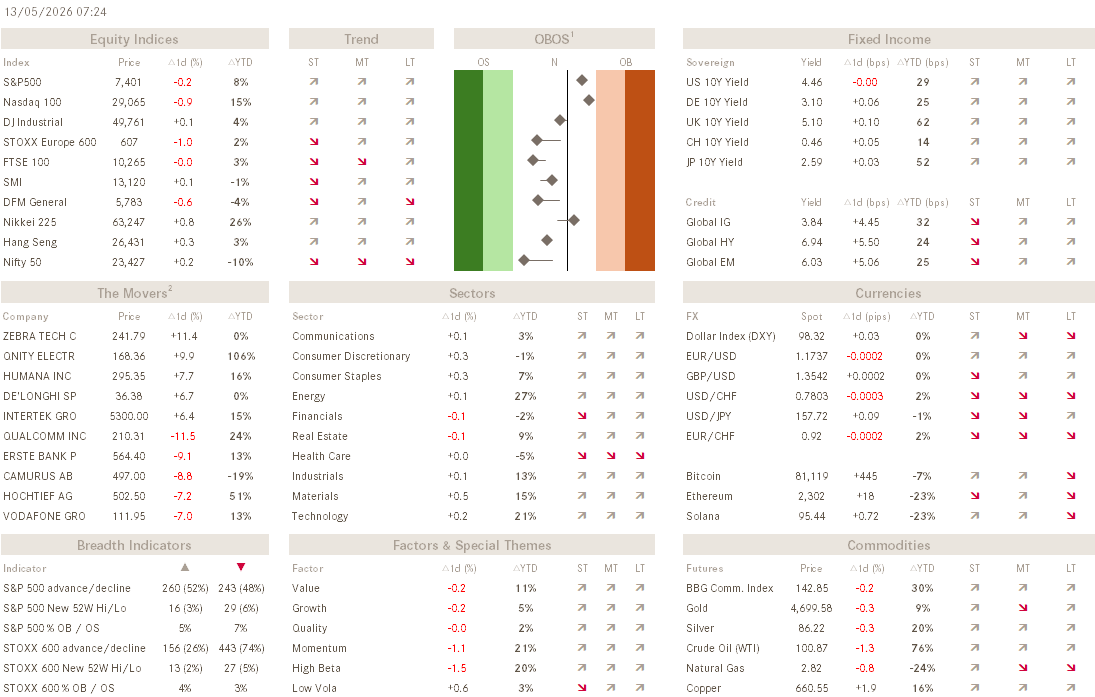

The Q - Daily Edition

The Writing on the Wall

Mene, Mene, Tekel, Upharsin" — "Numbered, numbered, weighed, divided. You have been weighed in the balances and found wanting."

— Book of Daniel, Chapter 5

** Housekeeping **

This is likely to be the only Daily Quotedian of this week as your editor is heading into a well-deserved, long weekend. Back next week with weekly and daily editions.

Just a few random observations today, starting with yesterday’s US inflation report where the Core CPI number “beat” expectations:

Which is really a bit sarcastic, considering the Core CPI strips out food and energy costs, arguably the two items facing most upside pressure of the coming month from higher oil/gas and fertilizer prices …

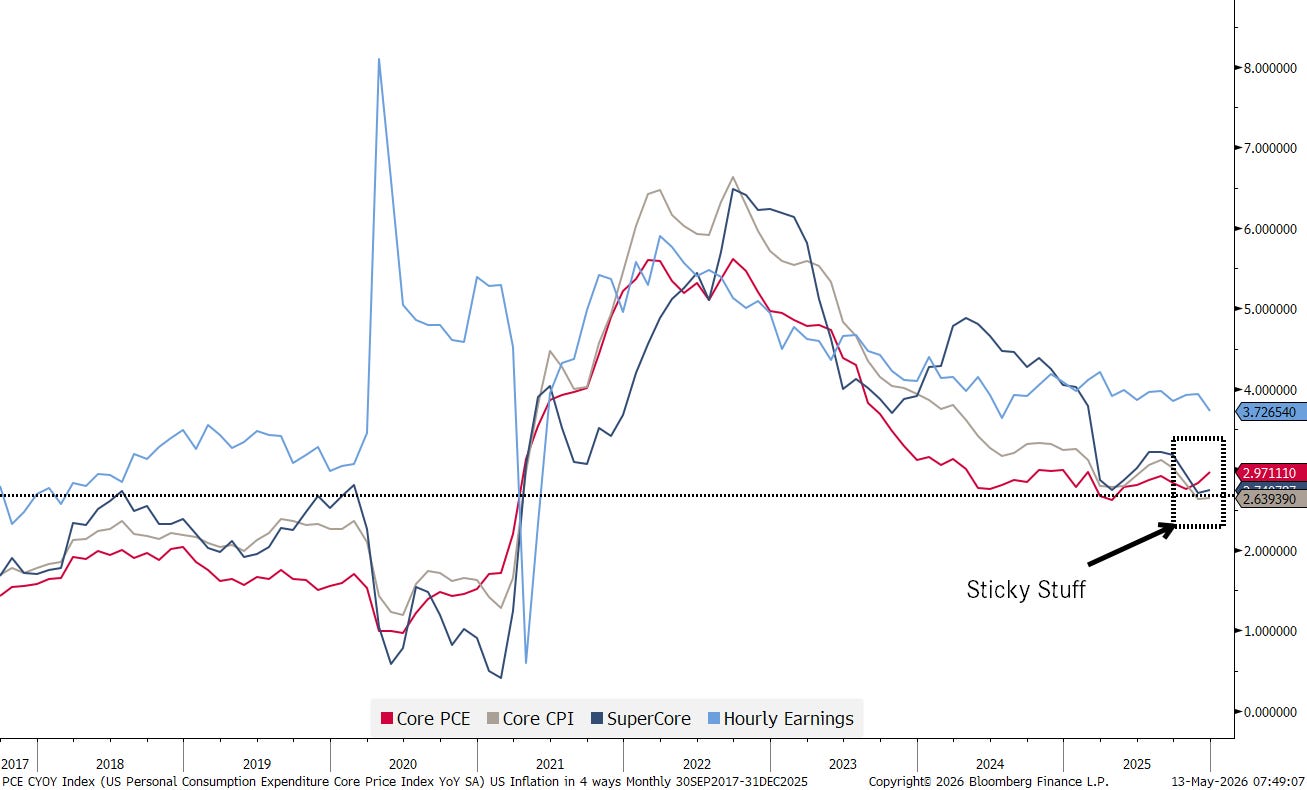

But, however government tries to slice, dice and hide it, inflation is picking up again, except in average hourly earnings (which kind of reinforces the stagfkation argument again:

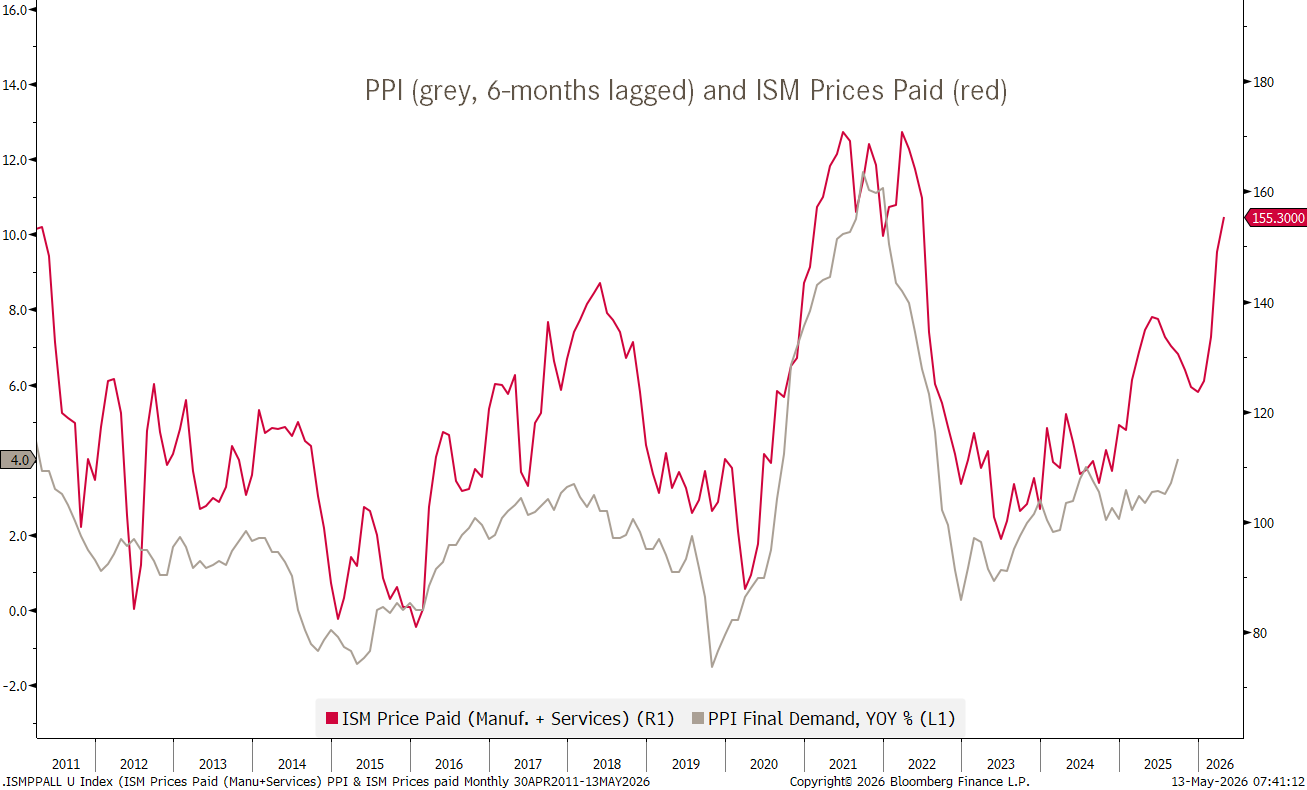

Later today we will get the Producer Price version of the inflation number, where a noticeable pick-up is expected:

Hence, let’s keep this chart in mind, which we have been following together for a few weeks now:

Please note that this chart above is not “chart crime”, even though it uses two different y-axis, because I am warning you of the potential “chart crime”. The importance on the chart above are a) lead and b) direction of the red line, not magnitude.

Onwards…

Nearly simultaneously with the release of the inflation numbers was Mr Ethan Hunt Kevin Warsh confirmed by the Senate as governor of the Fed. A Fed that is expected by one particular US president to lower interest rates, higher inflation or not… Mission Impossible?

Confirmation as next chairman of Mr Hunt Warsh will almost certainly follow later this week.

Some market observations from yesterday …

Semiconductor stocks FINALLY came under pressure … for a few hours:

The S&P 500, which admittedly dropped ‘only’ one percent top to bottom, unlike the SOX above, where the sell-off was in excess of five percent, made nearly the full round trip by market close and has gained additionally in after-hours futures market trading:

Asian stock markets are trading mostly higher this morning, with Japanese and Chinese Mainland stocks leading. One market worth mentioning however, is the Indian stock market, which while flat today has given back nearly five percent over the past few sessions:

The underperformance versus the wider Asian region is becoming very pronounced:

In bond markets, not a lot of good is happening, as yields are moving higher again (we highlighted our suspicion this would happen in our latest weekly Quotedian “To Infinity And Beyond”). The US 10-year yield is at its highest since last July,

and on the longer-term chart is approaching the upper end of its consolidation triangle:

UK 10-year Gilts are at their highest since 2008 on the back of a political starm(er) storm:

Fun fact: Over the past 10 years the UK had six different prime ministers (and possibly a new one in the making right now); Italy had five.

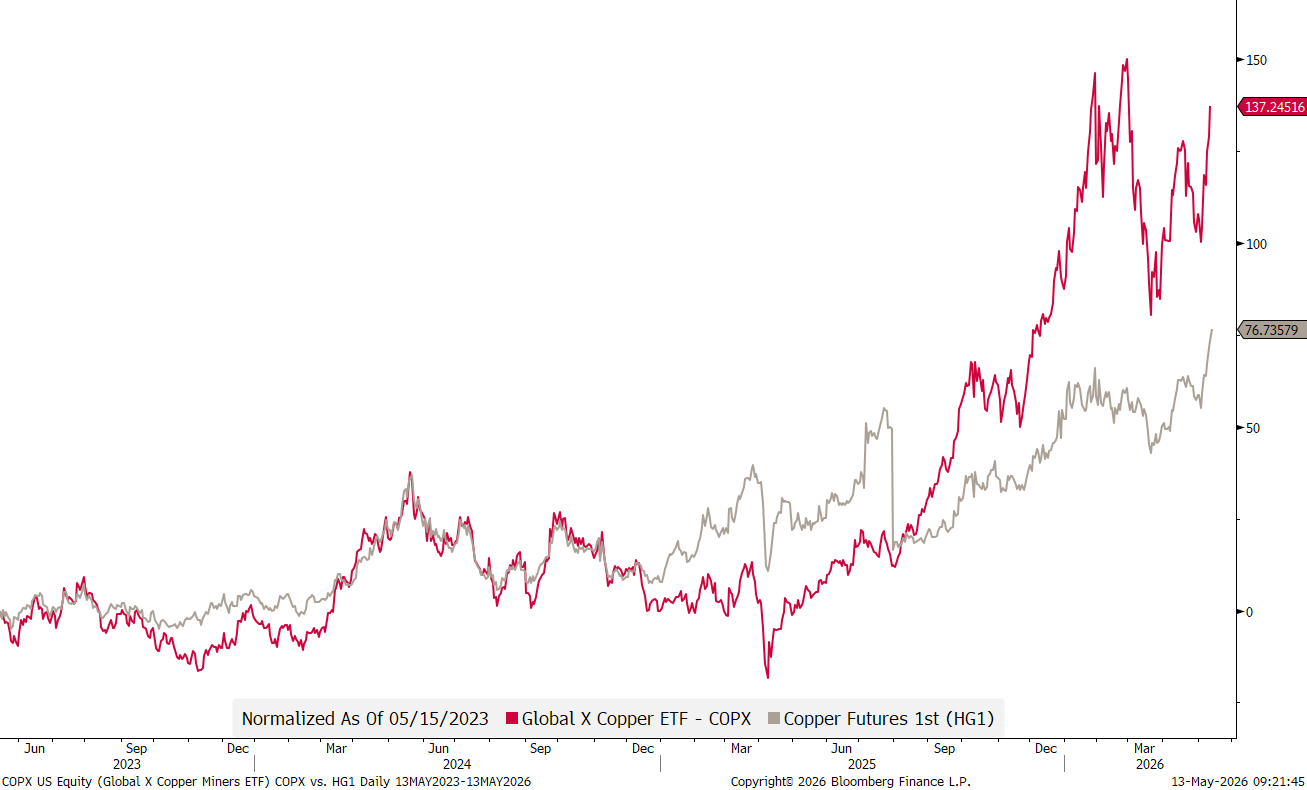

Finally, the copper trade we have been touting seems to be working well already. Here’s the chart of copper futures (1st):

Our preferred mean to invest, for those who cannot hold commodity futures in their portfolio, continues to be the Global X Copper Miner ETF:

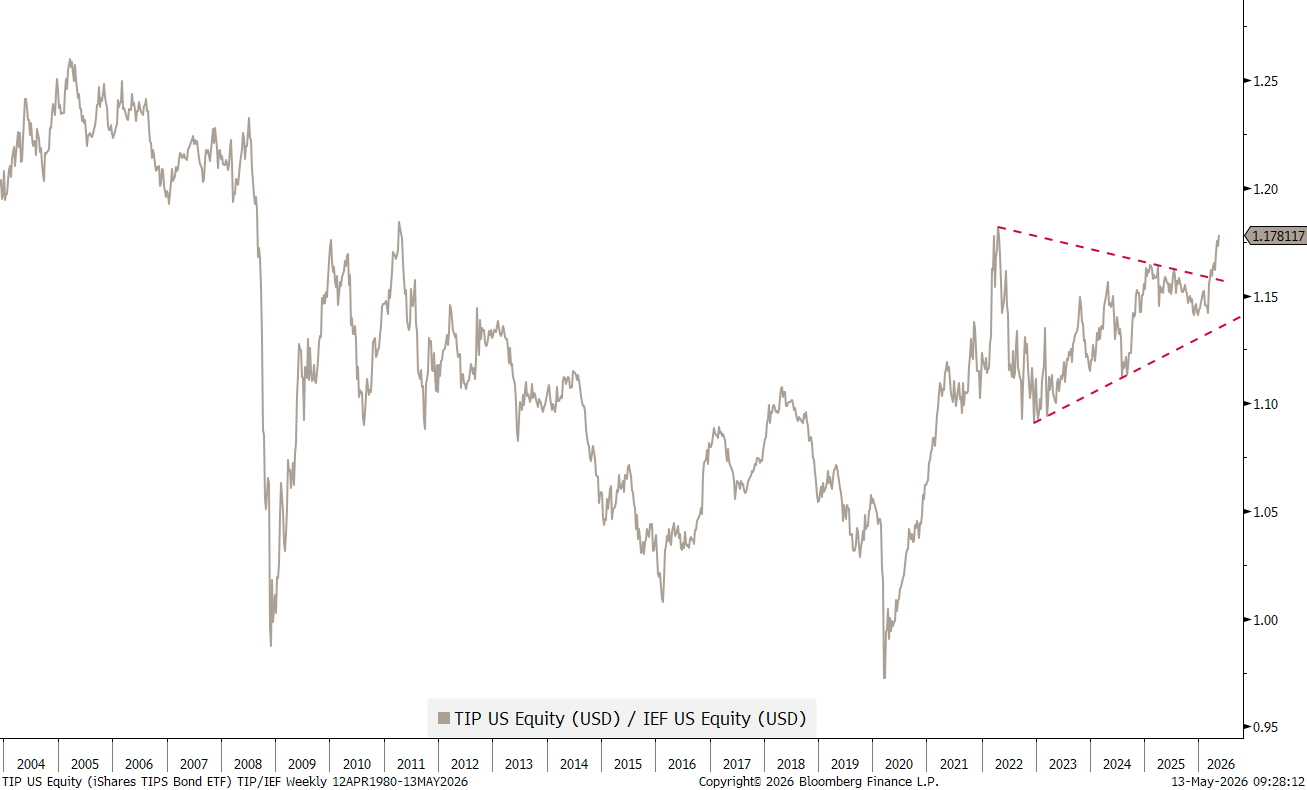

Really like this chart. It shows the ratio of iShares TIPS ETF (i.e. inflation-linked bonds) to the iShares 7-10 Year Treasury Bond ETF (i.e. nominal bonds).

The ratio is rising, having broken out of a clear multi-year triangle (red dashed) and now trading at the highest since 2022 (remember what happened back then to inflation?).

In my most simple interpretation, this means that investors are giving preference of inflation-protected bonds over those which are not.

The market has spoken.

Clearly all eyes on China over the next few days - this could turn out (in hindsight as usual) to be history being written.

May the Trend be with you!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG