Quotedian - Daily Edition 03/03/20206

Pavlov's Dog

“We are all conditioned.”

— Ivan Pavlov

As I wrote in yesterday’s LinkedIn post (click here), the fog of war surrounding the Middle East is still thick and heavy, and this is not the time to make some heroic market calls.

However, I would start daring to make some shy observations, which are mostly of unsettling nature.

We all know that the five most expensive words in finance are:

“This time it’s different”

However, let me use for today:

“But what if …”

For starters, the last nearly twenty years of (equity) market sell-offs, especially with relation to geopolitical events, have taught us to “fad them” aka “BTFD”. One of my all-time favourite analysts (no, no cheek in tongue, really adore the guy) cheerleaded that notion yesterday in X:

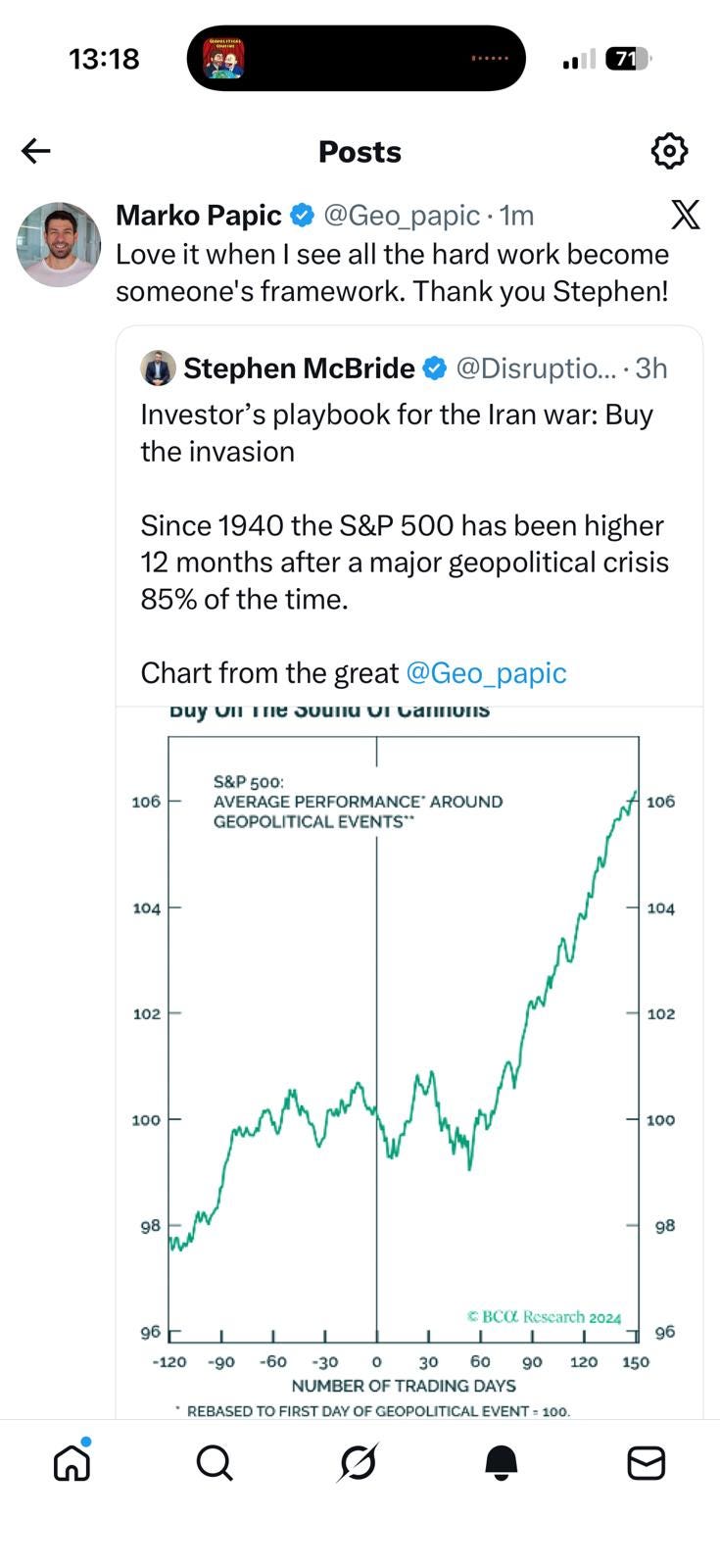

Or in other words, this is the quantitative confirmation of what Nathan Mayor Rothschild said some x years ago:

“Buy on the sound of cannons, sell on the sound of trumpets.”

And here’s where my “What if…” comes in …

WHAT IF … the failure of the US 10-year treasury bonds not only meaningfully fail to gain territory, as they usually do during major global geopolitical events, but even see a more-than-notable sell-off is a tell sign?

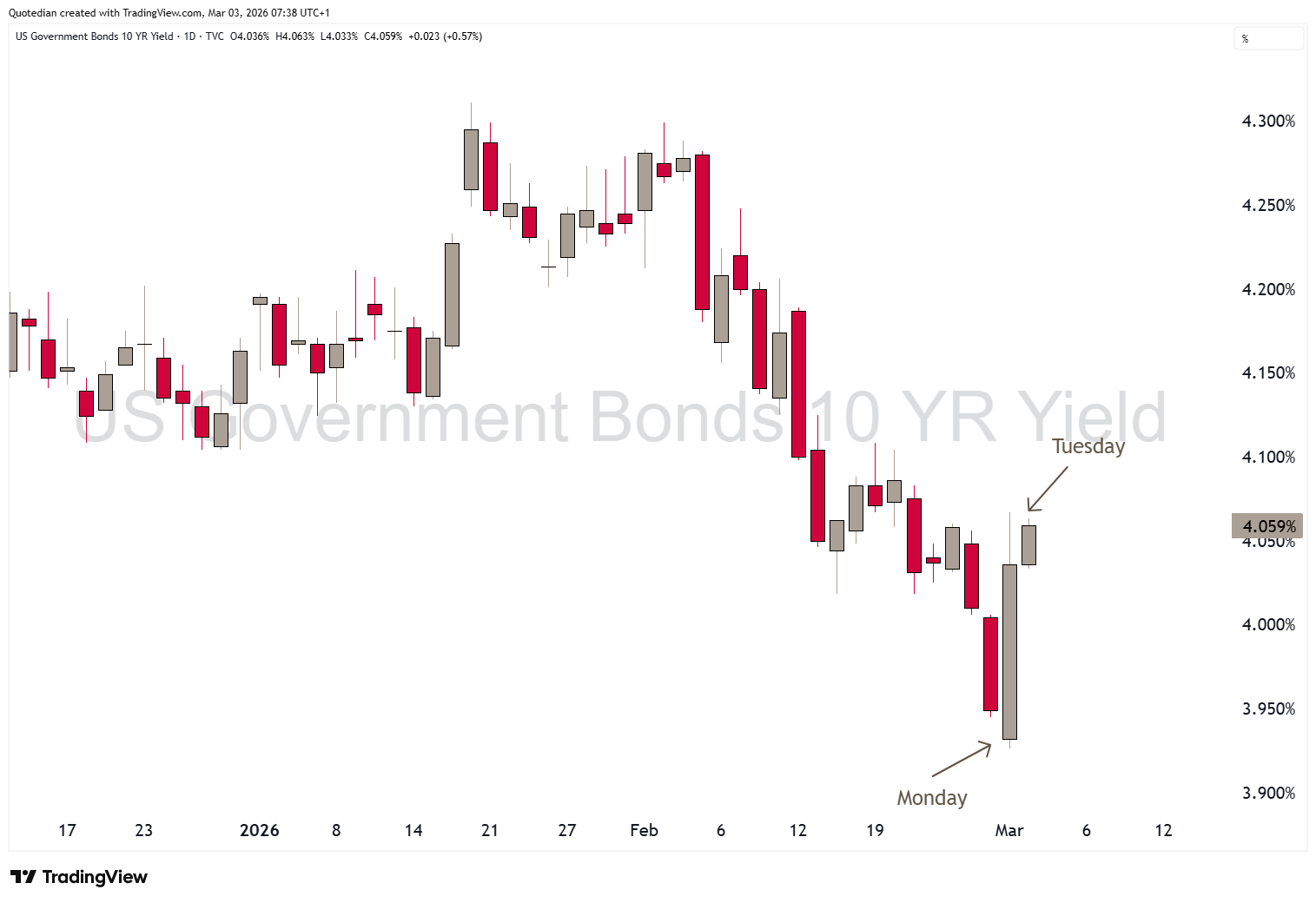

Here’s the 10-year US Treasury yield (opposite of bond prices):

That 12/13 basis points from bottom to top is not negligible. Is it based on an increase on an expected rise in future inflation? USD inflation swap rates would answer that rhetorical question with a firm YES:

Is that inflation expectation increase due to a higher crude (oil shock?) only?

Largely, but not excusively. General supply chain worries are probably playing a role too.

For example, WHAT IF a major US online retailer would suddenly see its operations hit in the Middle East?

Oh? Oh! We already had that!!

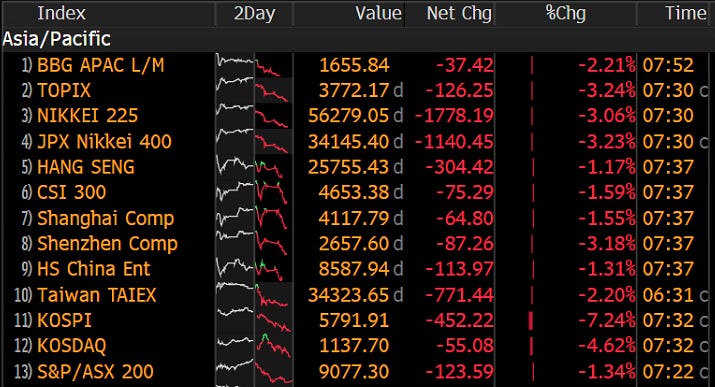

Is this maybe why equity markets have turned sour again overnight, after they had reclaimed early losses on Friday? Here’s the S&P mini-Future since Friday:

Asian markets are feeling some heat this morning:

Also moving … Silver, where maybe the industrial aspect is suddenly "shining “ (ha! what a silly pun!) through more than its precious metal affiliation:

That is a 14% drop highlighte in that chart over just two sessions …

Gold, for the right reasons, is hanging on in there:

I insist, not the time to stick out your neck investment wise, and if the itch becomes too strong, focus on (small) position sizing.

Three quick mentions:

The USD is finally reacting to the upside:

