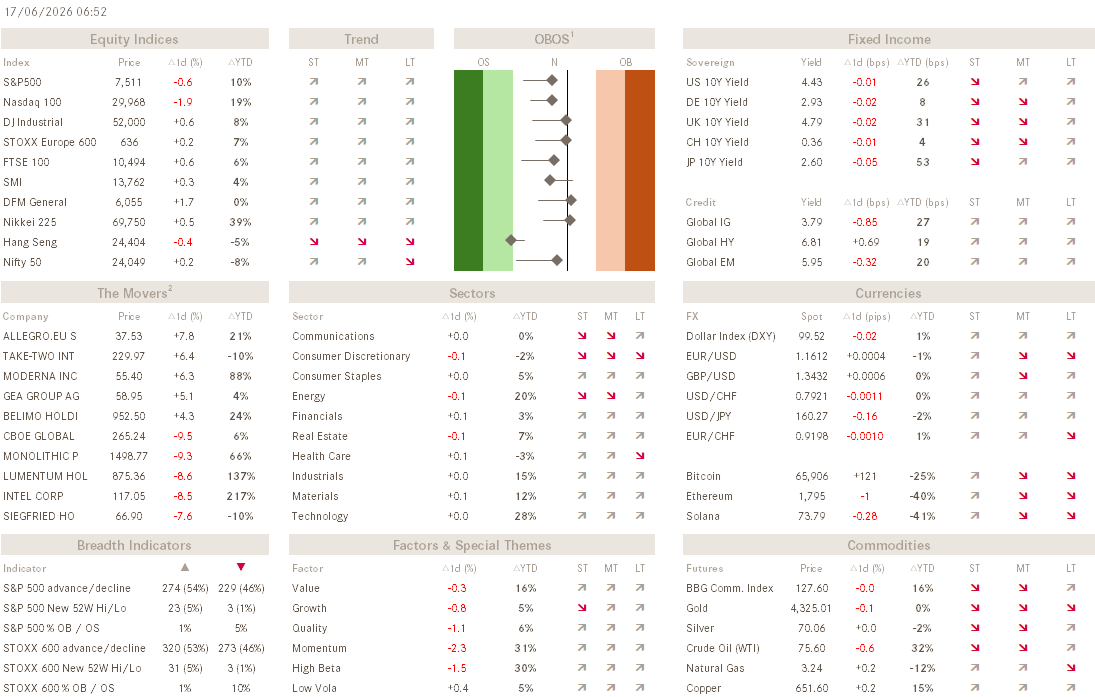

The Q - Daily Edition - 17/6/20026

KEEEVIIIIINNN!!!

“If you have a problem with me, text me. And if you don’t have my number, you don’t know me well enough to have a problem with me.”

— Christian Bale

Yesterday’s session felt a bit like this:

Whilst the stock was up ‘only’ five percent by the time of closing, down from an intraday high of up nearly 20%,

it seems the buyers of SPCX financed their purchases by selling their chip-making stocks contingent, with the Philadelphia Semiconductor index (SOX), down about by the same percentage points:

Noticeably, not a single stock in the SOX was up on the day:

The S&P 500 dropped a more timid half a percentage point on the day, and remains stuck between our upper and lower lines in the sand, as discussed in last weekend’s Quotedian (click here):

