QuiCQ 14/08/2024

Much ado about notin'

Welcome to the new, upgraded version of The QuiCQ, your daily dose of market commentary, witty quotes and interesting charts. Like it? Hit the like button and leave a comment. Hate it? No hate button to hit, but leave your comment.

Prefer to read today’s QuiCQ in PDF format? No prob, download it here!

"A statistician is someone who can draw a straight line from an unwarranted assumption to a foregone conclusion."

-- Anonymous

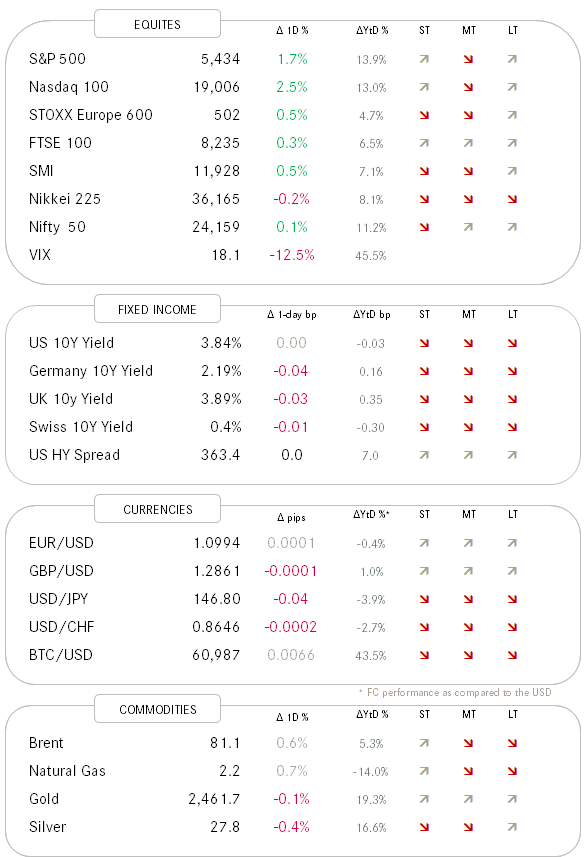

If Shakespear were still alive and he would have turned a financial market commentator, he probably would title his current piece "Much ado about nothing". Stock markets continued to recover from their slump of the past two weeks, as if nothing ever happened – which may actually be the case. Whilst the whole world and its mother are waiting for the US CPI release today, yesterday's PPI number came in softer than expected, heightening market expectations for a softer consumer inflation number too. 14:30 CET will tell. In the meantime, the S&P 500 1.7%, whilst the Nasdaq dashed 2.5 higher. US yields (10y) softened more than 8 bps to a low of 3.83%, whilst the USD also weakened 70 pips to briefly hit the 1.10 level versus the EUR.

Mixed performance numbers in Asia this morning, with Australia up, the Chinese equity complex generally a tad lower and Japan unchanged, after PM Kishida announced he would be stepping down.

In corporate news, the change of Chipotle's (CMG -7.5%) CEO to become Starbucks (SBUX +24.5%) new captain is noteworthy, as is UBS Group's reporting of an expectation smashing USD1.14 billion profit. A possible Google breakup should also get some further attention.

Besides US inflation numbers, we also get CPI in the UK and GDP for the Eurozone.

Today's Chart of the Day is probably a curve ball to many here. Stock market liquidity, in the form of share buybacks is about to become very supportive. As today's graphs shows, despite the late summer, early autumn bad reputation for stock markets, it is actually were most money is spent on share buybacks. Goldman Sachs estimates that close to USD 5 billion of daily purchasing will take place until the current window closes on September 6th.