QuiCQ 27/03/2025

Energizing Energy

“If you can't be kind, at least be vague."

— Judith Martin

Enjoying The QuiCQ but not yet signed up for The Quotedian? What are you waiting for?!!

In Tuesday’s QuiCQ (click here) we highlighted that investors should pay attention to the $575 level on THE S&P 500 ETF tracker (aka Spider) as a possible level of resistance. Turned out to be timely advice, at least for now:

The equivalent of the underlying index would be at 5,775.

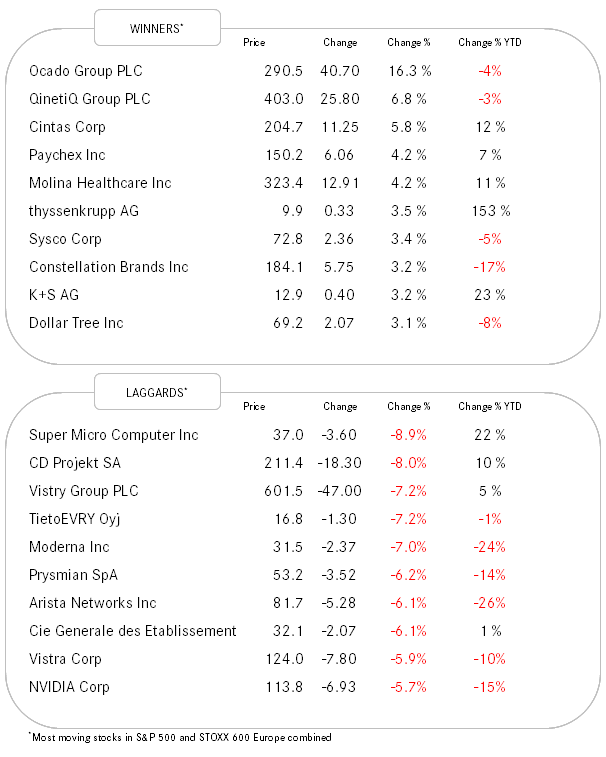

However, despite yesterday’s non-ignorable drop in excess of one percent of the S&P 500, more stocks than rose (266) than dropped (235) on the day and sectors up (5) versus down (6) was split in half as good as you can split eleven in half in this case:

Clearly then, the declines were led by some of the index heavy-weights:

So, any specific reasons for the sell-off as “more sellers than buyers” does not work as an explanation in this case?

Well, apart from technical set-up of course the usual Trump Tariff Tantrum (TTT) fears, reinforced by 25% slapped on no-US based automakers. Or maybe it some Fed speech warning about inflationary impact of TTT. Or maybe apparent gridlocks on Ukraine/Russia peace-prospects. Or maybe disputes regarding financing of the EU Readiness 2030 peace plan. Or maybe a bit all of the above.

Or probably, some simple profit taking in the more risky/growthy corners of the market:

In the US, bond yields are facing some upside pressures since breaking out of the 2-week trading range, probably on the back of tariff fears as we march towards ‘Liberation Day’ (2nd April):

Talking of ‘Liberation Day’ and given the level of the VIX, it is probably not the moment to LOAD up heavily on risk:

The US Dollar continues in some kind of recovery rally. Verus the Euro, 1.0670 and then 1.0590 would be the obvious targets:

Failure to reach those would be a strong sign of a cyclical downtrend to have been initiated.

The BOTTOM for oil (WTI) seems to be $65, from where it has been rebounding since the beginning of the month:

And finally, Gold seems to have coiled up five to six sessions and is ready to ‘spring’ higher again now:

Asian stocks are on the weaker side morning, notable exceptions Hong Kong, China and India. European equity futures are currently deep red, playing catch-up to yesterday’s sell-off in the US, whilst those later futures are flattish at the moment.

Time's up, more tomorrow - May the trend be with you!

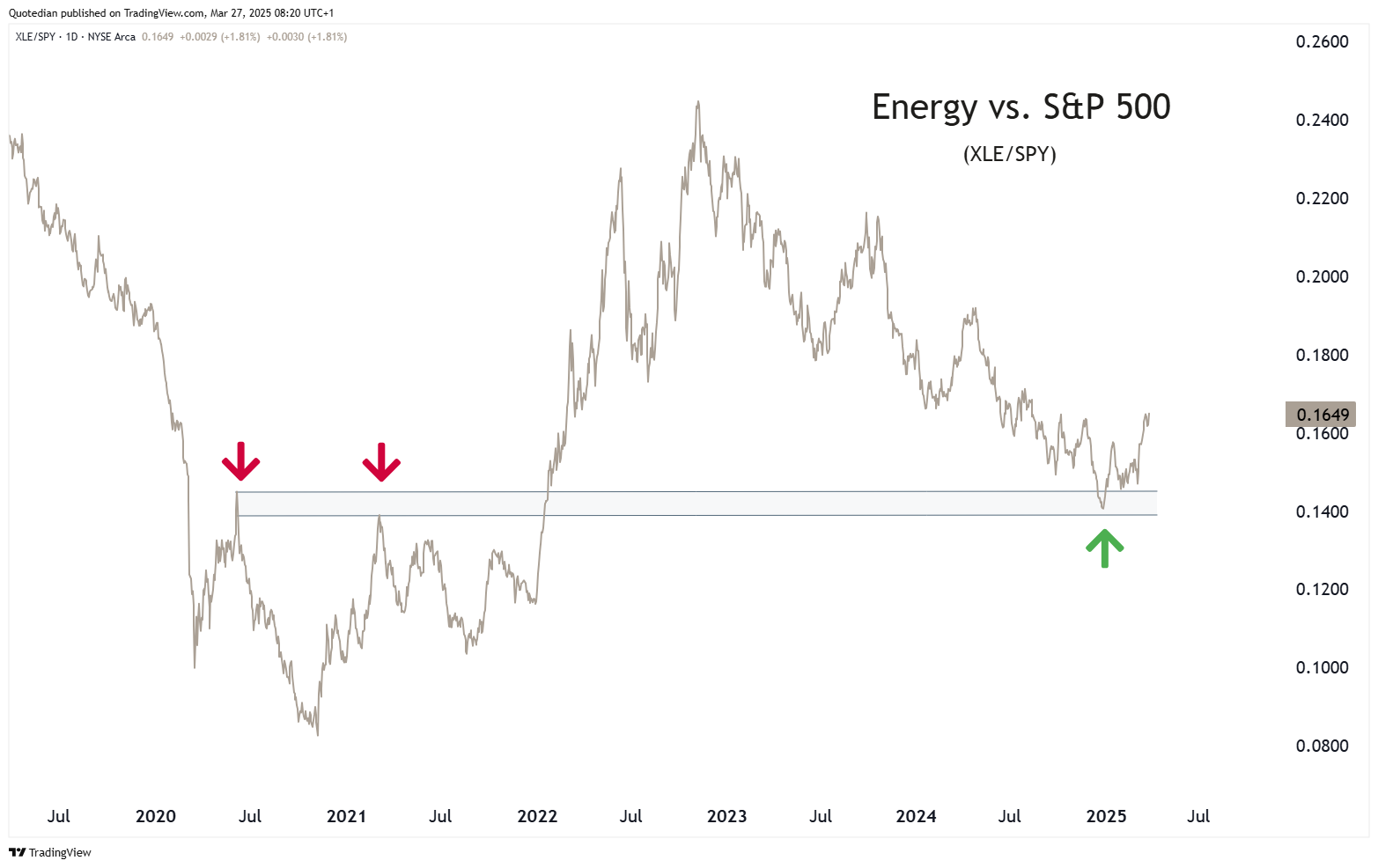

Crude oil price have been rebounding for two or three weeks now. Is it coincidence then that prices of major US oil companies (XLE) are also trying to put in a relative bottom, just at what seems to be a crucial pivot zone?