QuiCQ 20/09/2024

Superlatives

“I like long walks, especially when they are taken by people who annoy me.”

— Fred Allen

Prefer to read today’s QuiCQ in PDF? No prob, download it here, but don’t you dare complain about the formatting!

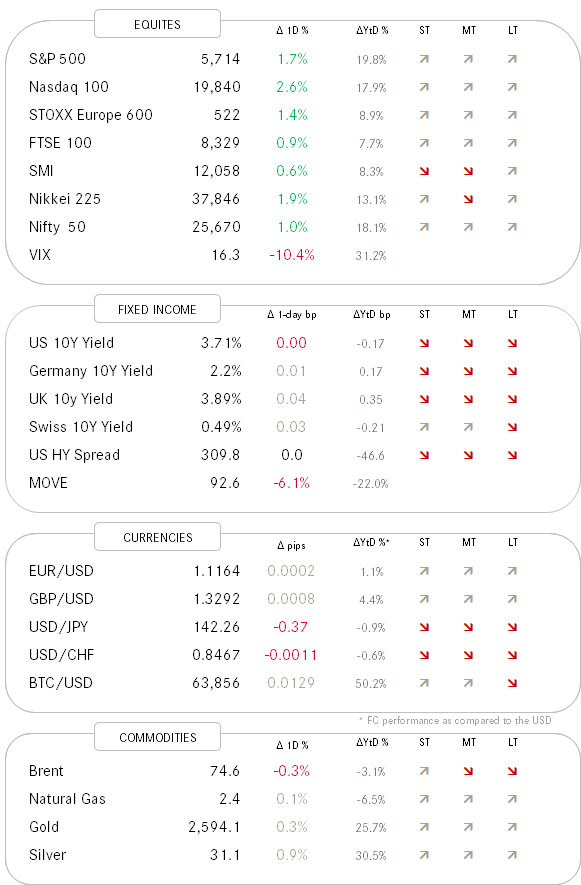

After Wednesday’s post-FOMC initial digesting phase for stocks, not unakin to your mother telling you not to jump into the pool/lake/sea right after lunch, Thursday was a day of superlatives for equity markets.

The S&P 500 opened up 1.7% higher, marking its second-largest opening gap in history (the largest was on November 9th, 2020 after the release of data showing the Covid vaccine was effective, in case you wondered). Of course, the index also closed at a new all-time high, as the cumulative advance-decline ratio had been suggested (we discussed it here).

In the Nasdaq the up down ratio was close to 6-to-1 and singling out the tech sector within that, 96% of tech stocks where higher on the day.

European equity markets, for once, where able to maintain Wall Street’s pace.

In the interest rate complex, US short-term yields (2y) softened, whilst the longer end of the curve (10y) remained unchanged, leading to a steepening of the curve.

The most important news this morning is the BoJ’s decision to stand put on their current monetary policy, in another sign that they too, are fearful of the wrath of equity markets …

(a bit dramatic I know, but it’s Friday for me too).

Anyhow, Asian stock markets, led by the Japan, are applauding this decision this morning, with most indices printing a bright green. Exception are Chinese mainland stocks, which are retreating about two thirds of a percentage point.

Have a great weekend!

Not only did the S&P 500 (large cap stocks) hit a new all-time high (top clip), but so did the S&P 400 (middle clip). And as we are it, small cap stocks as measured by the S&P 600 (bottom clip) are only 0.4% away from achieving this feat too.

Broadening out rally anyone?