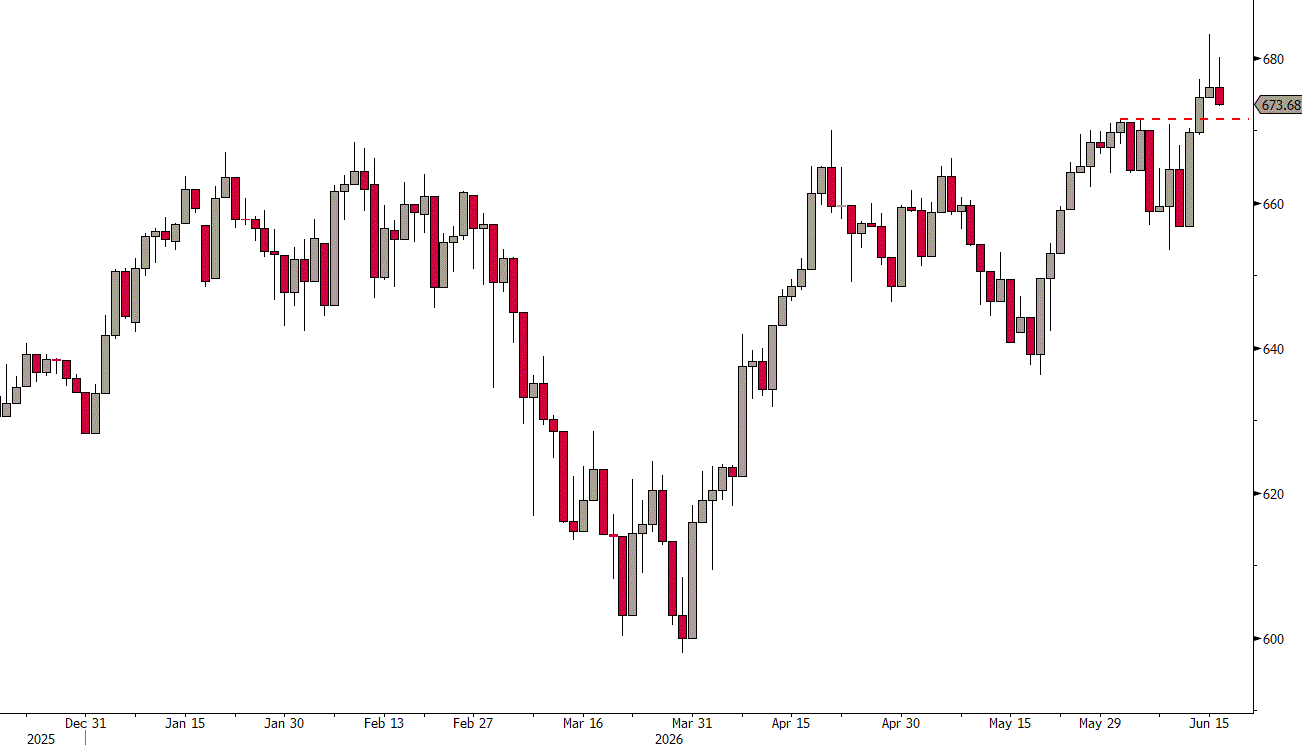

Whilst we remain disciplined and wait for a clear breakout on either side before fulling adding or reducing equity risk, we continue to think the break will be to the upside, given that several indices have either hit a new ATH or at least a new cycle high already, including the S&P 500 equal-weight index, the Russell 2000 small-cap or even the very broad Valueline Geometric index (VALUG - see below):

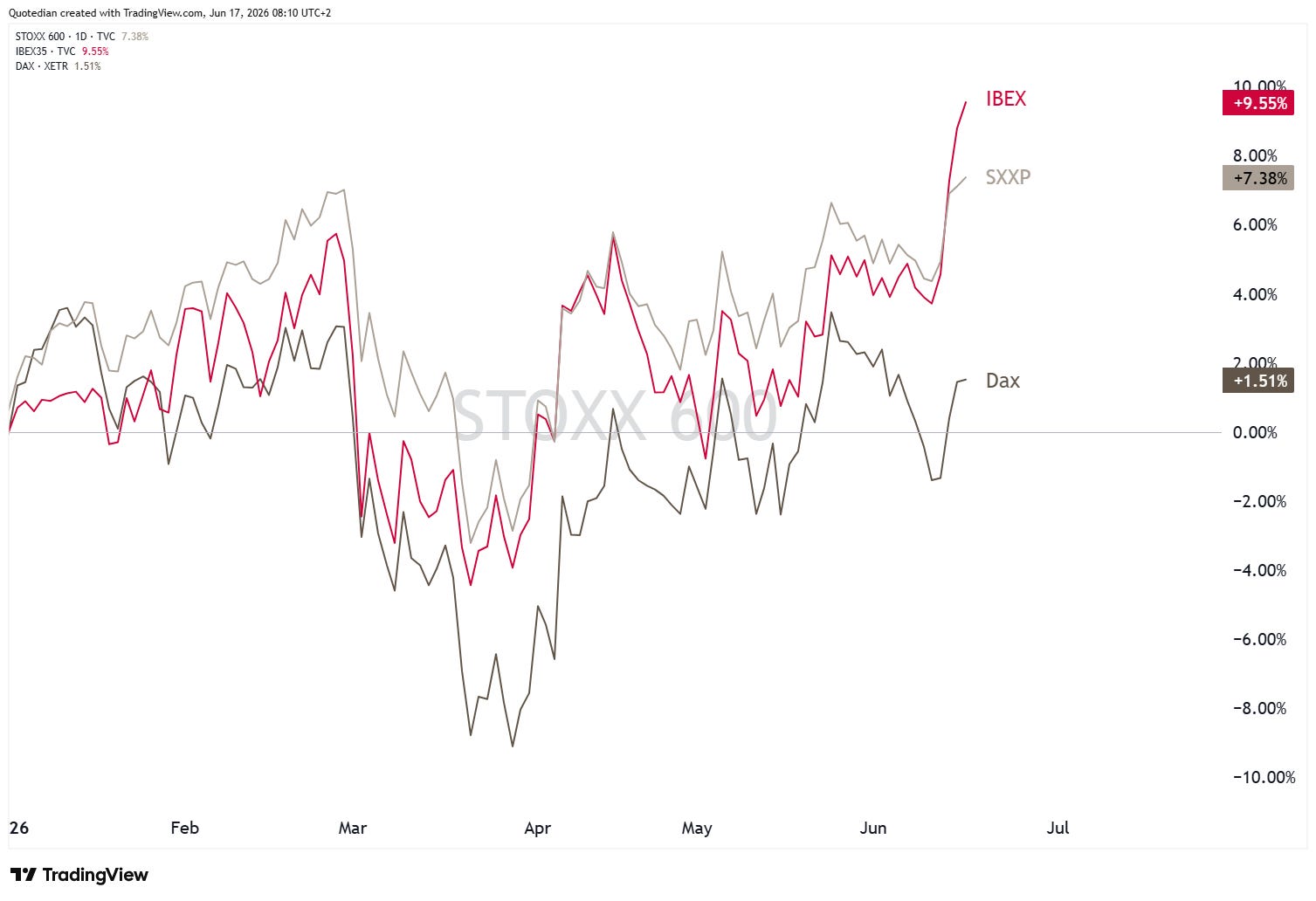

As previously discussed, European stocks (SXXP) have also reach new ATHs,

however, the spread between good (e.g. IBEX) and less good (e.g. DAX) is becoming very meaningful:

