The Q - Daily Edition

Yes but, no but, yes but ...

"When the facts change, I change my mind. What do you do, sir?"

— John Maynard Keynes

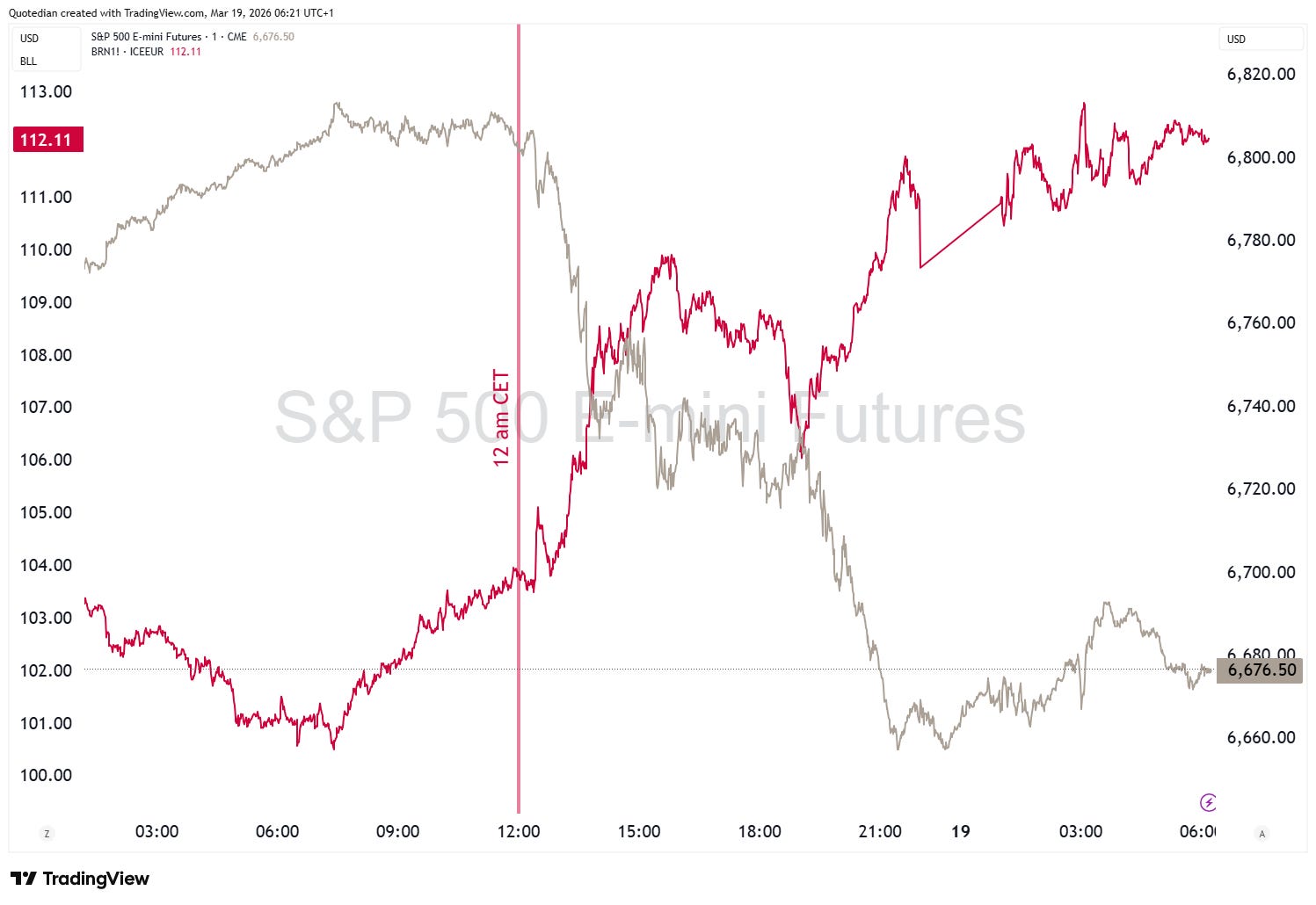

I was going to admit that there is some egg on my face with yesterday’s call for (equity) risk-on.

However, I was right for till about European lunch time:

More or less from then on it was oil (red) up and stock (grey) down:

The key news of the last 24 hours is of course Israel’s attack on Iran’s South Pars gas field. This is an escalation, attacking oil production facilities for the first time.

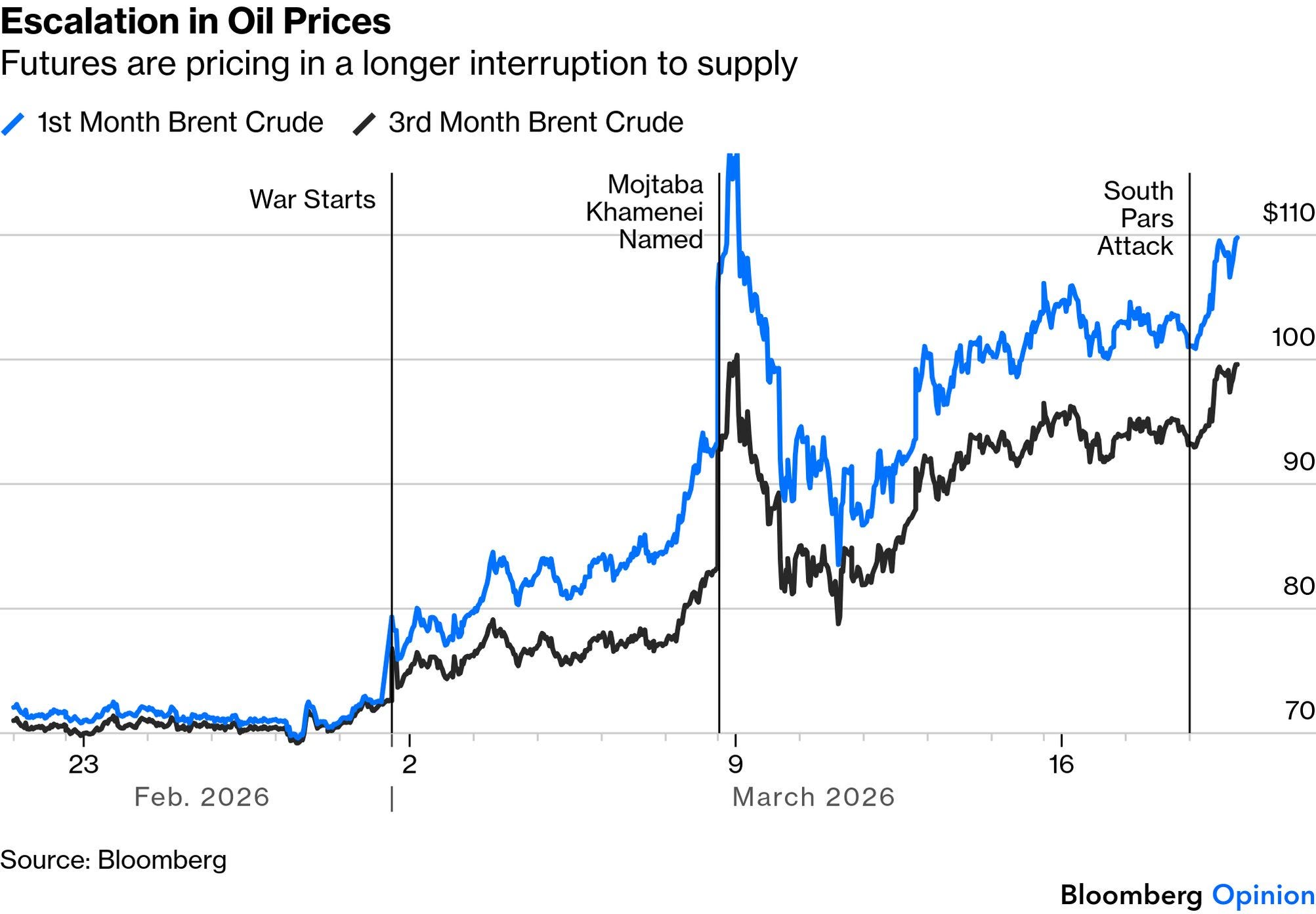

And, it is clearly Israel playing with (literally) fire, which was immediately depictured in the oil futures markets. Whilst the nearest (1 month) futures (blue line below) has not quite yet reached the previous high, the 3-months futures prices (black line) did hit a new cycle-high, expressing the market’s concern that this conflict will go on for longer.

Of course, there was also a Fed meeting yesterday, which was more about “boardroom battle” than interest rate policy. Regarding the latter, the decision was to leave the policy rate unchanged, with strong hints at the fog of war making any immediate visibility more than murky. The decision was nearly unanimous, with only one dissident. Guess who!

Critically, Powell updated his career plans. If Kevin Warsh isn’t confirmed by the end of his term as chair, he said he will carry on as chairman pro term. And as long as the government continues to prosecute him , he will continue on the board of governors, where his term has two years to run…

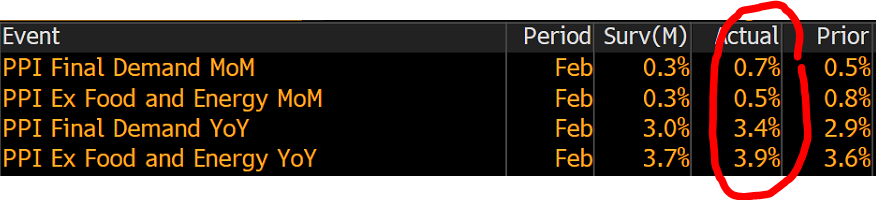

Talking of egg and faces, I also highlighted yesterday how much yields, illustrated via the 10-year US Treasury yield had come down over the past sessions.

Well, that was that …

The pointed hand is yesterday’s session, which saw a huge reversal not only because a renewed spike in oil prices (which was actually nearly the secondary reason yesterday), but mainly due to a “surprise” high reading in the Producer Price Index:

Is our long-awaited second inflationary wave finally coming? Perhaps.

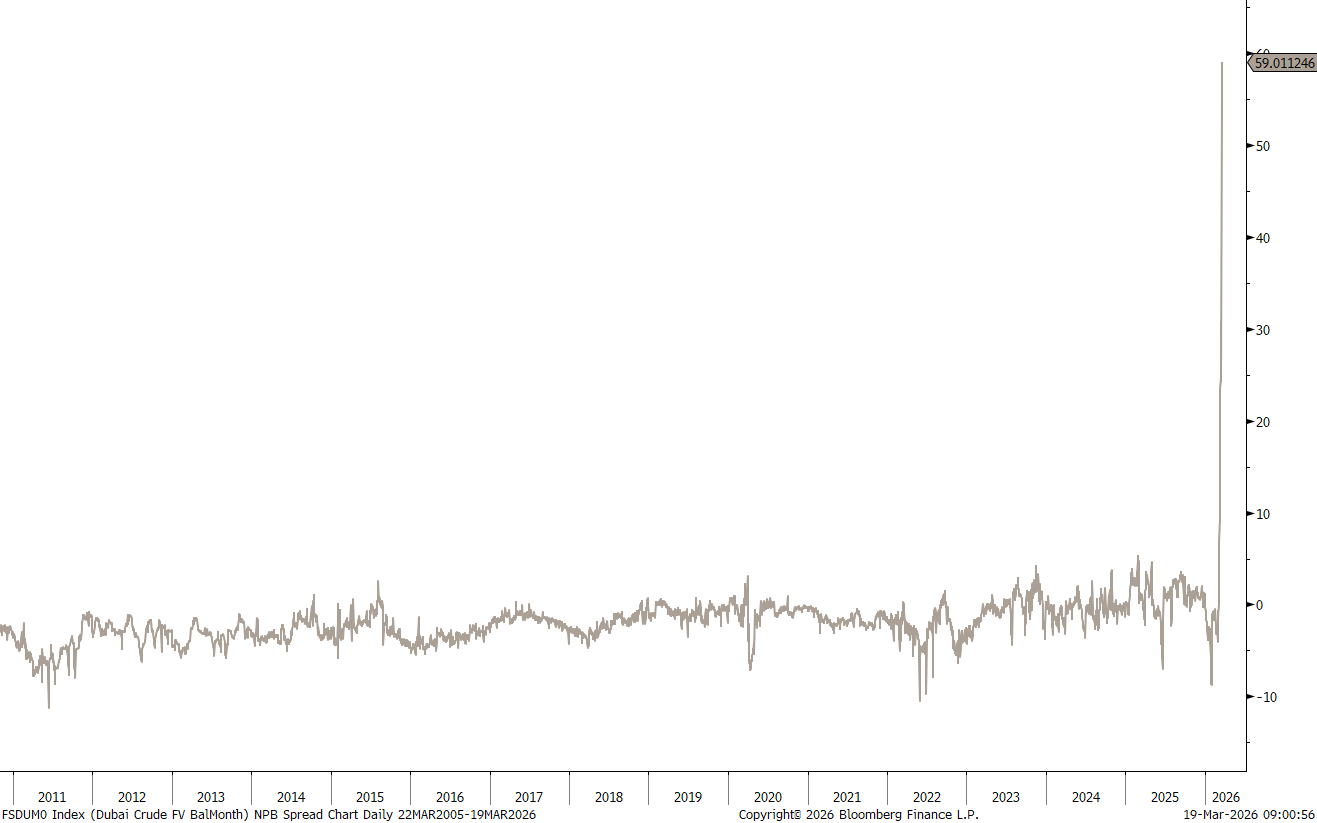

Above we spoke about how the backwardation in oil futures is slowly abating, as investors start assuming a longer war ahead. One spread that is interesting to watch is the price of oil in Dubai versus Brent. Below the spread, historic, I’d say …

BoJ rate decision — already out. Held at 0.75% (8-1, Takata dissented wanting 1.0%). Flagged upside inflation risk from Iran/oil. USDJPY back toward 159.

SNB rate decision — 09:30 CET. Quarterly monetary policy assessment. Key read for CHF and European rates path.

BoE rate decision — 12:00 GMT. Expected hold at 3.75%. Watch MPC vote split — was 5-4 in Feb. Inflation re-accelerating toward 4% vs. zero-growth economy = stagflation trap.

US Initial Jobless Claims — 8:30 ET / 13:30 CET. Exp. 215K vs. prior 213K.

US Philly Fed Manufacturing — 8:30 ET. Exp. 8.3 vs. prior 16.3. Big drop expected — watch prices paid component for stagflation signal.

US Building Permits — 8:00 ET. Exp. 1.376M vs. prior 1.455M.

US New Home Sales — 9:00 ET. Exp. 722K vs. prior 745K.

Fed Beige Book — 14:00 ET / 19:00 CET. First post-FOMC anecdotal read.p

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG