The Q - Daily Edition

Telltale Sign

“Is there any other point to which you would wish to draw my attention?”

“To the curious incident of the dog in the night-time.”

“The dog did nothing in the night-time.”

“That was the curious incident.”— Arthur Conan Doyle, Silver Blaze

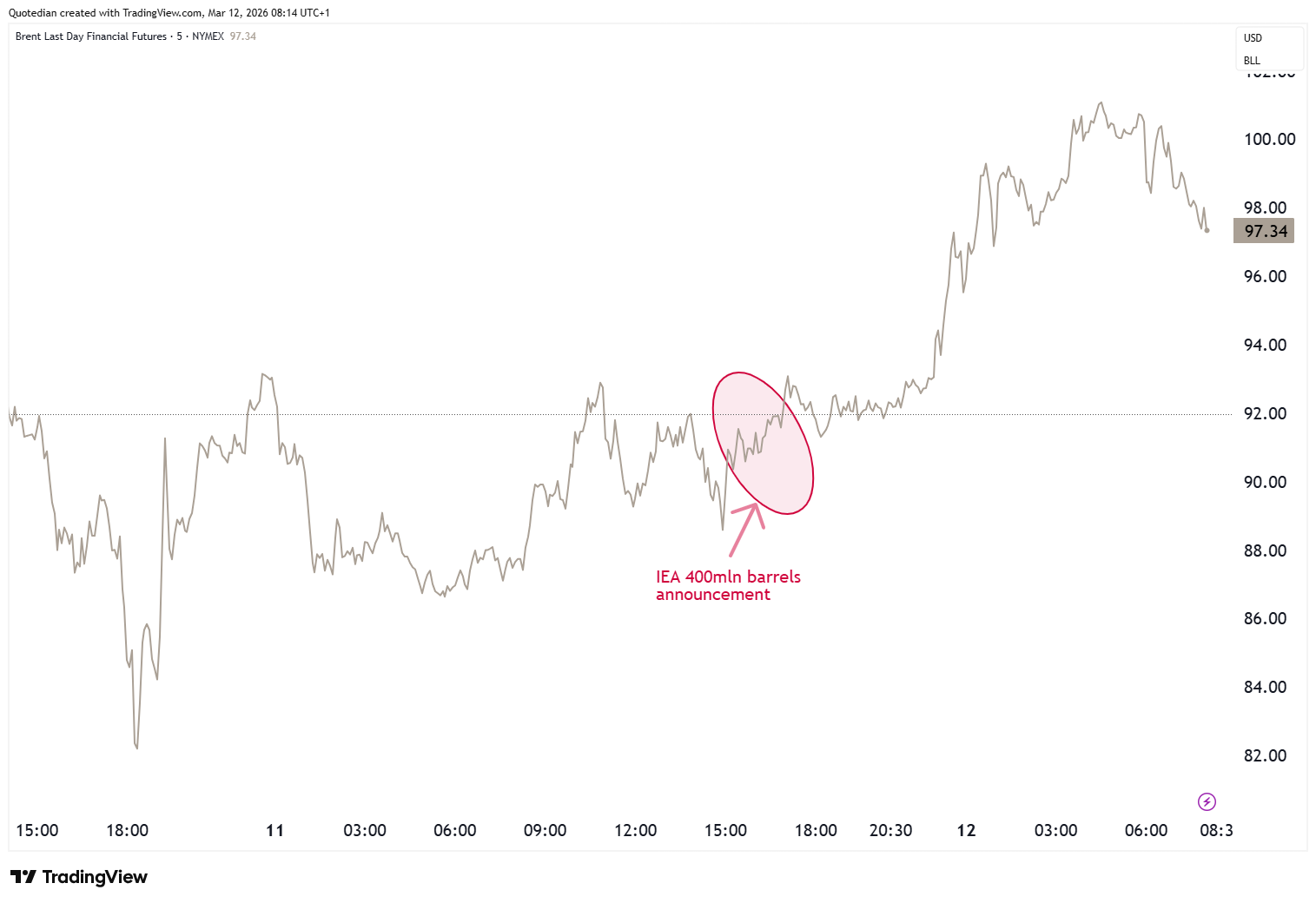

The effective closure of the Strait of Hormuz has removed approximately 20mbd (million barrels daily) of oil from the global market.

Yesterday, the 32-member countries of the International Energy Agency (IEA) unanimously approved a coordinated emergency oil release of 400 million barrels, the largest in its 52-year history, to “counterweight” that supply shock.

This means that the IEA is providing 20 days' worth of relief oil supplies and implies that the group expects a short war.

