“The only constant in life is change.”

— Heraclitus

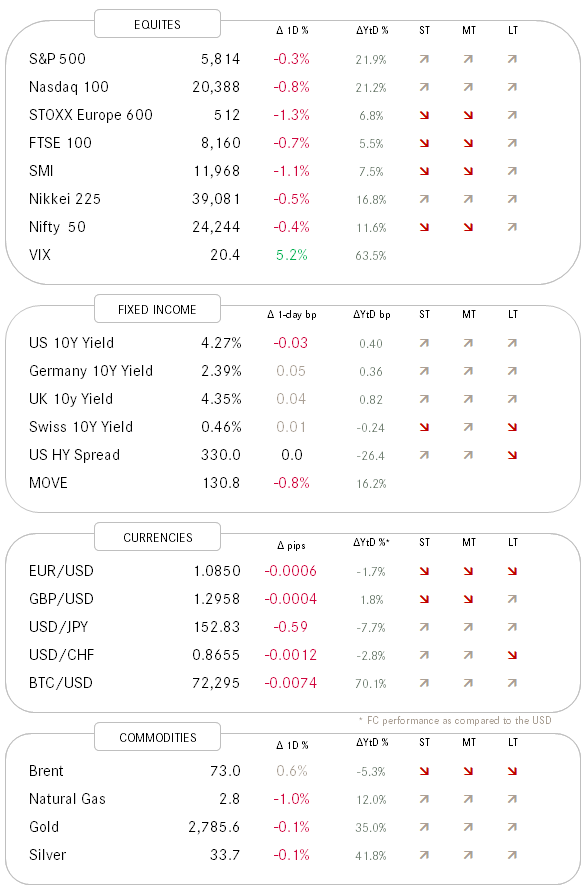

Yesterday’s equity session was volatile though within a confined range, partially driven by macroeconomic data though mostly by earnings surprises to up- and the downside. On the latter, did for example Google’s earnings lead stocks higher early on in the session, whilst disappointing results from AMD (-11%), followed by Super Micro Computers’ auditors (EY) resignation announcement, weigh heavily on stocks. Eli Lilly, Ebay, Coinbase and Micrsoft after the close were some other companies disappointing on the earnings side.

Taking our usual quick look under the (S&P 500) hood, we note that despite the third of quarter percentage point retreat and only three out of eleven sectors printing green, the number of stocks up versus those down was very much balanced and 28 stocks hit new yearly highs versus only three new lows.

On the macro front the UK budget got a lot of attention. Probably could have been worse, as we did not quite get a Liz Truss-moment, yet it was “generous” enough to push UK 10-year Gilt yields 20 basis points higher intraday before settling at a level for an eight points net change. In a little side note to the budget, chancellor Rachel Reeve clarified the on Inheritance Tax on AIM shares (the most ventures part of the UK stocks market). AIM shares will attract an inheritance tax rate of 20% if they are held for two years, which eliminates of course the exemption in place so far, but a subsequent 5% rally on the AIM 50 index indicates that worse was expected.

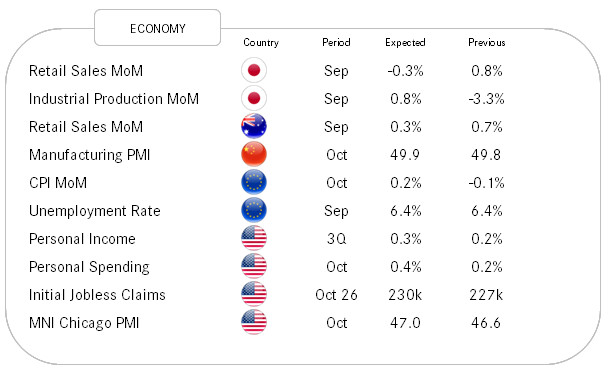

Different job numbers in the US continue to provide a hot “foreplay” (yes, I really wrote that) ahead of Friday’s NFP number. Other indicators (Consumer spending, pending home sales) also pointed to a continuedly strong economy.

Gold hit another new all-time high (I think I put that part into the template to save me from future typing), whilst the Greenback is showing further signs of reversal of recent strength.

Asian markets are trading mixed this morning, with Japanese stocks small down and the Chinese complex (Mainland, Hong Kong) even smaller down.

Some more economic data out today, but slowly all eyes are shifting to tomorrow’s non-farm payroll October reading.

Can’t remember who wrote it, but I recently read the headline “The sick man of Europe is Europe”. While snazzy, I do not concur.

If we take small cap equity performance as the pulse of an economy, which I think is a good proxy, then the following chart, comparing small cap index performances over the past two years, clearly shows that Europe is moving at two different speeds:

So, quite contrary to the original figurative meaning of “When Pigs Fly”, PIIGS are really flying here.

Permanezca atento … Restate sintonizzati … Fique atento … Μείνετε συντονισμένοι