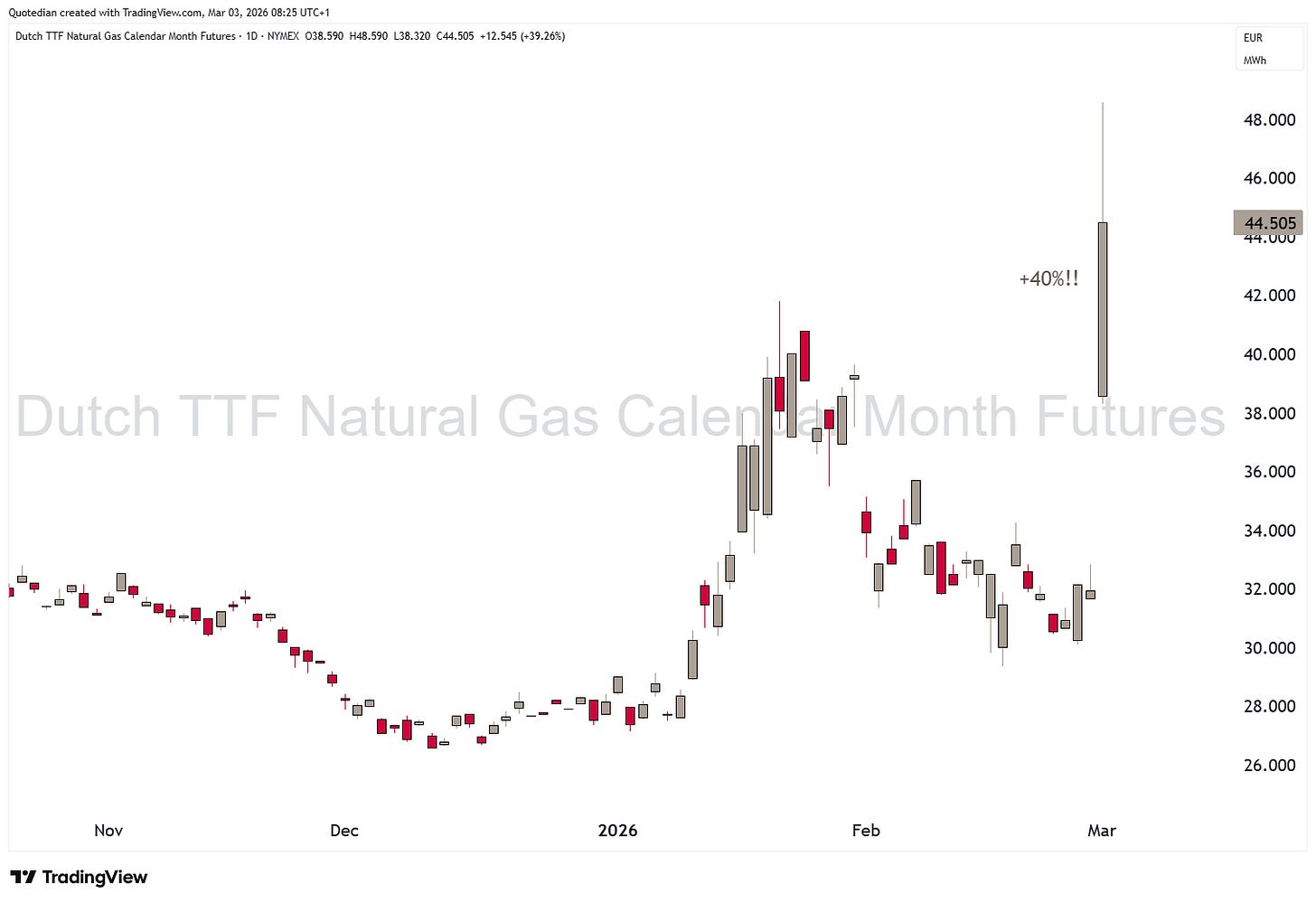

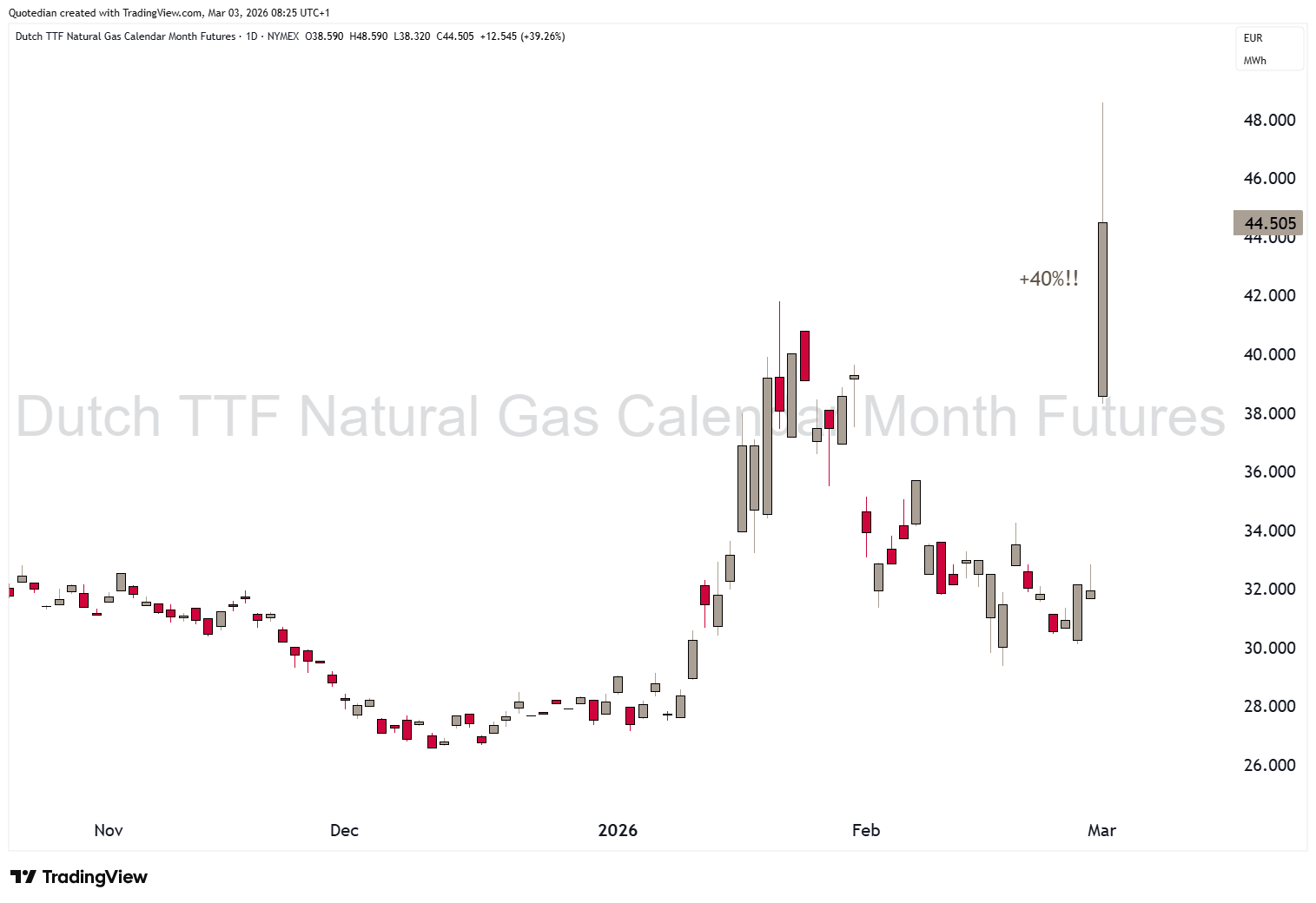

European defense stocks largely failed to react to war breaking out:

which could mean most is already priced in, or,

investors expect a massive increase in European energy costs (and defense is an-energy heavy industry). Here’s the price jump in Dutch Natural Gas prices:

Let’s pretend for a moment there is no major geopolitical conflict going on right now.

