"He who will not change his opinion will soon be without change."

— W.D. Gann

Prefer to read today’s QuiCQ in PDF? Download here:

Keeping today’s note out of necessity short, yesterday’s session was about two matters:

First, Dutch chip manufacturing leader ASML, reported earnings a day early by error (or not), showing that their order book was only about half of what analysts had been expecting. So, just as the entire semiconductor segment got started moving higher again, with NVDA for example a new ATH yesterday, this was a major sticks in the wheel, with the Philadelphia Semiconductor index for example falling by 5%. ASML itself was down more than 16% on the day.

This shaped most of the equity session, as it lead to a general risk off move into the most speculative corners of the market. Nevertheless, despite the S&P’s three quarter of a percentage point drop, the advance-decline ratio was 1:1 and five out of eleven sectors still closed in the green. Also, 56 stocks hit a new 52-week high, versus ‘only’ 17 a new 52-week low.

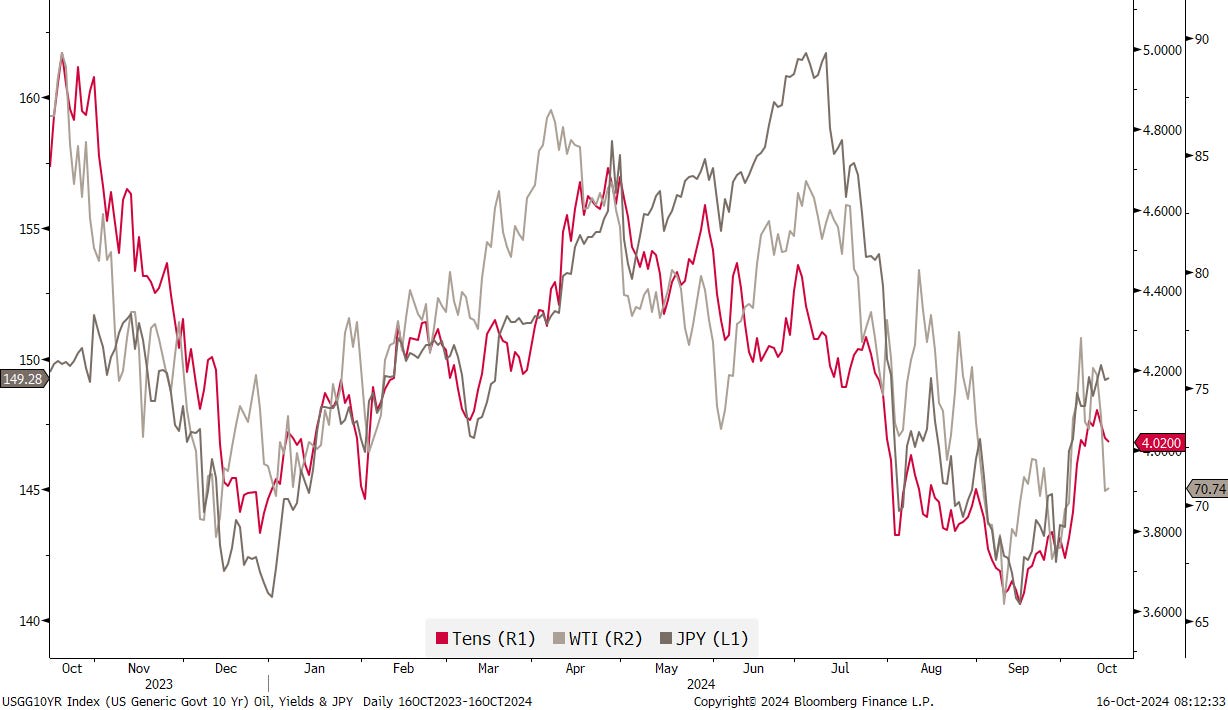

The second major theme of yesterday’s session was oil, which saw its price slump by more than 4% (on the back of Monday’s already 2%), in a mix of disappointment regarding further China stimulus and further ‘relaxation’ of tensions in the Middle East.

Global bond yields followed the oil price lower, also helped by a weaker-than-expected Empire Manufacturing reading out of the US. The following chart, consider it a “freebie” #2 chart of the day, shows the recent relationship between crude, us yields and the USD/JPY cross;

It’s all in the macro!

Have a great day.

Here’s another way for us pragmatic optimists to look at the markets “expensiveness”. Checking in on the S&P 500, we note that the index is 19% cheaper since 2021, whilst it has risen 40% over the same time period:

Et voila!