QuiCQ 13/12/2024

Tired Edition

"Superstition is the poetry of life."

— Johann Wolfgang von Goethe

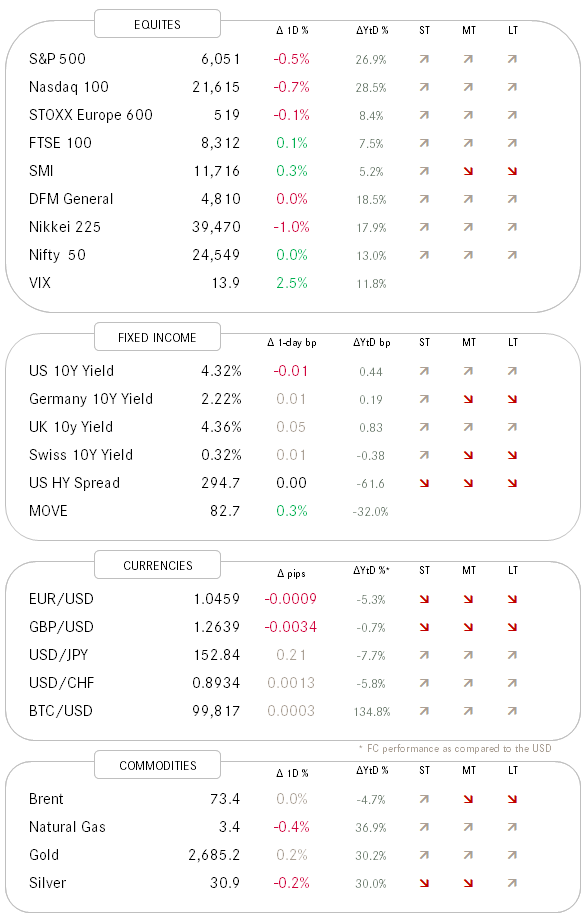

Yesterday’s session was very much influenced by macro factors. During the morning session, and within a short time span, the central bank of Brazil increased their key policy rate (Selic) by one percent and the SNB surprised with a 50 basis point cut:

It was the best of times, it was the worst of times …

The ECB followed a few hours later with a 25 basis point cut, much inline with expectations.

And yet a little later US Producer Price numbers (PPI) were reported, which came in a tad hotter warmer than expected, provoking an negative undertone for the US equity session.

Stocks closed lower on the day, with the Dow producing its sixth consecutive negative daily candle:

Worrisome?

Not at all, when we glance over at the S&P 500, which is 0.6% away from a new all-time high:

Breadth continues to be weak, though as mentioned on other occasions, it is more than normal for a market to take a breather after the strong advances we have seen since early November (and the beginning of the year…).

Rates, as could be expected post the higher-than-expected PPI reading, moved higher, with the US 10-Year Treasury yield above 4.30% again:

Which means the US Dollar was annoyingly strong also, moving up for a sixth consecutive session as measured by the Dollar Index (DXY):

At least it helped the SNB additionally to weaken the Swiss Franc:

Little more to report today. Have a great weekend!

They say that nobody rings a bell at the top of market:

Yesterday, President-to-be-(again) rang the opening bell on the NYSE in celebration of him having been chosen as Time Magazine’s “Person of the Year”.

Maybe, just maybe, sometimes somebody DOES ring a bell at the top?

(Spoiler Alert: Probably not)