QuiCQ 23/05/2024

MOVE on

Prefer to read today’s QuiCQ in PDF format? No prob, download it here!

"Stocks are stories, bonds are math."

-- David Leinweber

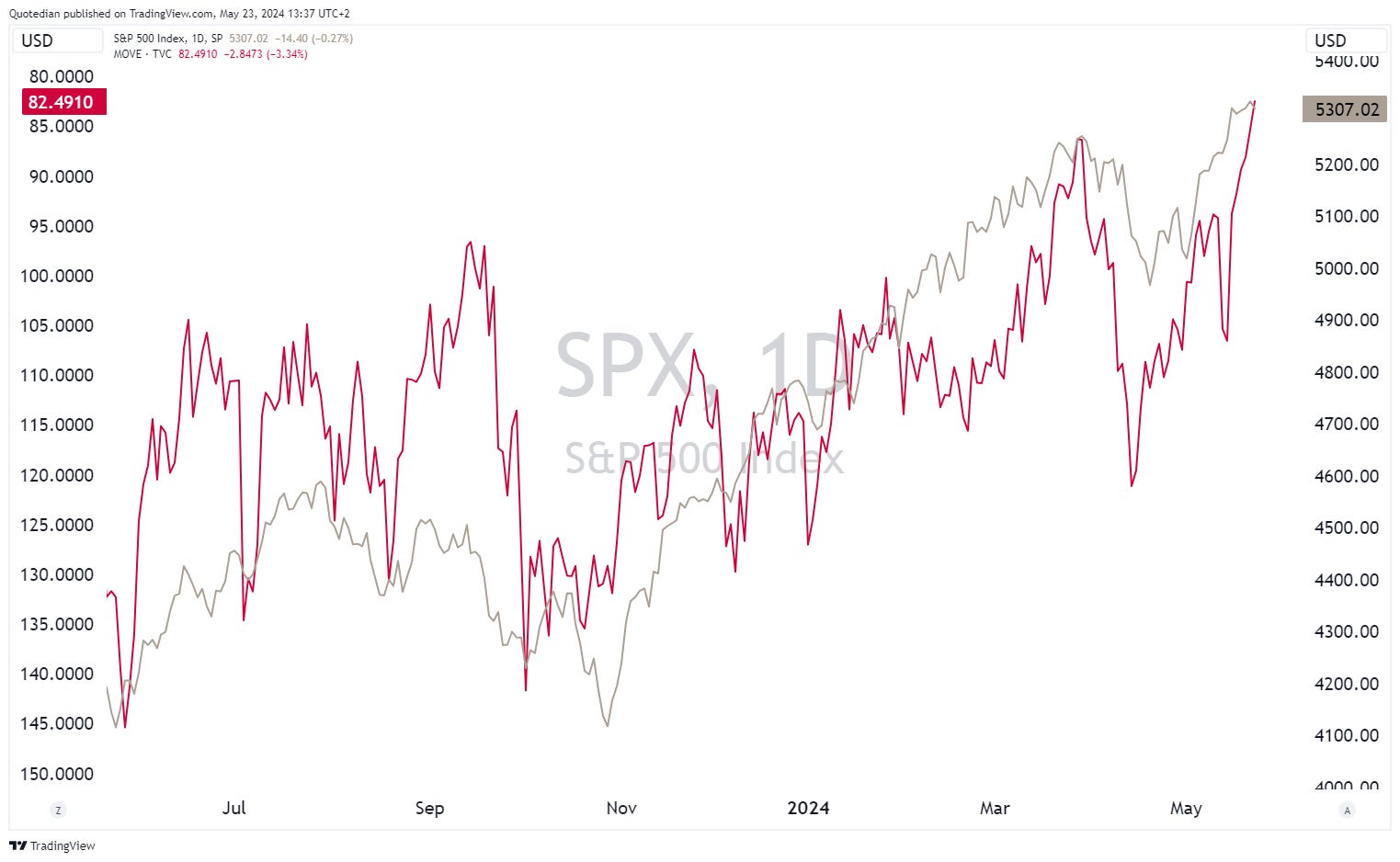

Bond yields, as proxied by the US 10-year treasury yield, shot up from the generational low at 0.50% in mid-2020 to their highest level at 5% in nearly two decades by October of last year, only to collapse below 4% again. Since then, things have started to calm down somewhat and our Q1/2024 outlook titled “muddle through” seems to come to fruition. This can be easily seen in the level of the MOVE (the VIX-equivalent for Treasury bonds volatility), which has come down from a cycle high at 180 to 82 as per yesterday.

As we show in the chart below and have often argued, stocks (S&P 500 – grey/rhs) do not care too much about the absolute level of bond yields, but more about the speed or rate of change (MOVE – red/lhs inverted). In that context, more upside in stocks seem possible from a bond volatility perspective.