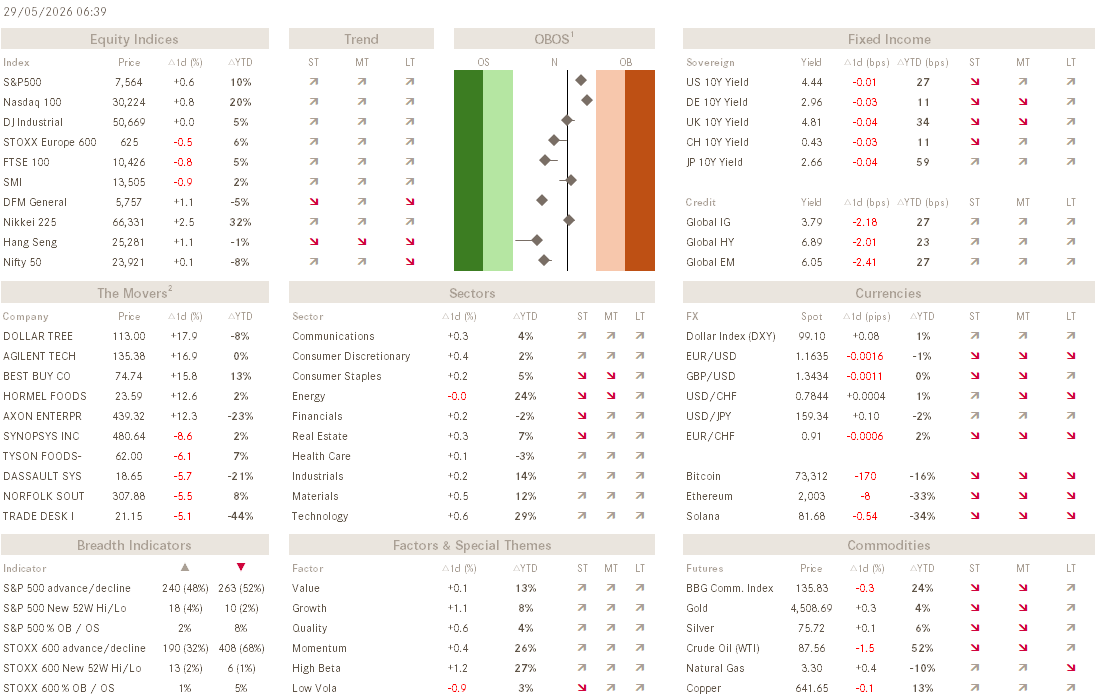

The Q - Daily Edition

Too Late to Buy, Too Early to Sell

"By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens."

— John Maynard Keynes

Is the zig-zaging and the Tuesday TACOing finally coming to an end? Bloomberg’s top headline this morning reads:

“Stocks scaled to a record and oil dropped after the US and Iran reached a tentative deal to extend their ceasefire, pending President Donald Trump’s signoff.”

To which the equity market probably would reply with a sarcastic: “No shit!”

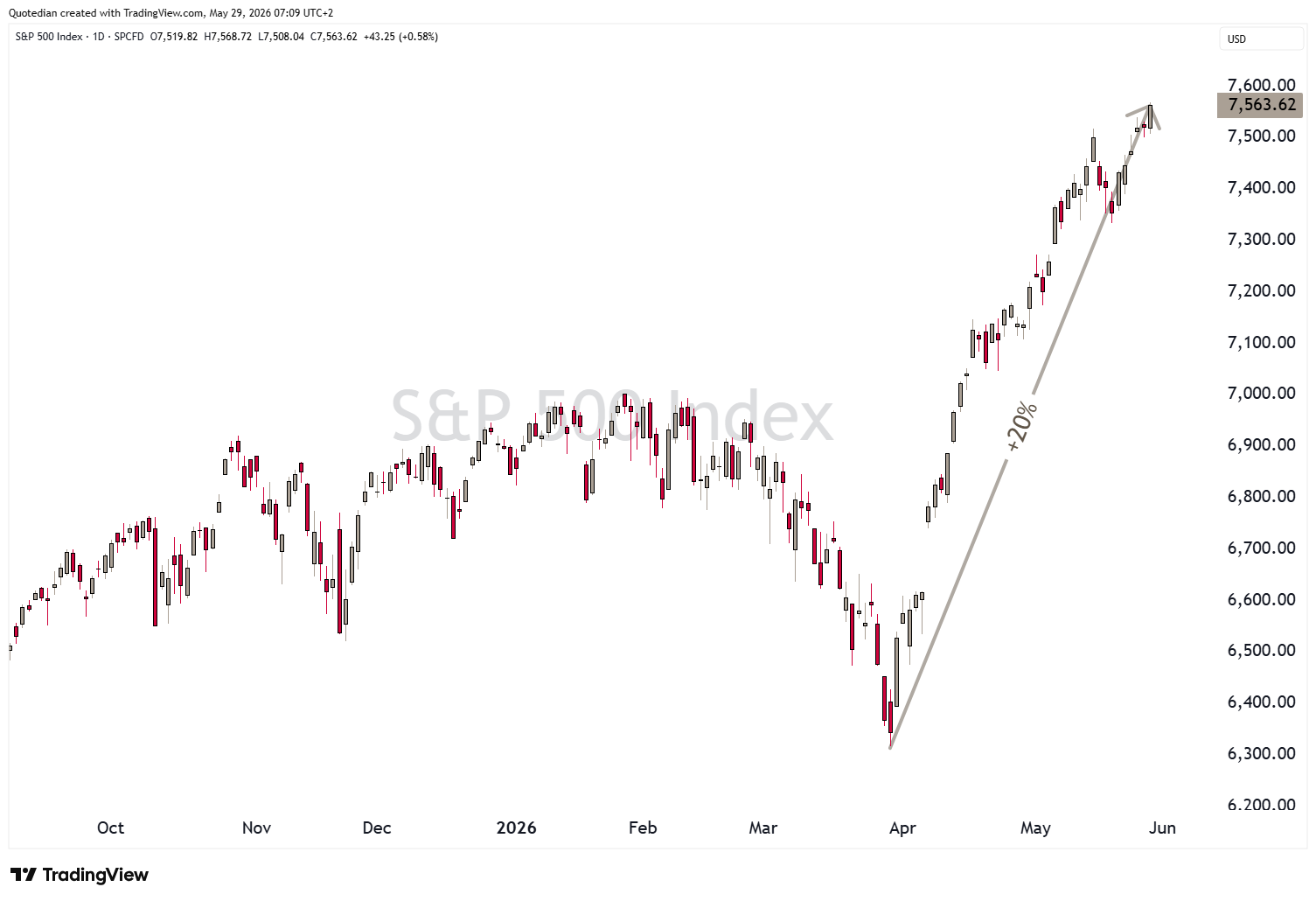

Up nearly 20% in since early April and hitting a new all-time high yesterday, I think it is safe to say that the global investor already decided a while ago that such a deal would be reached.

But it was not only the largest cap indices such as the S&P 500 (below), the Nasdaq or the Dow Jones Industrial in the US, all reaching new ATHs yesterday,

but also smaller cap stocks,

but even more importantly from a European-focused investor’s point-of-view, local indices such as the DAX are about (today?) to do the same:

Meanwhile, the market safely ignored a warning from ExxonMobil that oil inventories will fall to record lows in the coming weeks, possibly pushing oil prices as high as $150 per barrel.

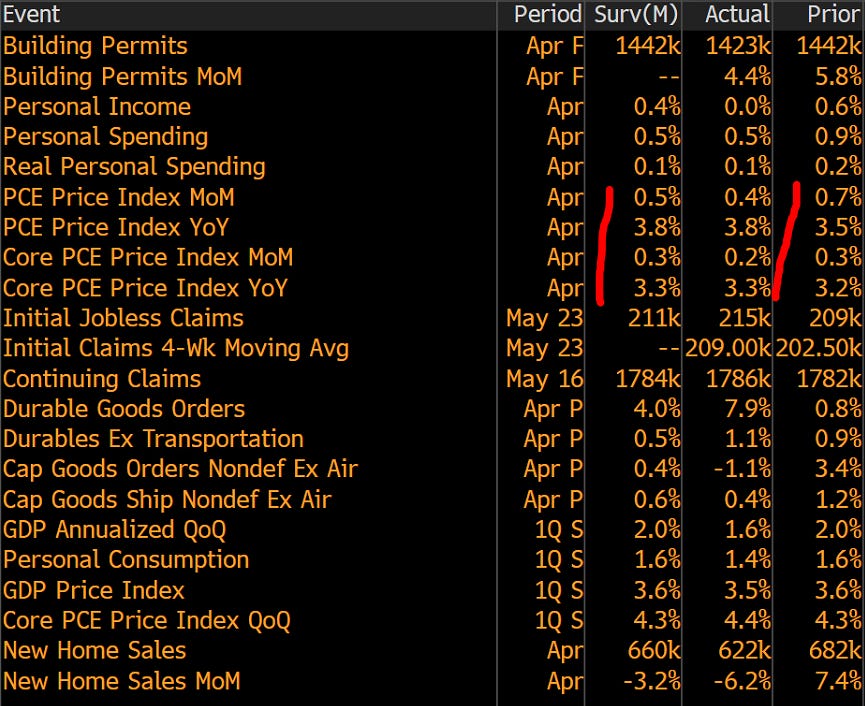

Also, the market “thinks” that yes, inflation readings are higher (PCE yesterday), but are in checkers and even slightly less then assumed by those infallible economists:

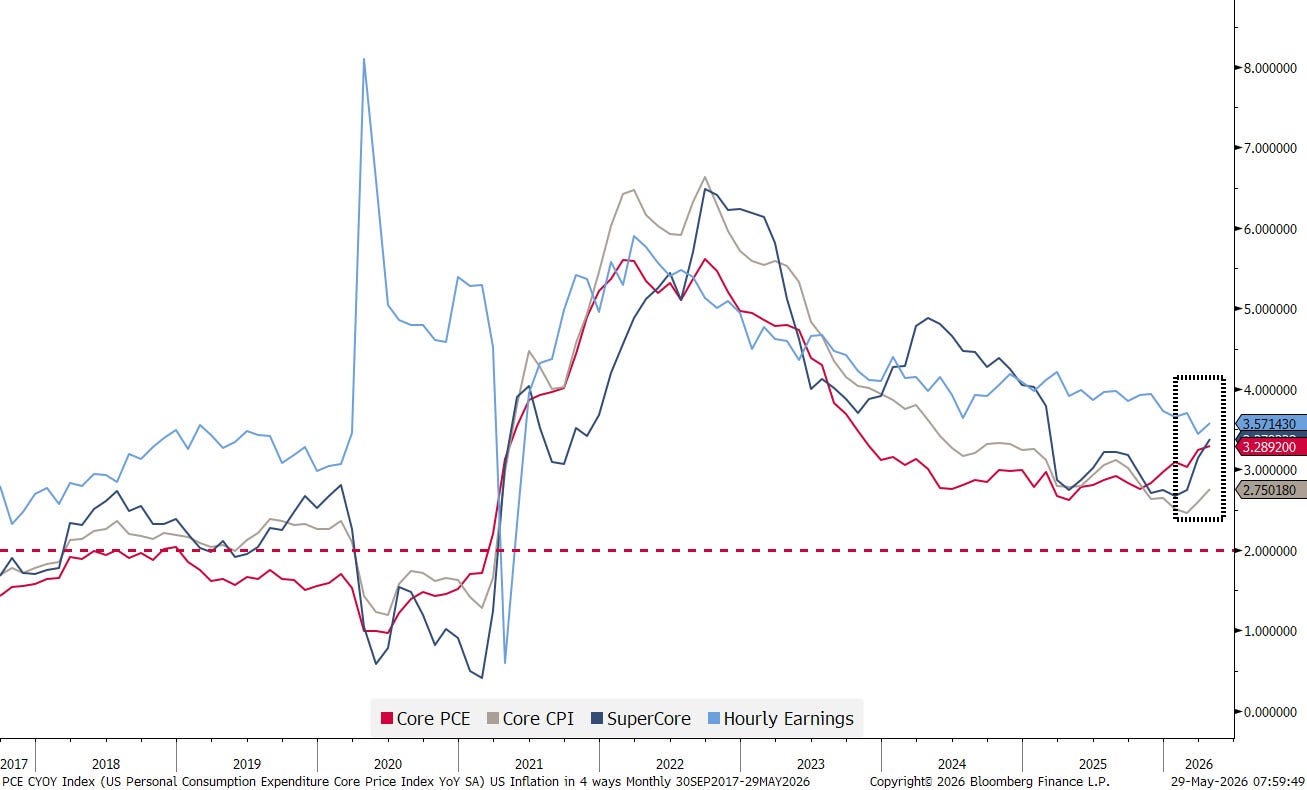

But the longer-term point is that inflation has not gone back to the Fed’s target rate in over five years and has started heading the wrong direction again:

But even the bond market ignored that yesterday:

There’s a good chance for bond prices moving higher over the next few sessions, with a yield target of around 4.35-ish.

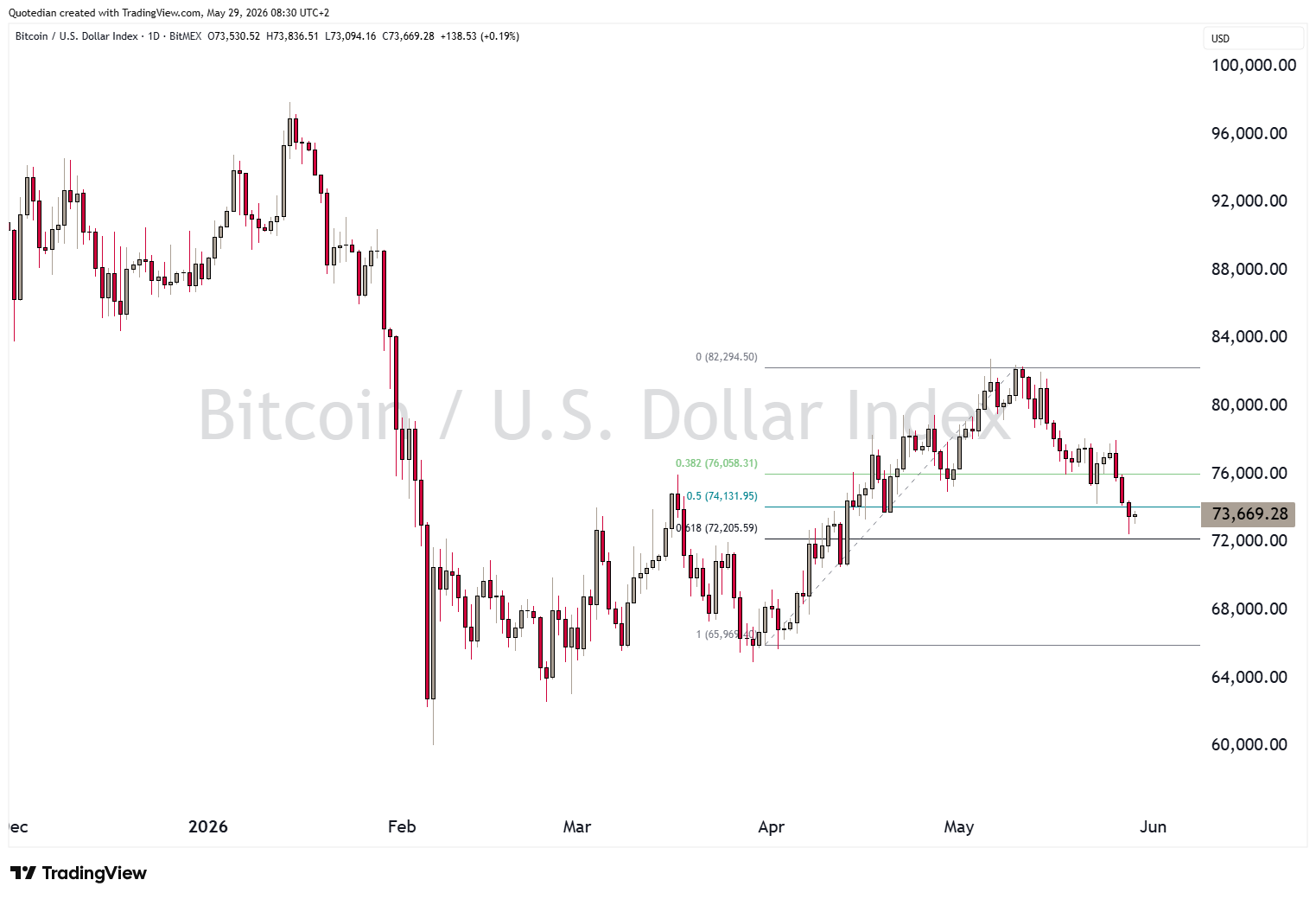

Nothing specific happening on the (fiat) currency side, but maybe worth highlighting that Bitcoin should hold above 72,000, otherwise the technical picture de-proves substantially:

Gold, despite this morning’s bounce, is also somewhat under pressure, with 4,370 the clear line in the sand for the bulls (and the bears):

Stock markets are hitting new ATHs and some segments are seeing frothy valuations and even frothier investors animal instinct behaviour. In my view, a violent correction over the coming weeks (mid-June?) is becoming a likelihood.

HOWEVER, yesterday saw the Value Line Geometric Index (VALUG). an index widely viewed as a gauge of the median stock's performance, break out to new all-time highs:

Translated this means that breadth is broadening, i.e. more stocks are participating in the rally and is further supported by recent breakouts in the equal-weight indices of the S&P, the Nasdaq and the Dow.

SO…

Should we get that correction over the coming weeks, gather all your courage and BTFD!

Really nothing to highlight from the economic calendar today, with maybe the exception of German regional and nationwide inflation numbers being released.

There is a high likelihood of NO daily updates next week, but there should be a Weekly Quotedian out on Monday morning. So, check your inbox for that and if you have not yet signed up to the original, weekly Quotedian… shame on you!

May the Force be With Me.

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG