QuiCQ 25/04/2024

TENANDYEN

Prefer to read today’s QuiCQ in PDF format? No prob, download it here!

"Those who use 'Correlation is not the same as causation' as a magic incantation to dismiss all fact-using professions are fools holding a lit match in one hand and an open gas can in the other, screaming, 'One has nothing to do with the other!'."

-- David Brin

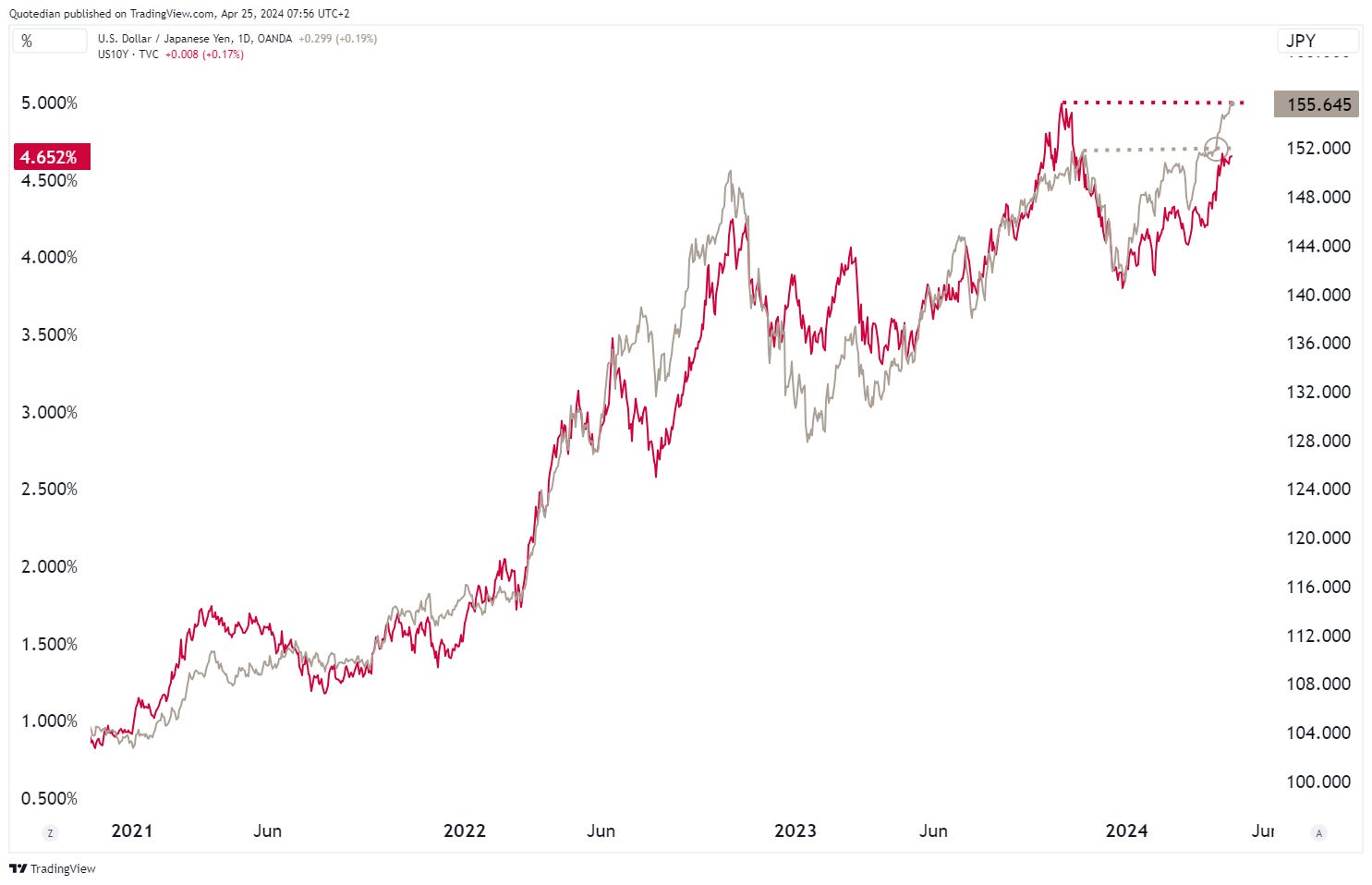

As the chart below shows, the correlation between the USD/JPY cross-rate and the US 10-year Treasury yield is high (R2 ~0.5). Comparing the same FX pair to the US10T yield minus 10-year JGB spread would give a very similar picture and correlation reading. The best explanation for this relationship lays in a mix between interest rate differentials, capital flows, market sentiment, and central bank policies, with the first having probably the largest impact. Which brings us back to our COTD – whilst the USD/JPY has broken above its previous November 2023 highs (grey dashed line & circle), the US 10-year Treasury yield has not, i.e. a divergence has been created. A “catch-up” on behalf of the treasuries, would take that yield well above 5% (red circled).