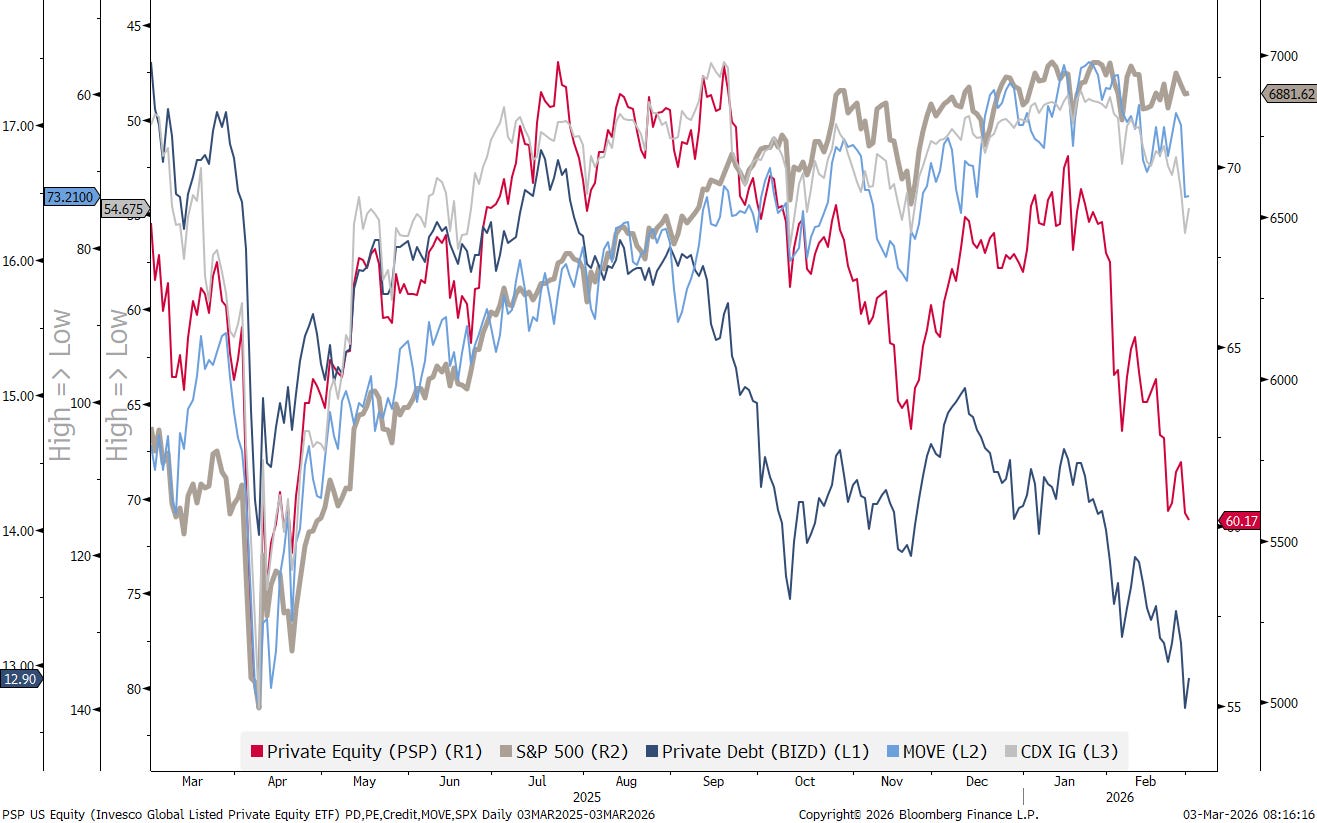

Seems everybody has already forgotten about the private credit disaster story that is unfolding and seems to be showing first sign of contagion into private equity and financial (bank) stocks.

The chart below basically asks, if (or when) the last domino stone (aka broader stock market) will fall:

First, private debt (blue - BIZD) started tumbling

Shortly after, private equity (red - PSP) followed

Recently, bond volatility (light blue - MOVE) and Credit Spreads (light grey - CDX IG) - both inverted - have turned ‘lower’ too

Will stocks (thick grey - SPX) soon follow?

Little on the economic agenda, except some inflation data out of Europe (which now does not matter until in a few months) and Japanese unemployment numbers

Fed’s Williams & Kashkari Speak

Trump meets Merz at White House

UK Chancellor Rachel Reeves delivers her Spring Statement

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG