QuiCQ 14/11/2024

It came, saw and left

“It’s easy to lie with statistics. It’s hard to tell the truth without statistics.”

— Andrejs Dunkels

The (US) CPI number came, saw and left, with the market largely ignoring it across all asset classes. I would continue to look out for signs of pick-up in inflation as it is likely THE Achilles tendon for the bond AND the equity market…

To yesterday’s session, where stocks closed more or less flat (SPX slightly up, NDX slightly down), but as a look under the hood would reveal, was actually a solid win for the bulls. The ratio of stocks hitting new highs versus those hitting new lows (52 weeks) was well above 5:1, even though stocks up versus stocks down on the day was a tad more balanced. Eight out of eleven sectors closed in the green.

Bond yields dropped initially over relief that the CPI number did not come in above expectations, but subsequently climbed to new multi-month high (4.48% for the Tens) on increased evidence that inflation numbers have stopped going down and have plateaued at a substantially higher level than the past few decades.

The greenback meanwhile continued its seemingly unstoppable march higher, with the EUR/USD cross hitting its lowest level since October of last year.

Bitcoin hit a new ATH at 93,425 yesterday, before sharply reversing and now trading below the 90k level again. In the meantime, Gold broke key support at 2,600 as we suggested it would in Monday’s Quotedian (click here) and is rapidly approaching our first target level around 2,400.

Asian equity markets are largely printing red this morning, with the biggest losses coming out of the Chinese equity complex. Index futures point to a softer start to over here in Europe and later on the other side of the Atlantic.

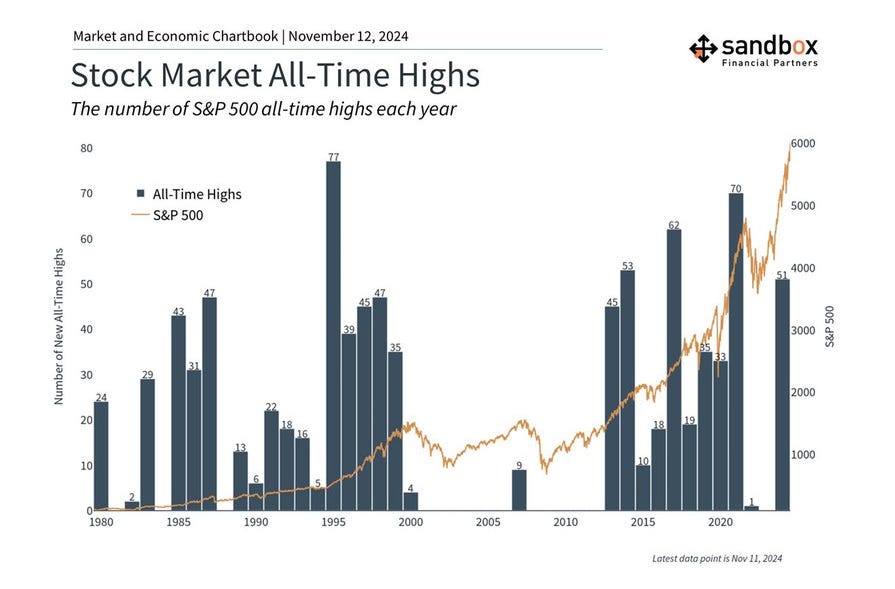

The following chart shows how many times the S&P has hit a new-all time high in any given year:

Since 1980, only four years (1995, 2014, 2017, 2021) have since a higher number of ATH than 2024. What were the full-year returns in the subsequent years to those record years?

1996: +23%

2015: +1%

2018: -4%

2022: -18%