The telltale sign is that the price of oil (Brent) did not nudge to the downside, but later in the session rather shot up another ten Dollars or so:

As one analyst put it:

“The flow vs the lack of physical supply in Asia already looked like a plaster on a shotgun wound.”

And this was before Iraqi ports were taken offline, which is, expanding on the metaphor above, another cartridge fired into the same injury.

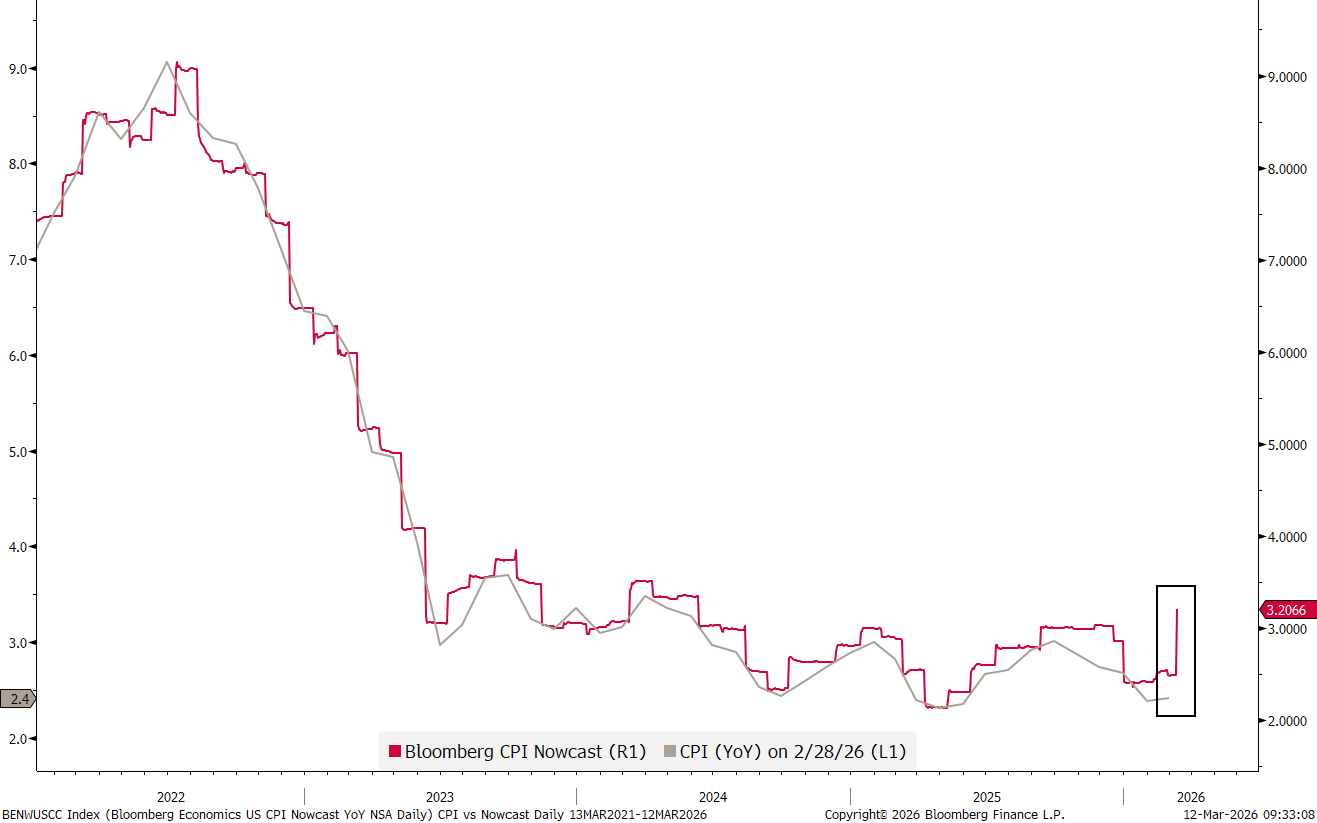

On another note, US CPI (consumer price inflation) was reported yesterday, and either nobody noticed or nobody cared. In any case, as you know, I de-test this super-lagging, even more super-manipulated economic ‘indicator’, but for completeness purpose, this is what the numbers looked like:

All bang-on inline, but, of course, this numbers do NOT include the recent increase in energy (and food prices - see below), but will do so starting next month. So, doubt not, that this number will be very closely watched again next month and even more so the few months following thereafter.

Here’s another telltale sign (aka spoiler alert) for those upcoming CPI reports:

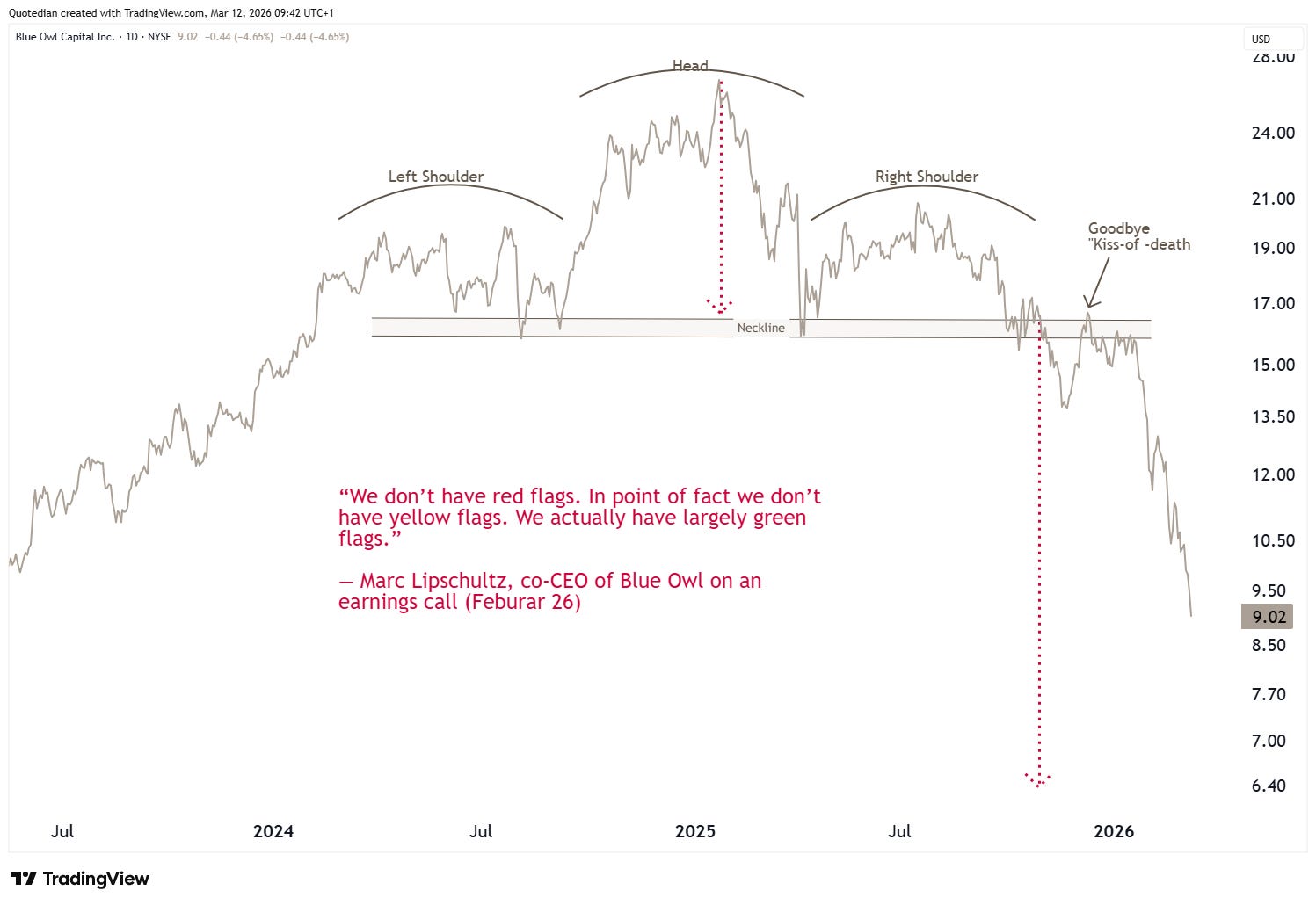

And then we have to talk private credit again … click here and here for previous conversation …

Yesterday, JPMorgan (of Jamie Dimon's “Cockroaches” fame) began marking down the value of loan portfolios held by some private credit groups, specifically those exposed to software companies that may face existential risks from AI.

Why did JPM do that? Because they can. But it will impact many of their other peers competitors.

Blue Owl, one of those major peers competitors is down now 45% since we highlighted that possibility back in early October. And, remember that technical analysis voodoo chart from a few weeks ago?

“Only” another 30% to go to our initial price target…

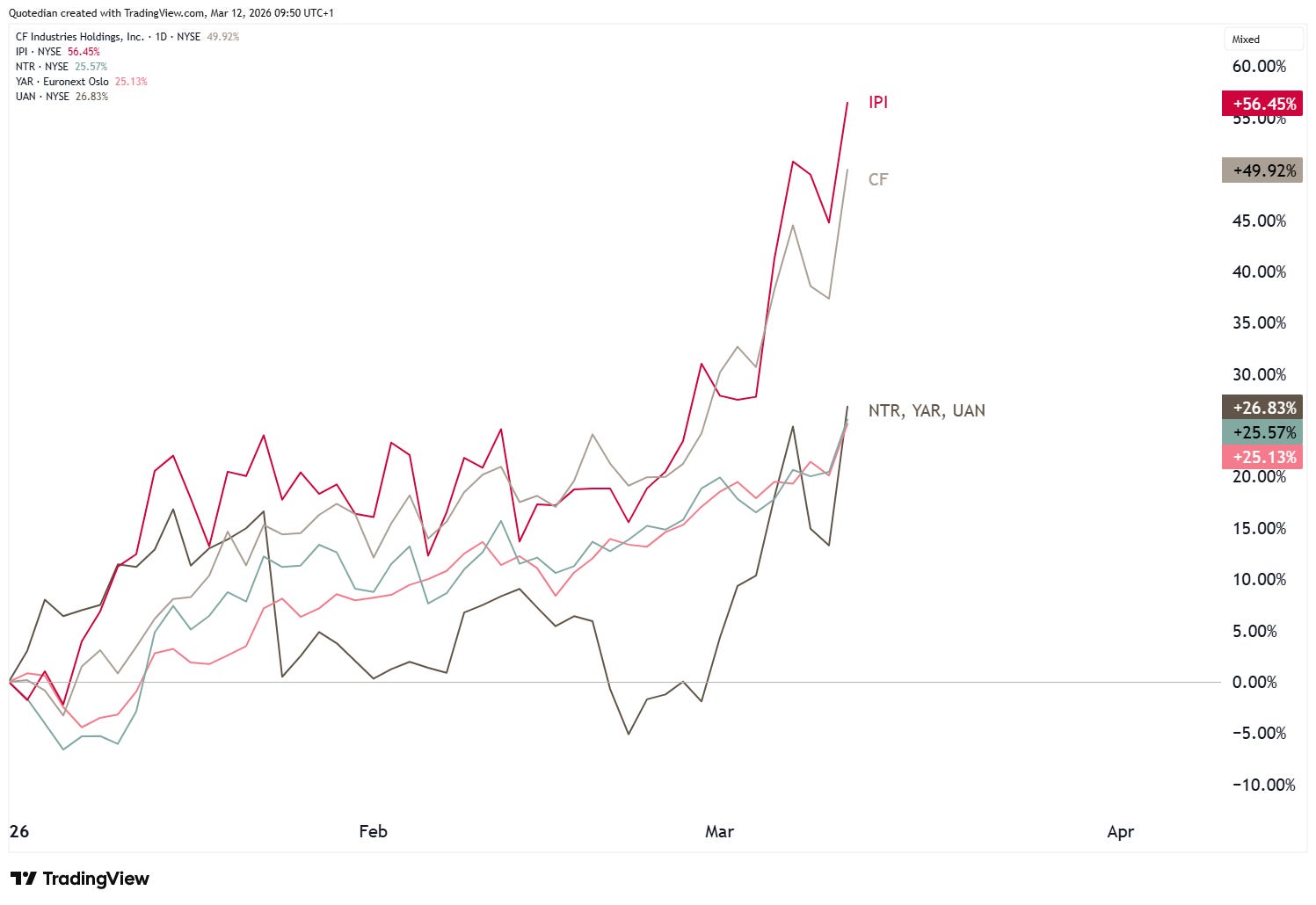

Lastly, we need to talk fertilizers … having set-up the investment office of a family office for a major fertilizer producer a few years ago, I know a thing or two about that. No secret here, but energy (Gas) is a major input into fertilizer production. Wonder why then everybody only speaks about the oil stocks going parabolic …

Due to some technical issues today (and yesterday, sigh) I have to cut today’s letter short here, but also, there’s simply too much going on to cover everything in just one daily letter, so my mission is to try to highlight some of the most interesting and hopefully critical/meaningful points in the daily edition of The Quotedian. As I am not quite prepared yet though to publish a “The Quotedain - Hourly Edition”, I will try to pack as much as I can in the next weekly edition, with the working title (spoiler alert): “Damage-Control Reports, All Stations!”.

If your are not signed up to our weekly newsletter, make sure to do so right now:

Is the private credit fall-out swapping over into the public/listed bond market? The chart below answers that question with a crystal clear: Perhaps.

The top clip shows the ratio of a investment grade bond ETF (LQD) to a Treasury bond ETF (IEF). It suggest that a breakdown may be occurring.

The bottom clip shows the ratio of (US) financial stocks (XLF) to the broader market (SPY). It demonstrates that financials have been underperforming for the past nine months and may just be breaking down again.

Stay tuned and may the Trend be with you!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG