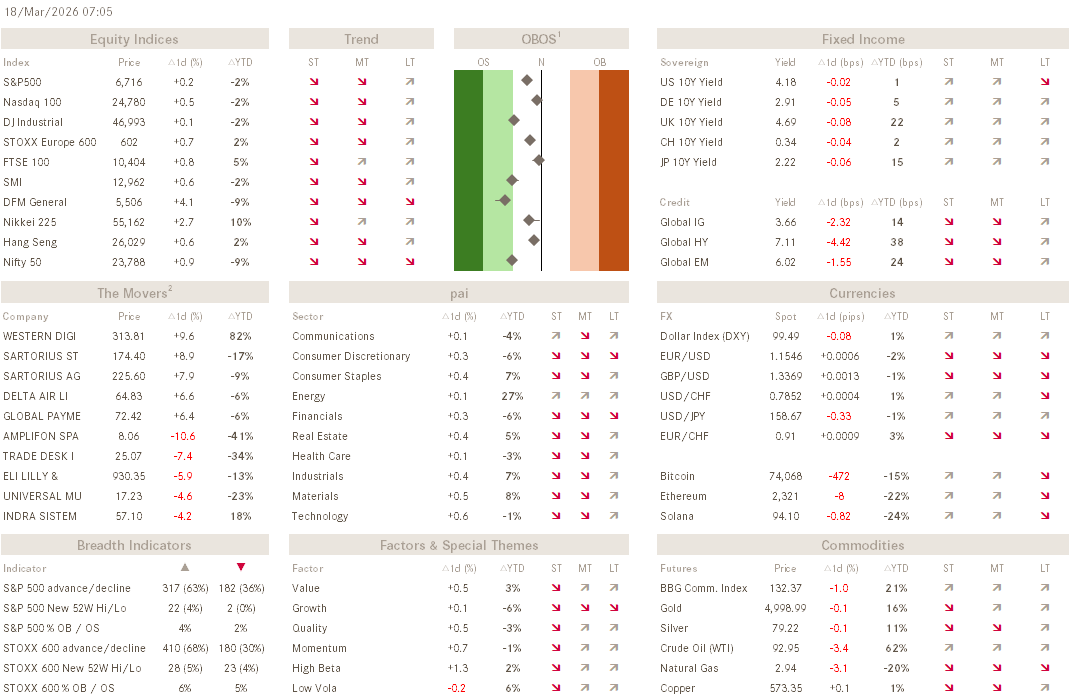

The Q - Daily Edition

Dire Straits

"In the midst of chaos, there is also opportunity."

— Sun Tzu

Despite the oil price (Brent) spiking higher yesterday and clocking in a closing high for this cycle,

equity markets actually showed a shy risk-on behaviour as you can see from our daily cockpit above. Given that oil prices meanwhile have reversed lower, that shyness was able to swap over into Asian equity markets (and Western index futures), with strong advances noted across the region but more accentuated in places such as Japan (Topix +2.5%) and Korea (KOSPI +5%).

This latter index is looking VERY constructive already again:

FOMO anyone?

Was Israel’s killing of two Iranian leaders, Larijani and Soleimani enough to make the market think we may be in for a closing of the conflict. Perhaps.

Or is it the famous notorious “The Economist”-contrarian-magazine-cover-indicator that once again is working its ‘magic’?

At least for today, risk-on seems to continue for the next few hours.

Sharply lower bond yields (UST10y) over the past three sessions,

and a mildly lower USD (index), having been rejected at major resistance,

support that risk-on notion.

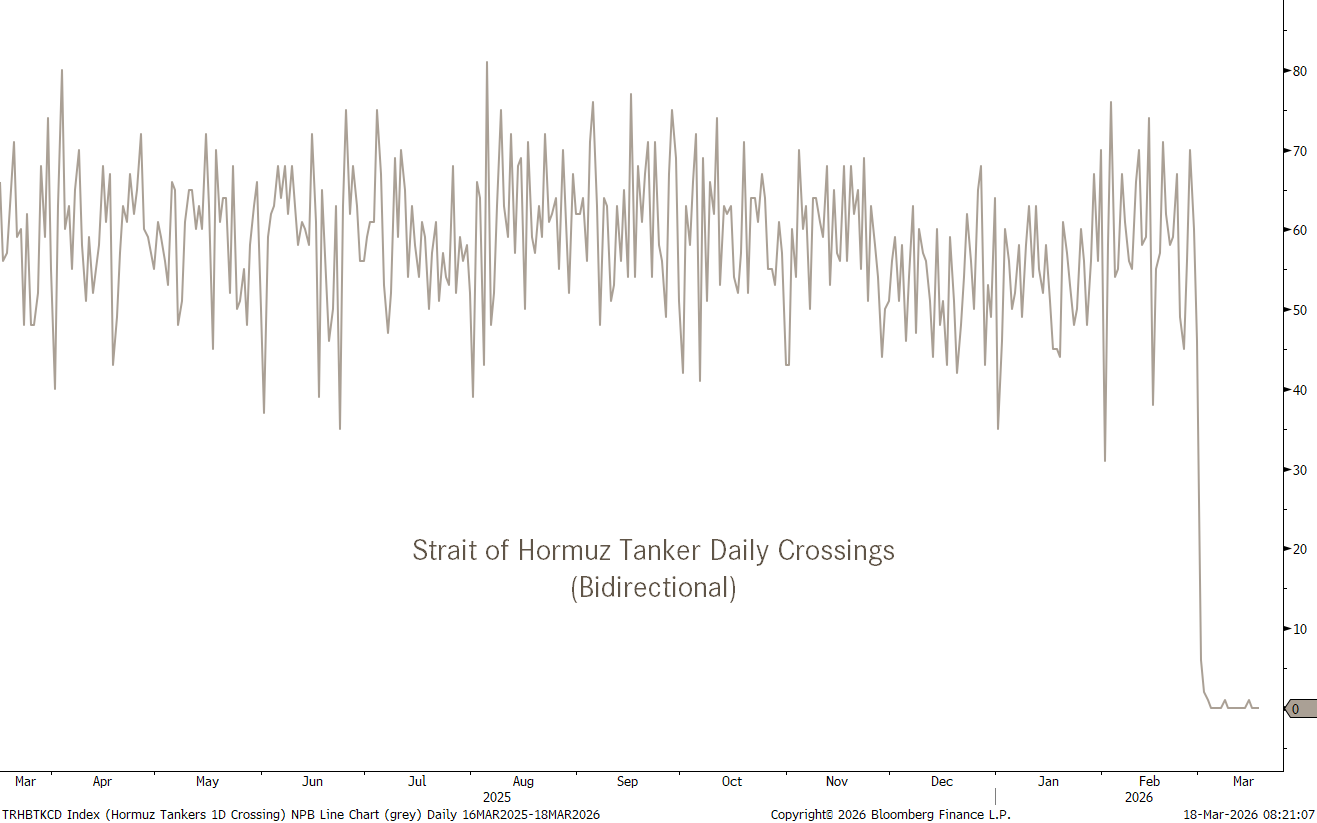

That’s still not an awful lot of tankers going through that Strait!

A busy day today, with the Fed’s FOMC interest rate decision (no change), but especially the presser of focus. But also noteworthy is that Trump is meeting Japanese PM Takaichi tomorrow. Agenda: Strait of Hormuz. Whilst Takaichi is constrained by constitutional limits and 82% public opposition to the war, any joint-intention agreement could still be a major shift on the global political chessboard. Stay tuned …

SECO Economic Forecasts — morning CET. Swiss govt quarterly outlook update

Eurozone CPI (final, Feb) — 10:00 CET / 05:00 ET. Headline exp. 1.9% YoY (flash 1.7%), Core 2.4% (prev. 2.2%). Re-acceleration watch

German 30Y Bund Auction — morning CET. Previous yield 3.47%

US PPI (Feb) — 08:30 ET / 13:30 GMT. MoM exp. +0.3% (prev. +0.5%), Core MoM exp. +0.3% (prev. +0.8%). Key CPI pipeline read

BoC Rate Decision — 09:45 ET / 14:45 GMT. Exp. hold at 2.25%. Press conference follows

US Factory Orders (Jan) — 10:00 ET / 15:00 GMT. Exp. +0.1% (prev. -0.7%)

EIA Crude Oil Inventories — 10:30 ET / 15:30 GMT. Exp. -1.5M bbl (prev. +3.8M). WTI ~$92, Brent ~$101

FOMC Rate Decision + Dot Plot + SEP — 14:00 ET / 19:00 GMT. Exp. hold at 3.75%. Updated economic projections & rate path — the main event

FOMC Press Conference (Powell) — 14:30 ET / 19:30 GMT

Brazil Selic Decision — after US close. Exp. cut to 14.50% (prev. 15.00%)

Earnings - Micron & Five Below

That’s all for today - May the Trend be with You!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG