QuiCQ 10/07/2025

Certainly Uncertain

“The necessity of making decisions in the face of uncertainty is the essence of investment.”

— Peter Bernstein

Enjoying The QuiCQ but not yet signed up for The Quotedian? What are you waiting for?!!

NEW! NEW! NEW! NEW! NEW! NEW! NEW! NEW! NEW! NEW! NEW! NEW!

Your favourite daily newsletter now presented to you personally by Avandré:

First one to laugh gets excluded from the list!!

I know, I know, I will improve on picture, facial expression and voice over the coming issues … a start is a start. (OMG)

In a way, President Trump is doing everything human-possible to make NPB’s Q3 outlook, which focuses on capital moving to where it is treated well and exoUSD, be absolutely relevant.

The latest aired episode of the popular TTT (Trump Tariff Tantrum) series, included a heap of new countries threatened with tariffs, where the unexpected twist in this soap opera came with the protagonists ex girlfriend in Brazil. Trump threatened to impose a 50% tariff on the country, with which it has a trade SURPLUS, due to “insidious attacks on Free Elections, and the fundamental Free Speech Rights of Americans.”. Of course, this is a hint to his latin lover Bolsonaro and him being prosecuted. Using tariffs now as political blackmail instruments are a new and not very ‘good’ turn in the storyline. The “death by a thousand (self-inflicted) cuts” continues …

But, onwards!

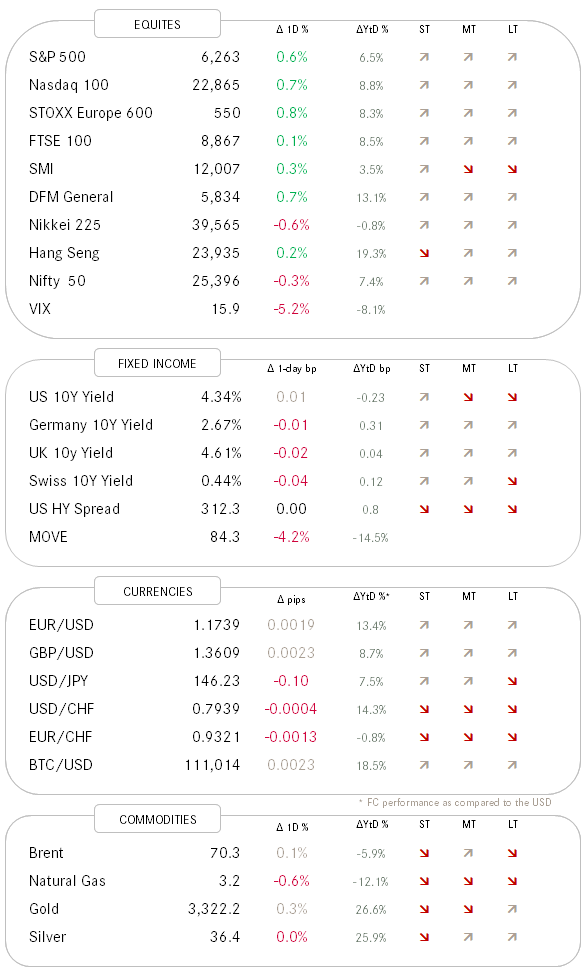

The equity market, in good old fashion, did not care, but rather showed solid gains by the end of the session, with major indices missing new all-time highs only by a few points. Up-down ratio was 3:2 for the S&P with eight out of eleven sectors closing up on the session:

The heatmap above reveals that some of the index champions did the heavy lifting in yesterday’s session, with of course NVDA briefly reaching as first company ever that USD 4 trillion market cap level (have achieve USD 1 trillion only two years ago):

How long it take for the company to reach USD 10 trillion? My guess is by 2029. Post your guess in the comments section:

One market segment that made a new cycle high yesterday were small cap stocks. Our call from a week or two ago to overweight the Russell 2000 is starting to pay off well:

As a segue into the rate/fixed income comments section, we should highlight that the FOMC minutes were released yesterday. As Yardeni research writes in their daily note today:

At the end of last year, the words "uncertain" and "uncertainty" appeared 12 times in the minutes of the December 17-18 meeting of the Federal Open Market Committee. Those words appeared more often during this year's meetings. The June 17-18 meeting minutes released today included those words 28 times. During his presser, Fed Chair Jerome Powell mentioned the two words 19 times.

More to our point of capital will flow where it is treated well or, in other words, where uncertainty is less elevated than in other places …

Anyway, the rest of the FOMC were clear as mud, showing the confusion amongst its members. Many saw two to three cuts this year, some as early as July, others none at all, everbody citing the aforementioned uncertainity regarding the impact and the timing of the impact of tariffs on inflation.

Nevertheless, bonds rallied quite hard (10-year yields -9 bp), though as the intraday chart shows, NOT due or at the time of the release of the FOMC minutes:

The Dollar softened versus other G10 currencies, probably on the back of lower bond yields:

Ok, enough for today - May the trend be with you!

With all that is going on in the world at moment, and I agree, it does “feel different this time”, there is always something to worry about. I found the infograph below an interesting and useful reminder that there have been constant excuses over the past 30 years NOT to be invested. Pick your favourite:

And yet, somehow, despite all of it, the market kept moving forward over those 30 years. The S&P 500 index returned +608% cumulatively since July 9, 1995. That’s 9.2% annualized.

Stay tuned (and invested)!