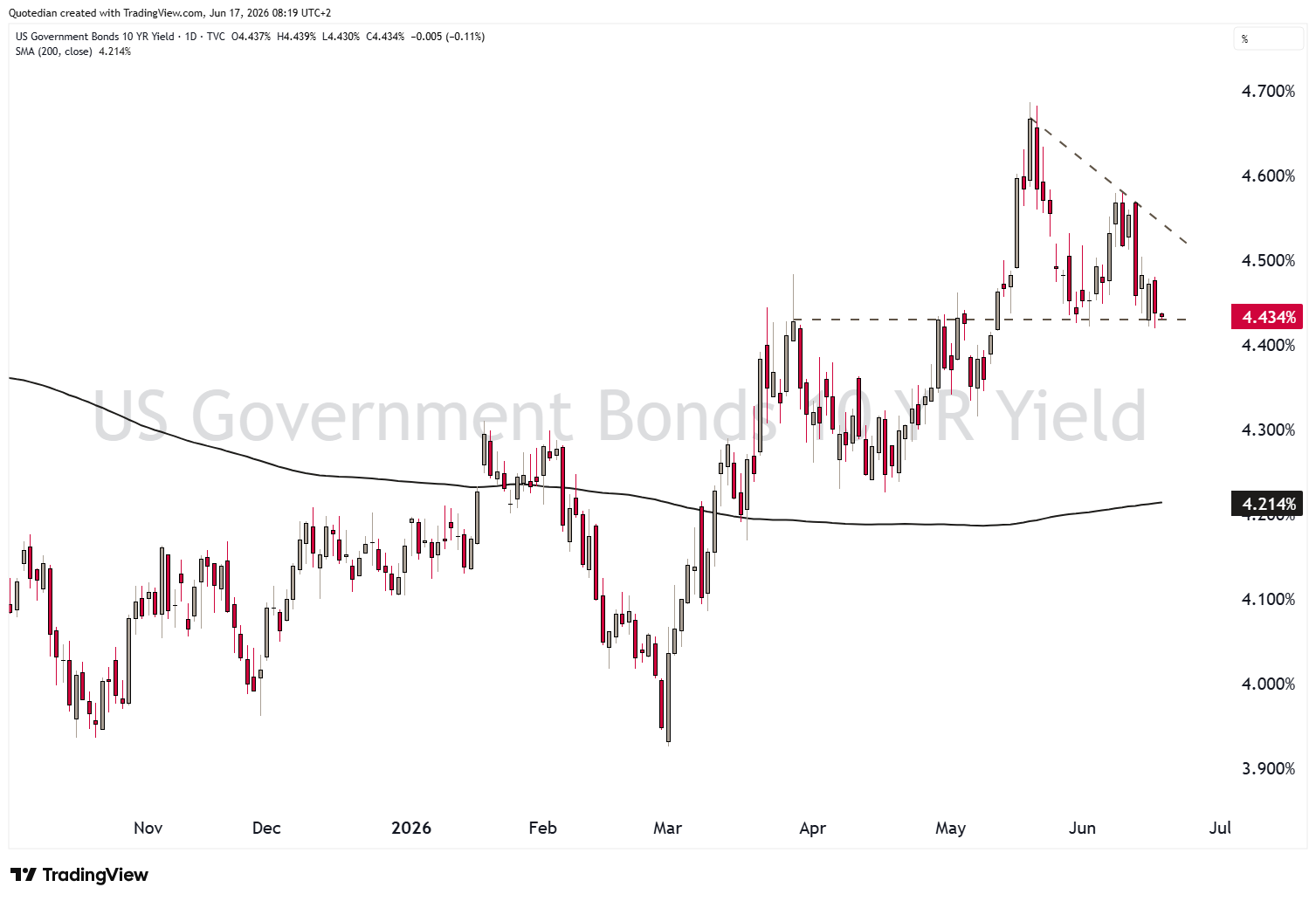

Turning very briefly to bond markets, where the world is waiting for tonight’s appearance of Mr Kevin Warsh as new Chairman of the Fed (also see the WTW section below).

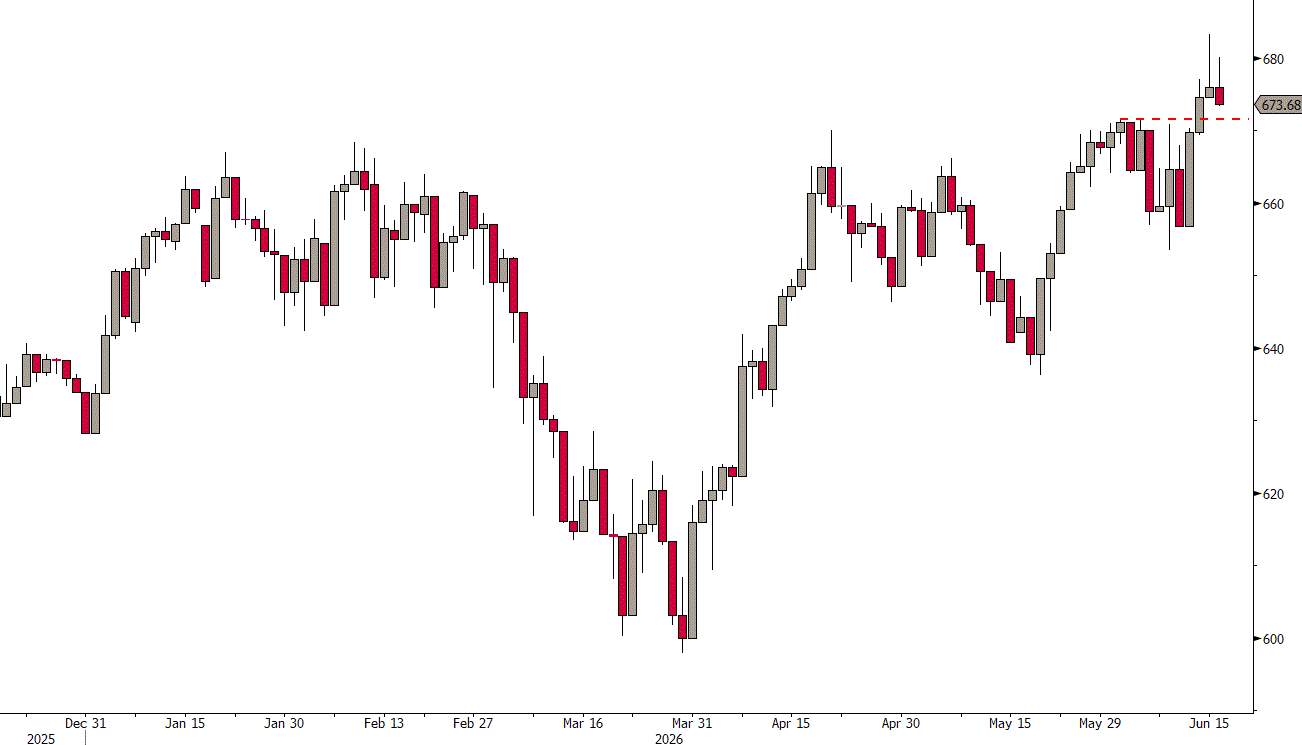

The US 10-year yield continues at the very lower end of the pennant (flag) formation I highlighted on Sunday and whilst I continue to believe that rates will move higher over the next few months to years, the next immediate move could be lower:

This is also we I mentioned a possible tactical long trade on the TLT:

