QuiCQ 27/11/2024

¡Ay, caramba!

“Feet, what do I need you for when I have wings to fly?"

Frida Kahlo

FOMO? YOLO? Or a bit of both?

Stocks, as measured by the S&P 500, headed higher for a seventh consecutive day and the 52nd new ATH for the year. Reason? Lebanon-Israel 60-day cease fire? I doubt it. Tech earnings? No. CRWD, DELL and HPQ all disappointed in their reports after-hours. A Fed that will continue to lower rates, albeit they should not. Perhaps.

On this latter point, the Fed minutes showed that the consensus for gradually lower policy rates prevails at the FOMC. But given that the stock market is at record highs with a valuation approaching the March 2000 highs, credit spreads are historically tight as a drum, the level of exuberance is very elevated, animal spirits post election are juiced up AND the Treasury market gave them a clear warning sign post their initial 50bp cut … PLUS, Trump has not yet insulted Powell over monetary policy, so no pressure from that camp either. I really think they should pause at least in December and wait for some more (weak) economic data to justify further cuts. But that’s just me …

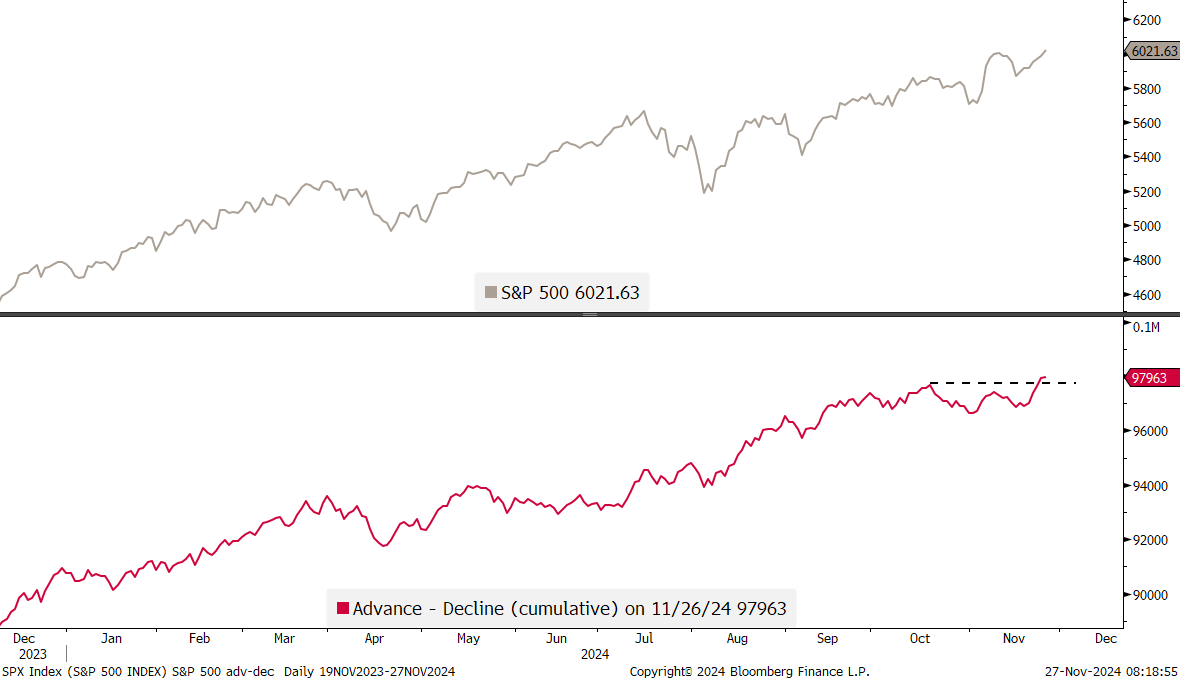

Back to the market quickly, where the S&P 500 with a new ATH as invalidated our expectation of a more complex correction, which we had outlined in the Quotedian over the past issue or two.

One of our main concern had been the rapidly falling cumulative advance-decline ratio (lower clip, red line), which was a sign of weak breadth. No need to worry anymore, as this indicator just made a new ATH:

We already expressed our suspicion that this could happen earlier this week, as the S&P 500 equal-weight index already hit a new ATH on Friday.

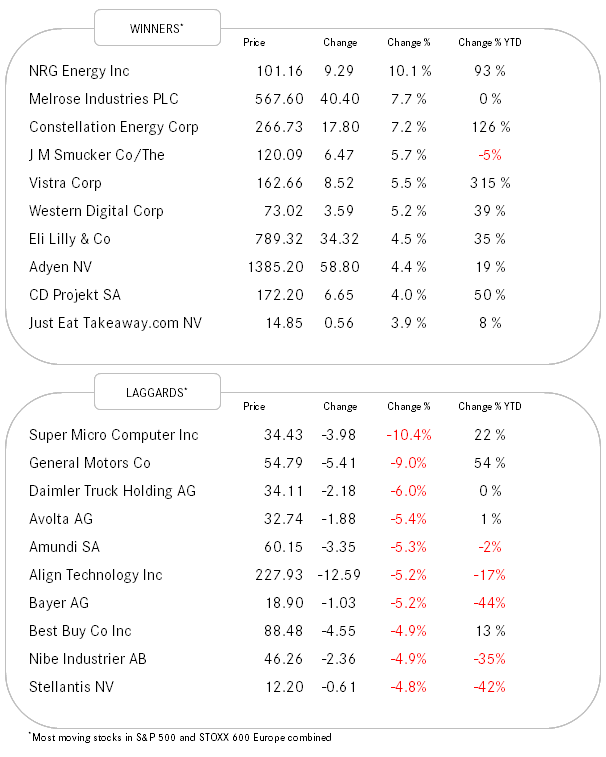

Just to finish of on equities, 99 red ballons stocks hit a new 52-week high yesterday, versus only three a new low, confirming positive breadth.

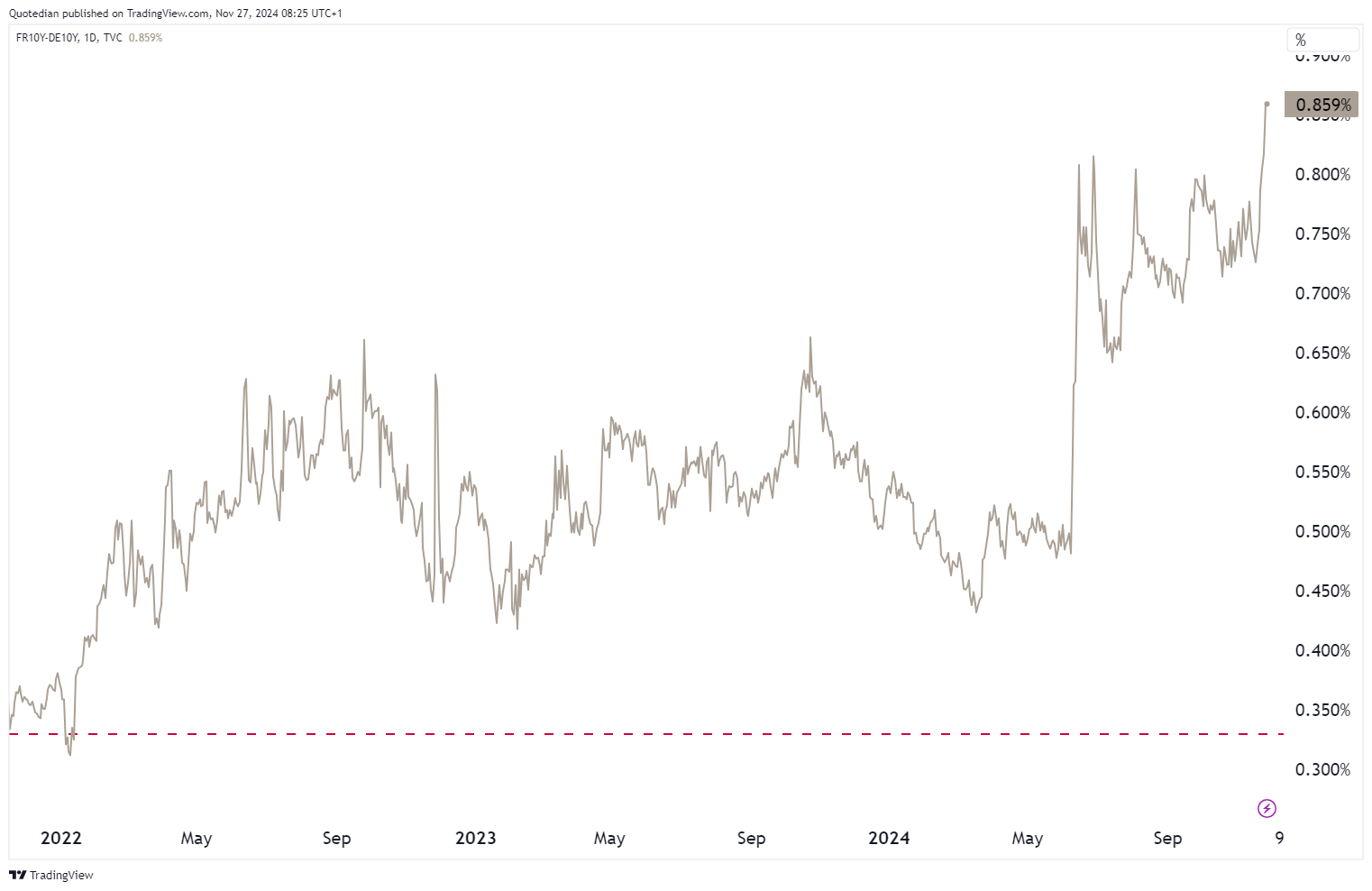

US yields moved little in yesterday’s session, wit the Tens continuing to hover around 4.28%. Worth noting is probably a pick-up in French government bond yields (below as a spread to their German counterparts), on the latest rumblings come after President Emmanuel Macron reportedly remarked that the fragile coalition government will fall.

In currency markets, the JPY showed a very decent rally versus the Greenback:

Really, really watch this space too, as I think the long JPY trade has the potential of being THE macro trade of 2025, should the Trump administration note (hint: they likely already have) that Japan is the bigger currency manipulator than China. Add to JPY longs below 151

Have a great day,

André

On Monday night, President elect threatened via a post (on his own social media platform - go figure…) that he would not only slam 10% of additional tariffs on China, but also 25% of tariffs on Canada and Mexico.

Guess which stock market is taking it better?

Spoiler Alert: Not Mexico