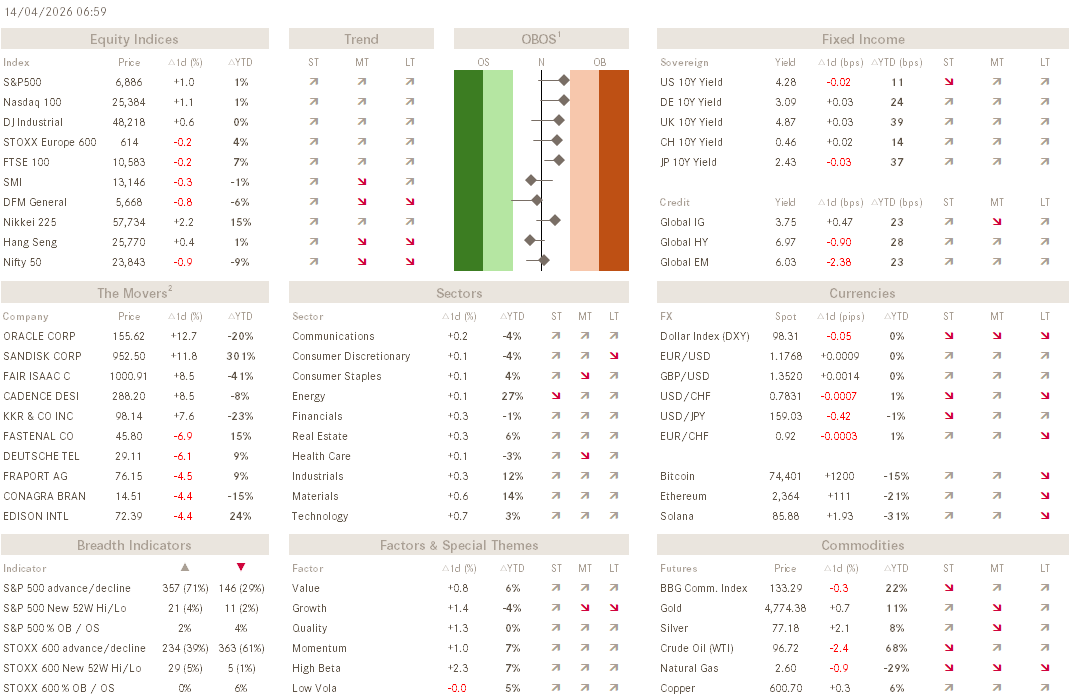

The Q - Daily Edition

Back To Square One (And Then Some)

“In preparing for battle I have always found that plans are useless, but planning is indispensable.”

— Dwight D. Eisenhower

So, there we are, with the (US) equity market having unwound ALL of its Iran War induced losses - and, since yesterday, and then some! Including yesterday’s two percent plus jump, the S&P 500 is now 1.5% higher than when the war broke out in the first March days:

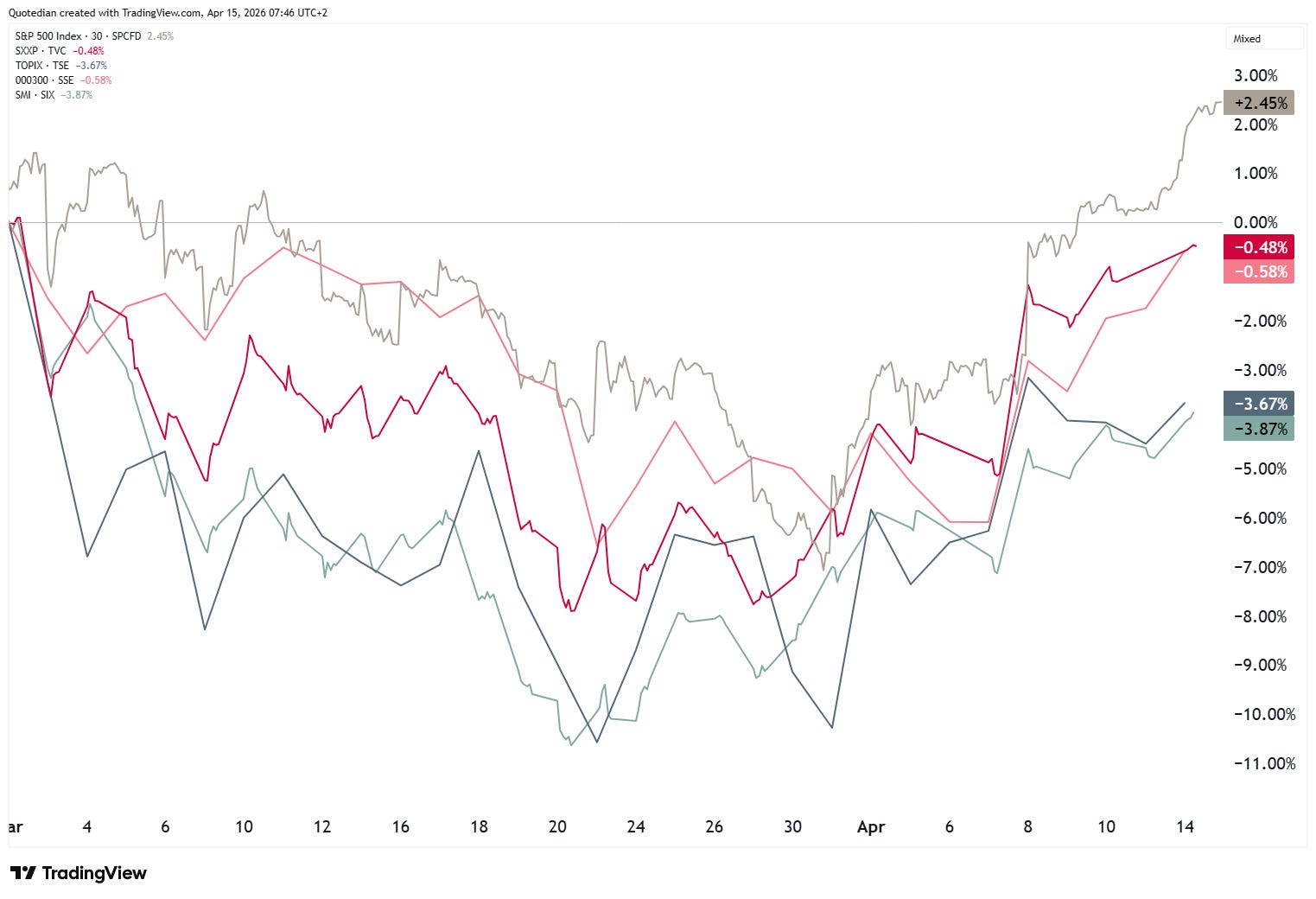

True, not all international markets enjoy the same recovery (a selection below),

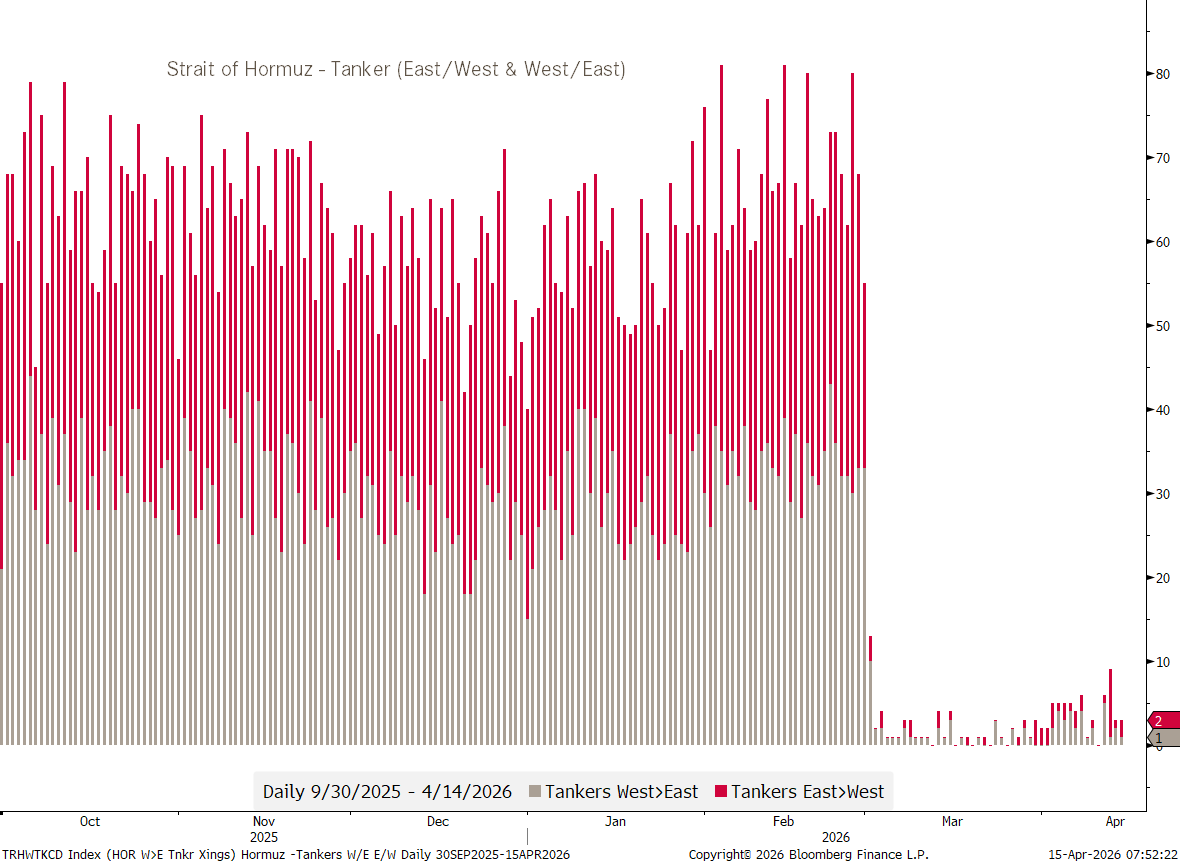

but overall it is fair to say that the market is expecting the ceasefire to turn into a peace treaty and also does not consider the still largely closed Strait of Hormuz (SoH)

to be a longer-term threat.

Well, good luck with that. As we highlight in our latest quarterly NPB CIO Outlook (click here) we are in favour of a short- to medium-term rally, but the longer term consequences of higher oil, fertilizer, helium, plastic, etc. prices should not be underrated… See the Chart-of-the-Day for more on this.

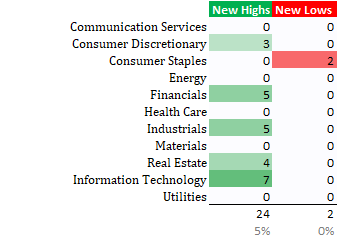

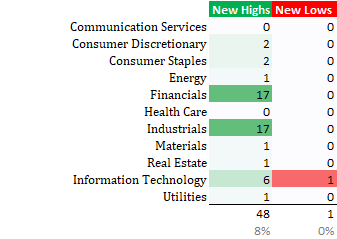

But back to yesterday’s rally, which was healthy not only in absolute progress, but also under the hood. Whilst the advancers-to-decliners ratio on the S&P 500 was ‘only’ 3:2, twenty-four stocks hit a new 52-week high, whilst only two a new 52-week low:

An even better stat on the same hit us out of Europe (SXXP):

Back to US stocks, where small cap stock have been on a 12%-plus tear since March 30, closing less than half a percentage point from a new all-time high (ATH):

Outside equity markets, bond yields are signalling some return to normality (whatever that means in financial markets, especially nowadays). Here’s the US 10-year Treasury yield, which could continue to move lower as equities continue to rally:

4.40% is now the big risk point.

German yields, as proxy for the Eurozone, have also calmed a tad, though remain above 3% for now:

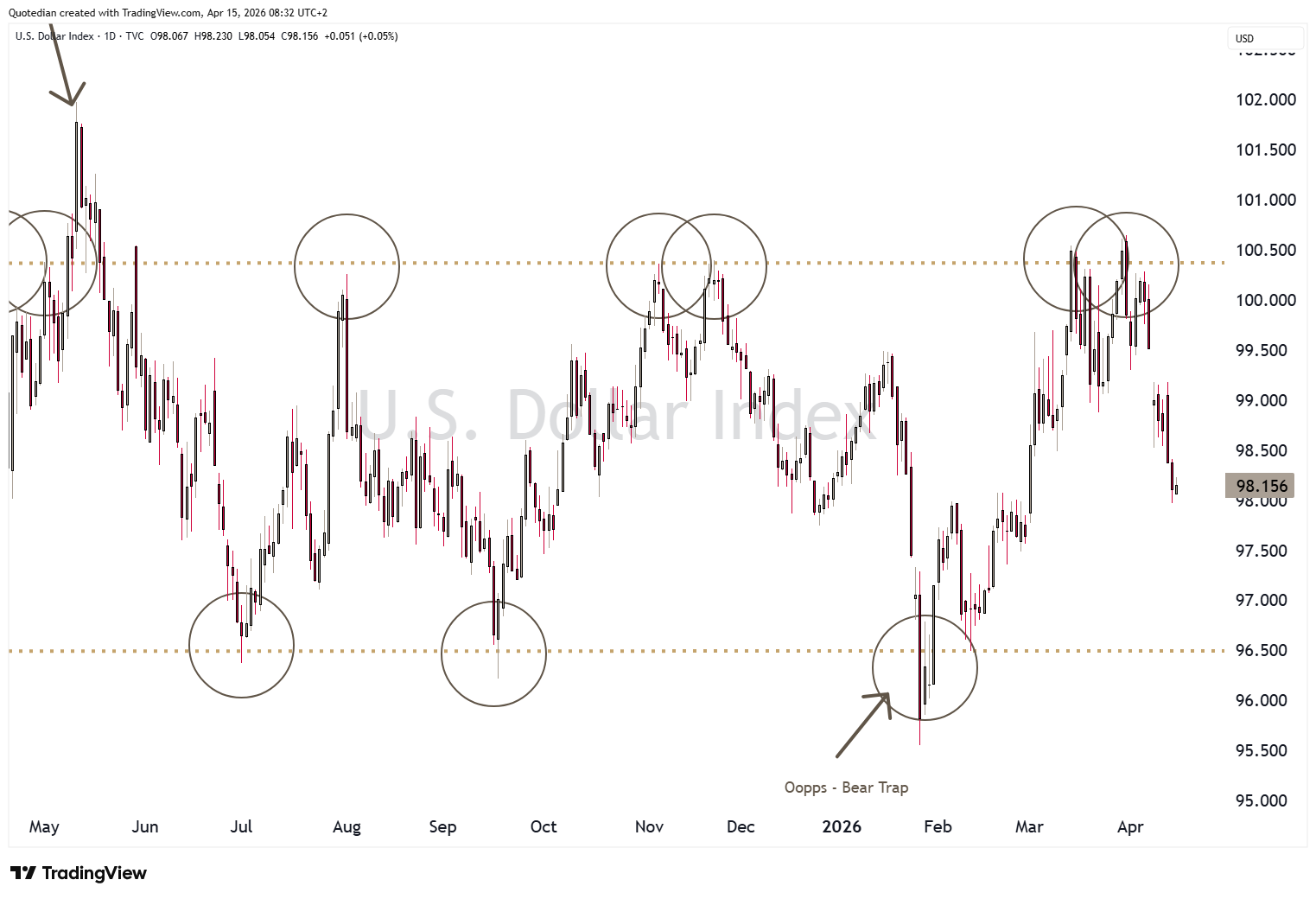

The USD continues to be one of my favourite, structural shorts. Here’s the Dollar Index (DXY):

And don’t look now, but Bitcoin may be up to something naughty:

In the section above I noted that investors should enjoy a short- to medium-term market rally, but should not turn a blind eye on the perils from longer-term impact of the SoH closure.

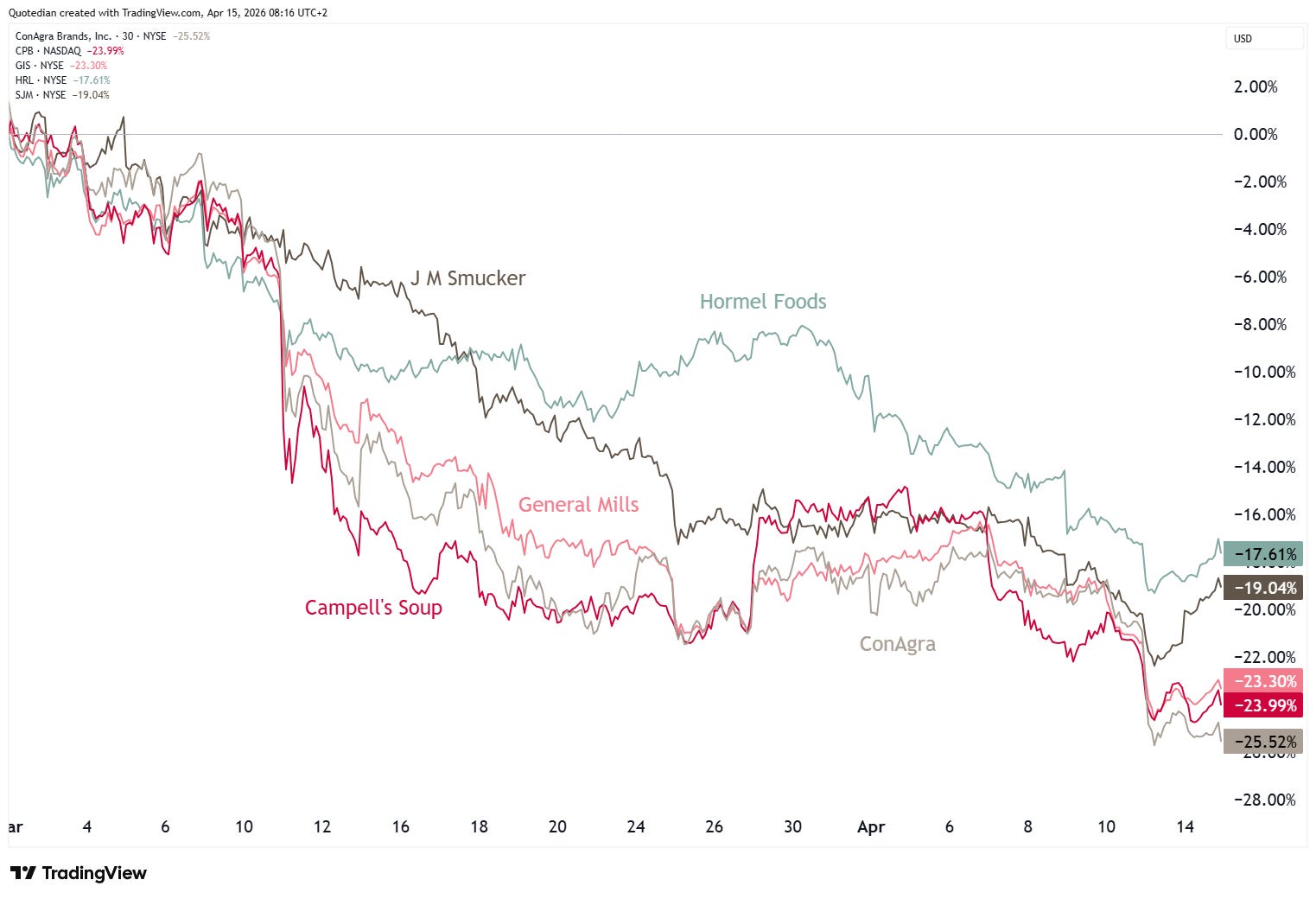

Point-in-case: Why do you think stocks of food makers have been under substantial pressure, hitting new 52-weeks lows early this week, and barely recovering with the rest of the market?

Yes, exactly. Higher input costs ahead! Watch this space….

Later today:

US eco data: MBA Mortgage Applications, Empire Manufacturing, Export/Import prices and the glossy magazine that is the Fed’s Beige book

Earnings: ASML, Helvetia Baloise, M&T Bank Corp, PNC, BofA, Morgan Stanley

May the Trend be with You!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG