QuiCQ 10/04/2025

Just Kidding

"I used to think that if there was reincarnation, I wanted to come back as POTUS or the Pope or a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody."

— James Carville, 1994

Enjoying The QuiCQ but not yet signed up for The Quotedian? What are you waiting for?!!

This early on in yesterday’s session:

This a few hours later:

I wonder, can a US president be impeached for insider trading?

Probably not, but even worse, he most likely even brag about having called the market bottom. Sigh.

But everybody else knows the truth. And the truth is, that he and his partner-in-crime Scott Bessent had their James Carville moment. The two intimidating charts we discussed in yesterday’s QuiCQ were:

The sudden sharp increase in 10-year bond yields:

The massive widening in the 30-year Swap to the 30-year Treasury spread:

Speaking to clients, partners, friends & family over the past days we always highlighted how binary the situation remains: Stick to tariffs, we might jump of that proverbial economic cliff - pivot through a “just kidding” moment and everything could be pretty ‘fine’ again in due course.

So, now we’ve got:

Trump’s Tariff Tantrum Turnaround™ (TTTT™)

Onward with a market speed round …

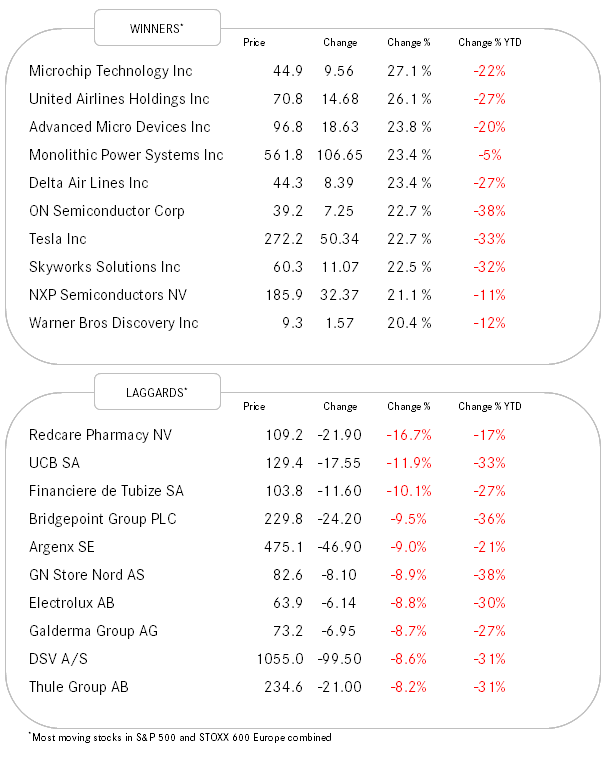

You can take the equity index moves from the table in the ‘Quotes’ section, but one thing I would like to highlight is that even with yesterday’s one-day double-digit rally, NONE of the trend arrows has changed.

Nevertheless, yesterday was probably the day we got A bottom. If it is THE bottom needs to be seen, but for the next few sessions we should get follow-through.

Market breadth was ridicousely one sided, with 9 out of the S&P’s 503 stocks down:

Or only one down in the Nasdaq 100:

Or less than 2% lower on the day in the Russell 2000:

You get the point.

On the fixed income side of matters, predictably enough, yields came down, though not quite to the extent that Scotty was hoping for probably:

Credit spreads relaxed a tad, but just a tad:

This will probably be an interesting chart to follow, to track how much damage the market assumes was done and how avoidable a recession remains.

Here’s something that surprised me this morning:

The US Dollar is currently continuing to weaken versus all other G10 currencies… Alright, it came of its lows yesterday, but currently Greenback sellers have the overhand again. Here’s the Dollar Index (DXY):

Gold is another mild surprise to me, especially the extent of the short-term reaction:

My best guess here is that markets are profoundly distrusting the path the global economy/geopolitics have embarked on - with the most recent twists and turns increasing insecurity even further. Stay long here - maybe even very long.

Oil rallied four percent on yesterday’s TTTT™:

Too much to cover and it’s time to hit the send button…

…. but, ah yes, just in case anybody still cares … US inflation numbers (CPI) are out this afternoon. Just saying …

“Markets are on fire, and so is my calendar. I’m long VIX, short MS Outlook.” - have a great day.