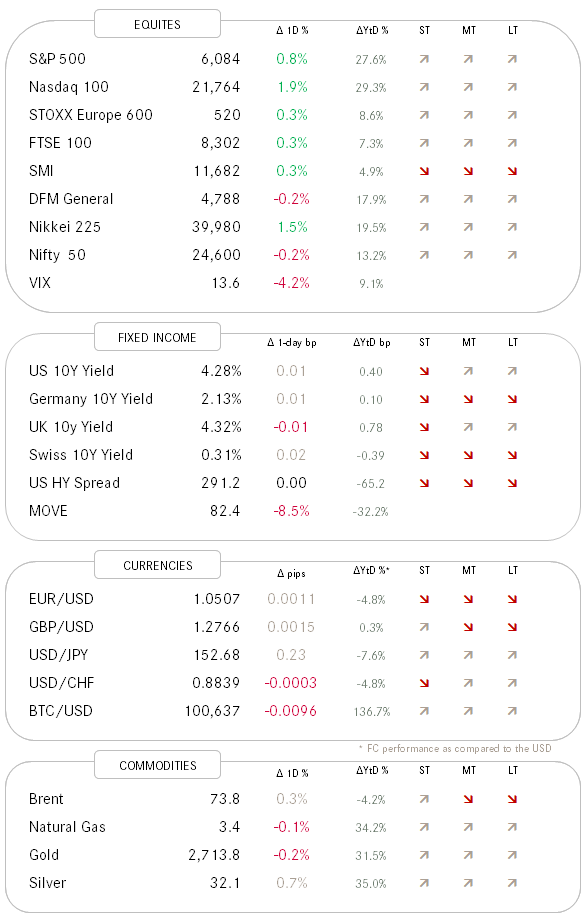

QuiCQ 12+12=24

Roaring 20s

"The GDP growth next year will be 3.276%, give or take 5%."

— Anonymous

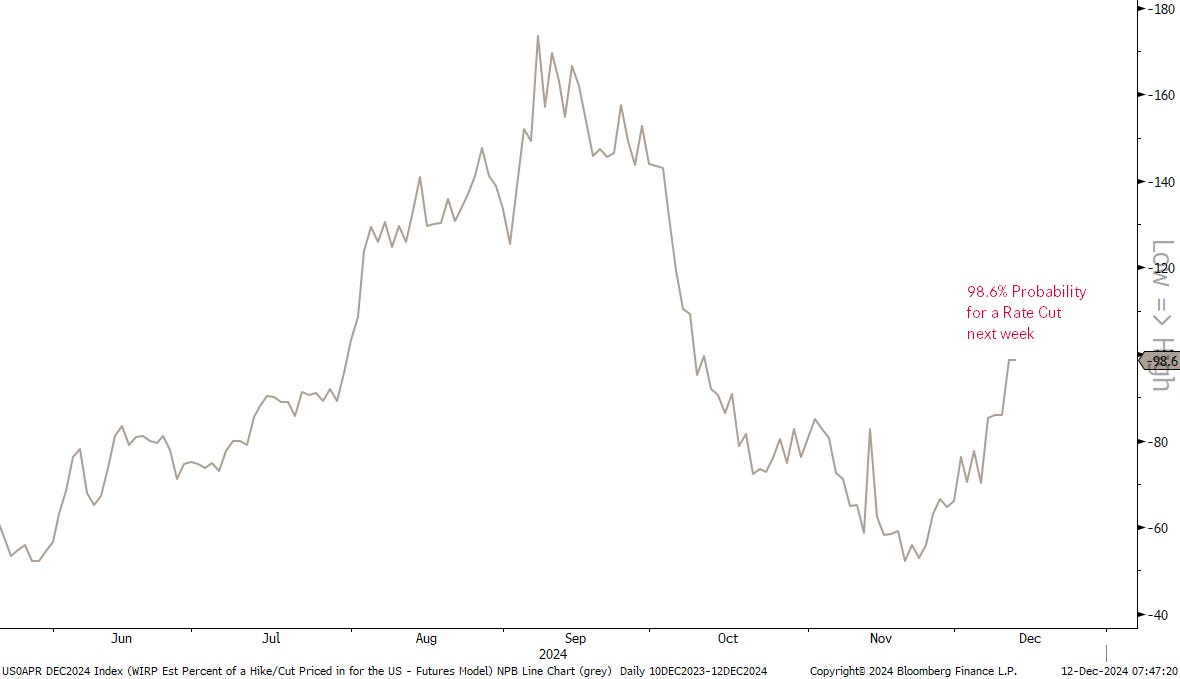

Yesterday’s session was all about the US inflation number (CPI), which, asides of being a joke anyway, turned out to be quite the non-event. The number was being bang on in-line with expectations, but observing it to a couple of digits to the right after the comma (hence today’s QOTD), a tad higher.

However, this tad higher, yet below whisper numbers, is likely to be ignored by the market and the Fed, and indeed have the probabilities for a FOMC rate cut next week increased to close to 100%:

Talking of rate cuts, the SNB is due to communicate their decision, and it is widely expected that new Martin Schlegel will cut by 25 bp at his first meeting as president. And still talking of rate cuts, the ECB is also due to communicate their monetary policy decision at lunchtime, where again it smells of one 25 bp cut:

Equity markets cheered the CPI number (and the implied rate cut) in the US yesterday, with especially the broad Nasdaq Composite (3284 members as compared to the Nasdaq 100) advancing meaningfully, moving and closing above 20,000 for a first time ever:

The S&P was also up a decent 0.8%, however, the number between advancing and declining stocks was balanced at best. Yet, this should not be of worry, or rather, after last weeks five sessions of more losers than winners, consider a breadth improvement.

Bond yields expressed a slight concern about the prospects of another rate cut next week, by moving higher, with 10-year US breakevens moving six basis points higher, lifting the nominal 10-year US treasury yield to above 4.28% this morning:

In such a scenario, stock up, bonds down as a function reaction to the inflation number, one could imagine for the Dollar to get very confused. Indeed:

Gold on the other hand, broke higher, and price behaviour is starting to challenge my call for no new all-time highs before the January 20th presidential inauguration:

Today, the forementioned central bank decisions and PPI in the US. After market close, focus list company Broadcom (AVGO) will be reporting.

We all have seen these “if history repeats” overlay charts, where the current period is compared to a previous period. Normally, these are doomsdayers charts where the overlay suggests that a imminent crash (aka “end of the world”) lays ahead.

Well, I have found a much more pleasant one, that compares the roaring 20’s a hundred years ago to the roaring 20’s nowadays. I have long been saying that the introduction of ChatGPT to the world is comparable to the introducing of Netscape (that was the first useful web-browser, for the younger folks out there) in 1994. What ensued was a wild six to seven year rally into the bubble top in 2000:

Different explanations, same outcome. Enjoy, will it lasts!