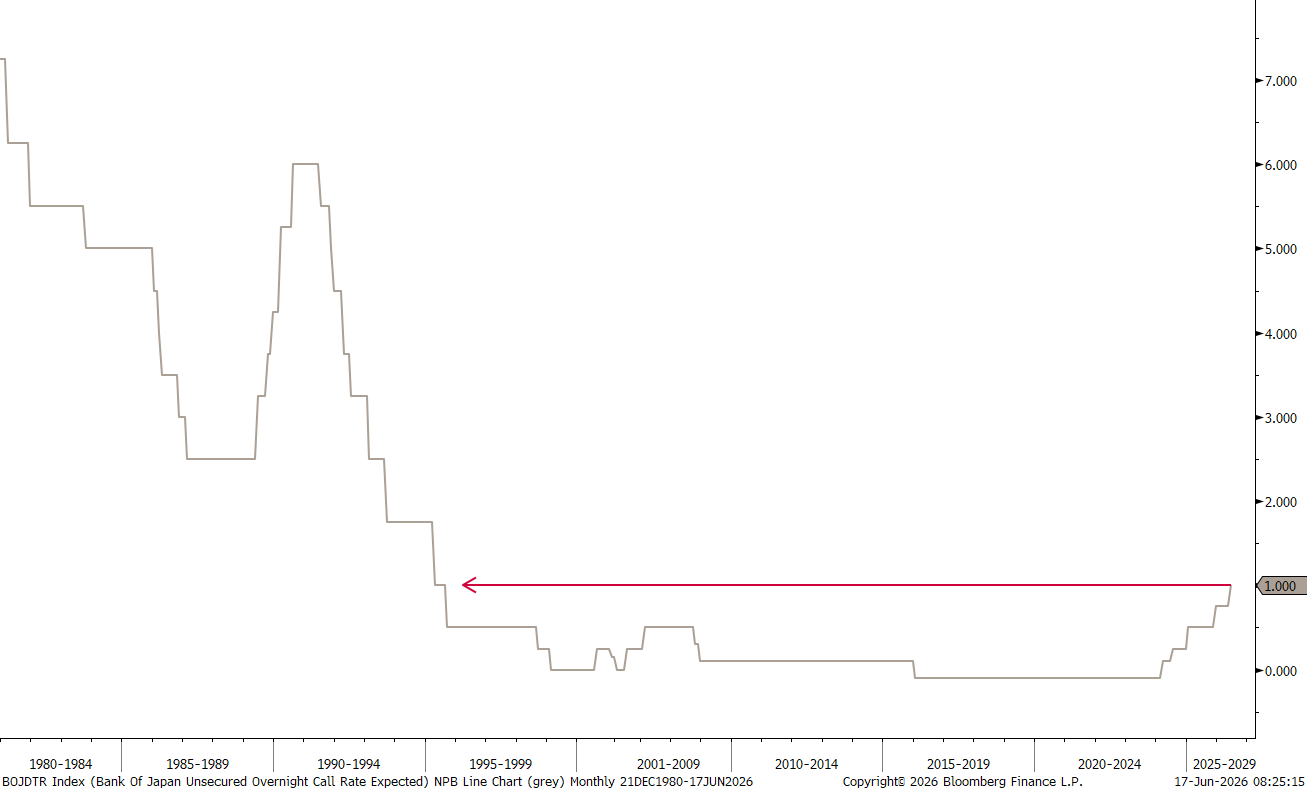

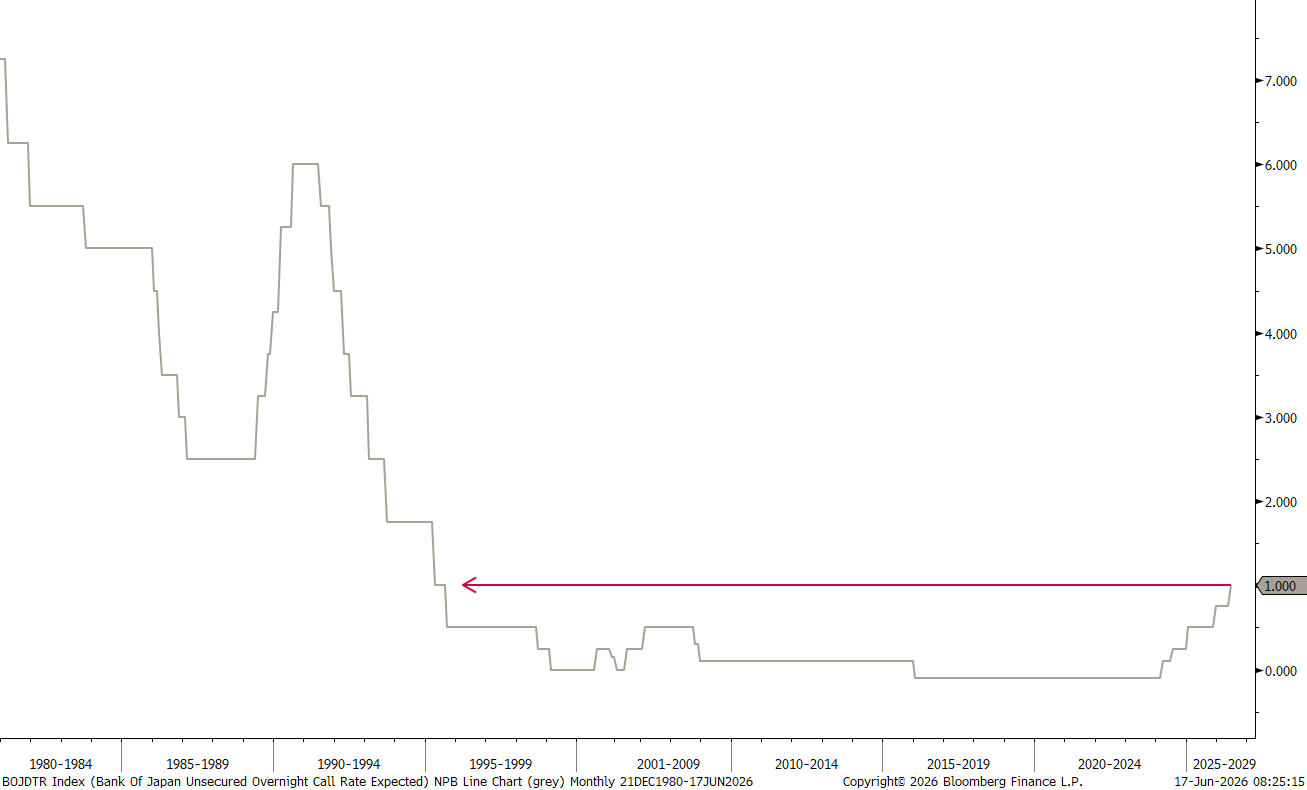

Coming into an (IT-related) time crunch, let me just highlight yesterday’s decision by the Bank of Japan (BoJ) to increase rates by 0.25% to 1%, with two comments.

Whilst a policy rate of 1% does not sound like a lot, it is the highest since 1995 (that’s 30-years+ for you):

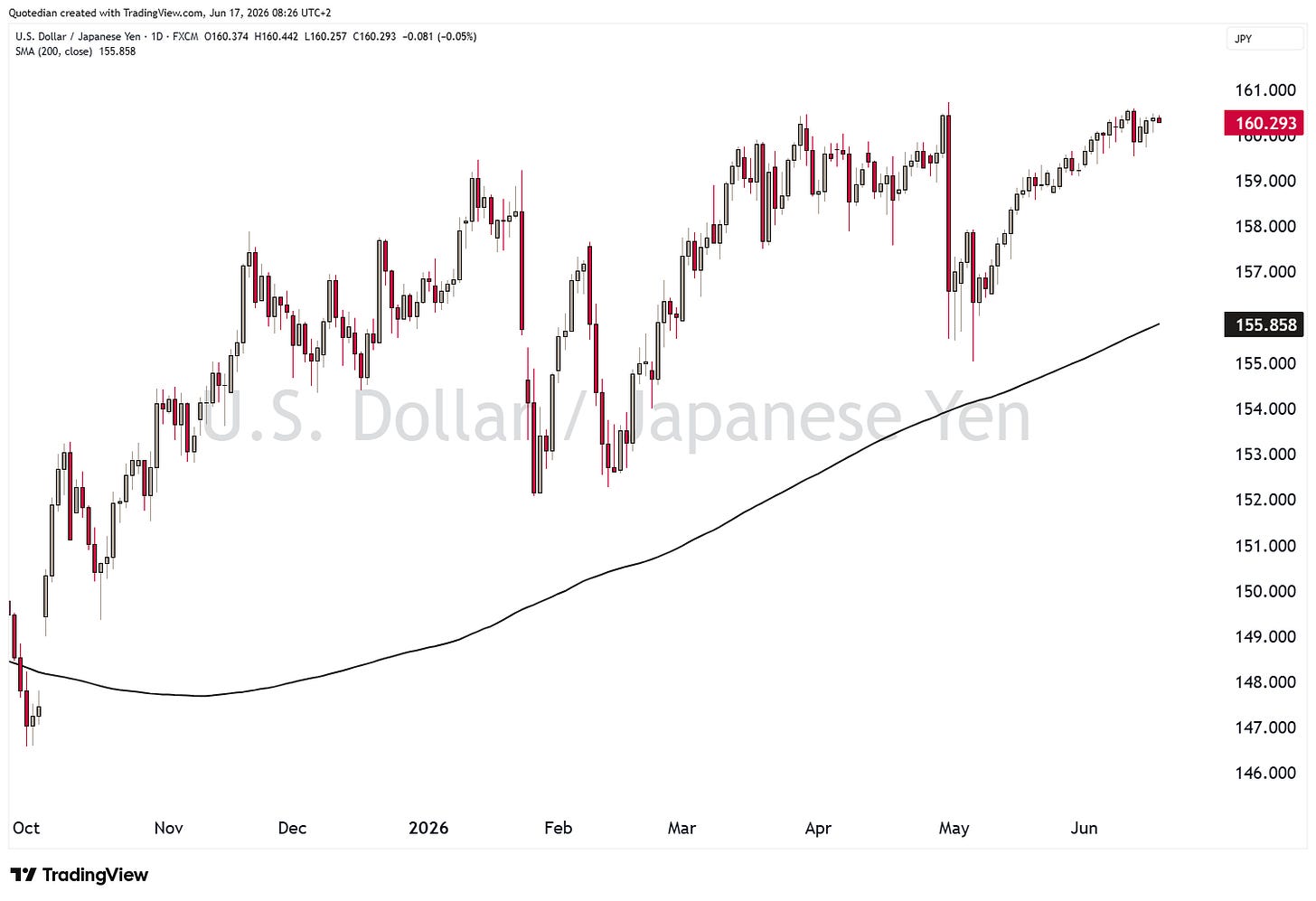

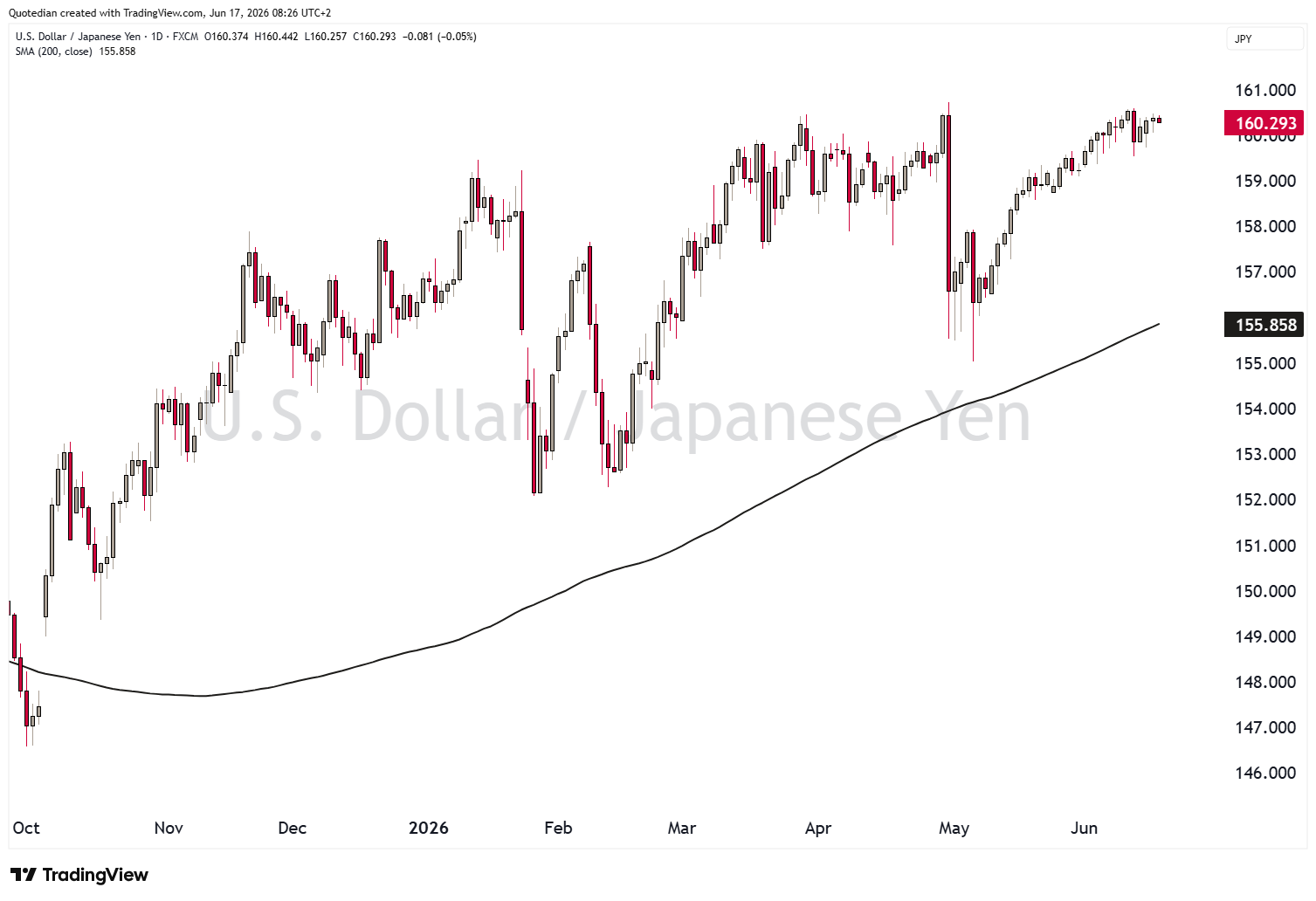

That rate hike helped exactly ZERO to strength the Japanese Yen, which continues to hover around BoJ/MoF intervention levels at 160:

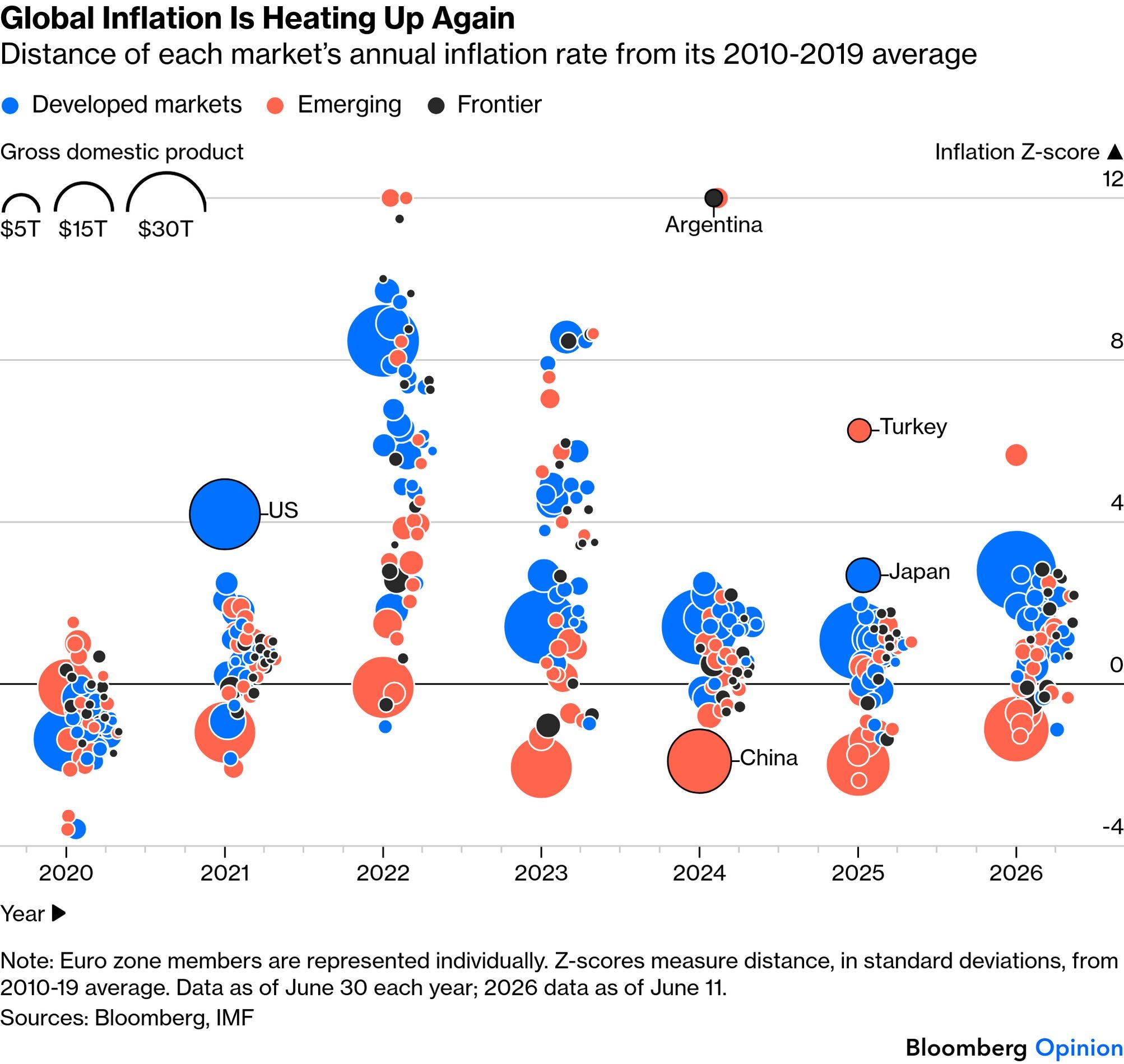

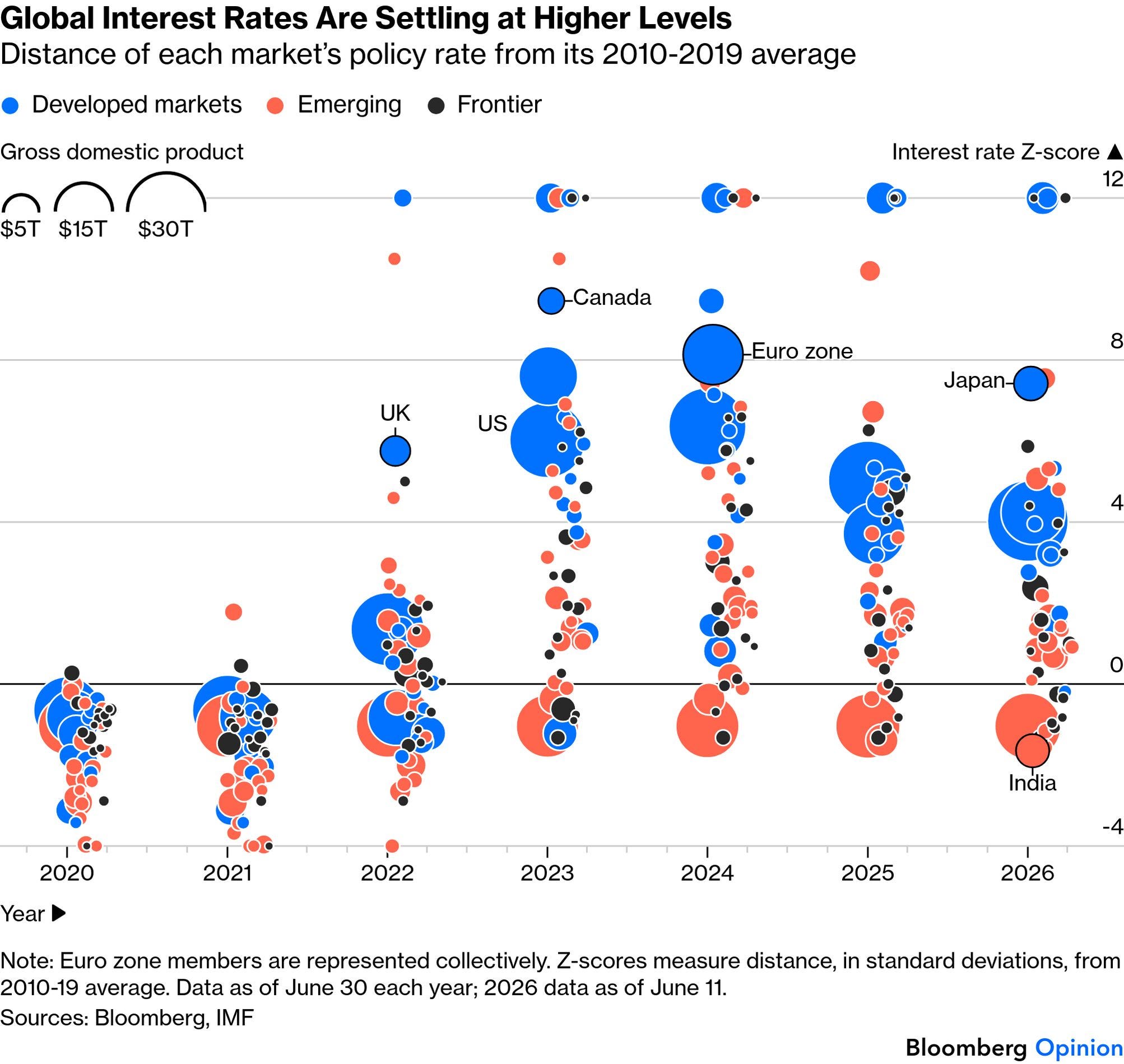

Two very illustrative charts on inflation and global interest rates from John Authers at Bloomberg. I do not think a lot of additional explanation is needed here.

On inflation around the Globe:

And on Global Interest Rates:

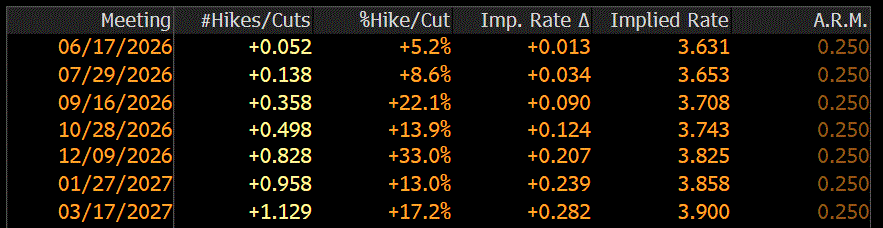

For today, all eyes on Mr Warsh’s post-FOMC press conference, which will likely turn out to be a big, fat nothing burger. With the Iran conflict largely out of his way now, there will be little need for hawkish talk, which might have upset Uncle Donald.

Clearly, no hike is expected:

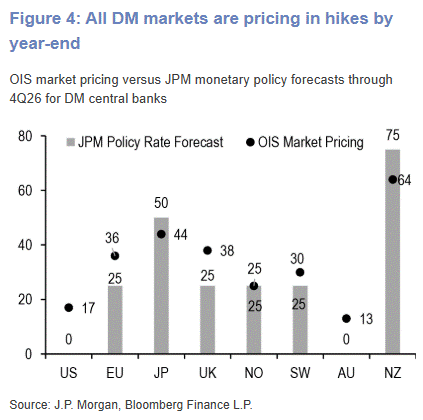

But equally clearly, the easing cycle has ended, not only in the US,

but for developed markets around the globe:

That’s all for today - apologies for the shortened version - but … dog ate my homework IT was a struggle this morning.

Andr

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG