QuiCQ 12/02/2025

BAG7 ?

“Expect the best, plan for the worst, and prepare to be surprised.”

— Denis Waitley

Enjoying The QuiCQ but not yet signed up for The Quotedian? What are you waiting for?!!

A two points close higher on the S&P 500, which equals +0.03% and does not even register on our “The Quotes” table above, is about all you need to know regarding yesterday’s session. I could also tell you that the number of stocks up was about equal to that of those down, or that 8 out of 11 sectors closed higher, but I won’t …

Much more exciting however is the session this morning over in Asia, especially if you happen to trade Hong Kong listed stocks. The Hang Seng Index, missed the technical definition of a bear market (>-20%) from October to mid-January by less than half a percentage point, but since finding a bottom is now up nearly 17%:

Especially since the “Deepseek”-moment has the trend been accelerating to the upside. We shall have a closer look in next week’s ‘The Quotedian’.

Other Asian markets are less exciting, with Japan and Mainland China small up and India small down.

US (10y) yield pushed higher again yesterday, trading at 4.54 as I type. A prepared and preleased Powell speech to Congress had him reiterating that there was no rush to cut rates further.

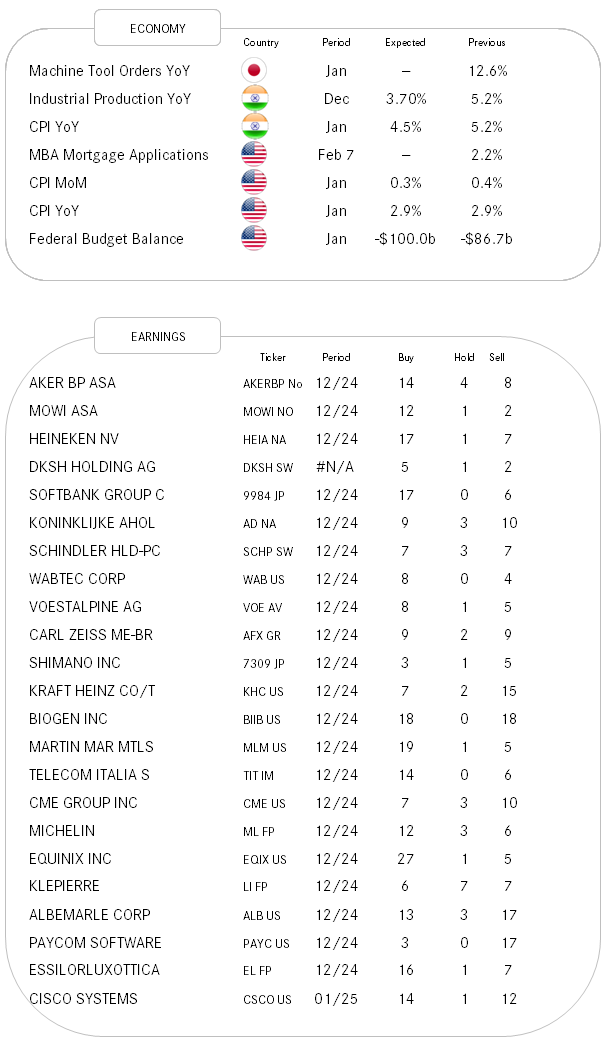

Which in turn of course increases focus on today’s release of the US inflation (CPI) number even further. Here are the estimates of 61 ““““Qualified Economists””””:

In currencies, the only noteworthy movement over the past hours came out of the USD/JPY cross, where the Japanese currency had been lower for two consecutive sessions but is seeing an acceleration of the downtrend this early Wednesday, as fears that Japan may be hit with US levies outweigh the 5-year JGB yield hitting 1%, its highest level since 2008:

Gold has (finally) corrected somewhat from recent all-time highs and is trading below $2,900 again.

That’s all we need to know - time to go.

The fine folks at JPM published a great chart a few days ago, showing how the period of MAG7 earnings growth dominating the S&P 500 has almost ended.

Is the relative underperformance of the Mag 7 (red) versus the entire S&P 500 (grey) to continue?

BAG 7 anyone?