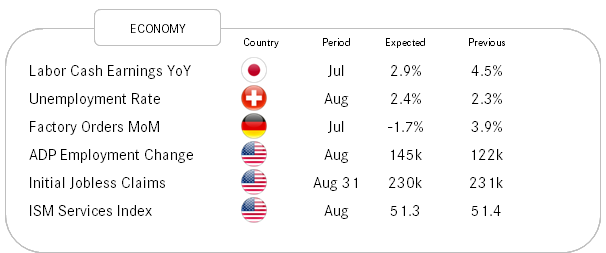

Today Jobless Claims and tomorrow Non-farm Payrolls (NFP), both in the US, will be focus.

A less than two minutes read and you know it all! Have a great day!

The yield curve has “uninverted”. Unfortunately, in the past, “uninversions” were shortly after followed by recessions. Caveat: The recessions were only officially declared ex-post. Implications for equities? To be discussed in another QuiCQ (or Quotedian)…