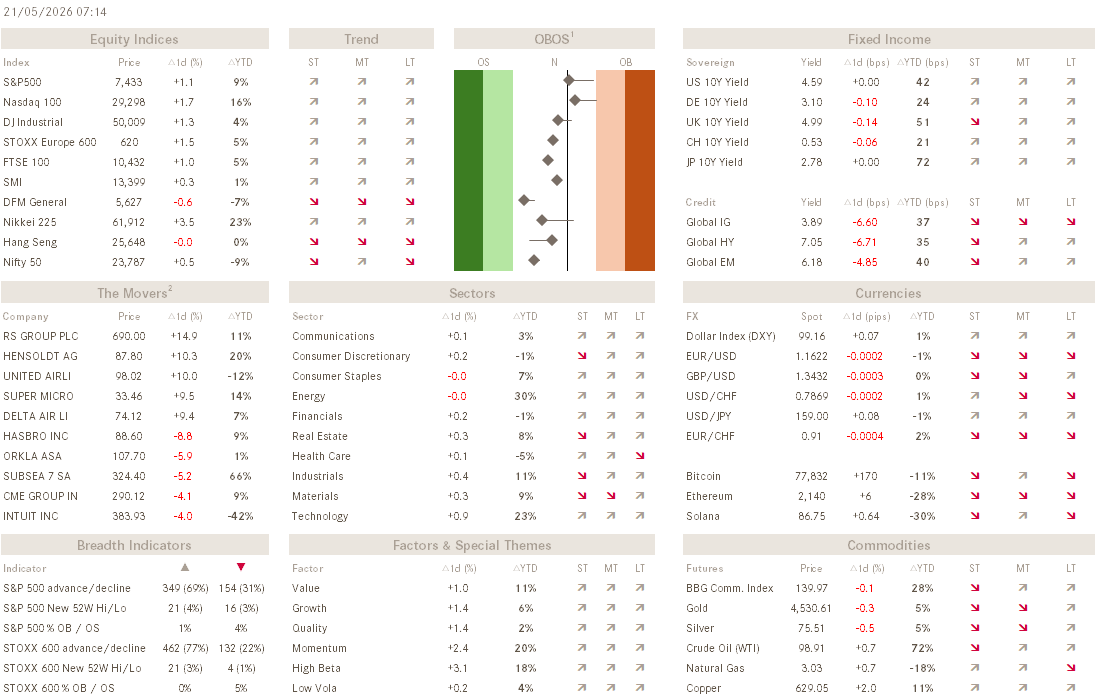

The Q - Daily Edition - Draft

The Envy of All

"It is not greed that drives the world, but envy."

— Charlie Munger

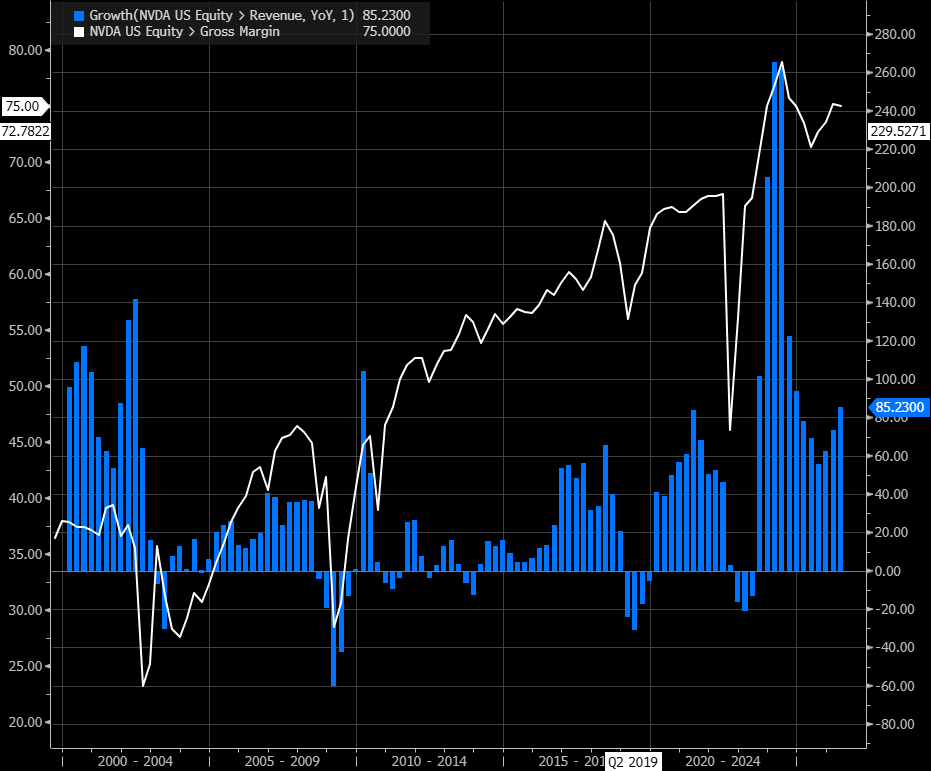

So, NVDA came, reported and sold off … a little bit. I guess it is tough to get too bearish on a company that reports an 85% year-on-year revenue growth (blue bars) and a 75% gross profit margin (white line),

despite still lofty valuations, expressed via for example a 20x price/to sales ratio (which admittedly has halved since the >40 levels two years ago):

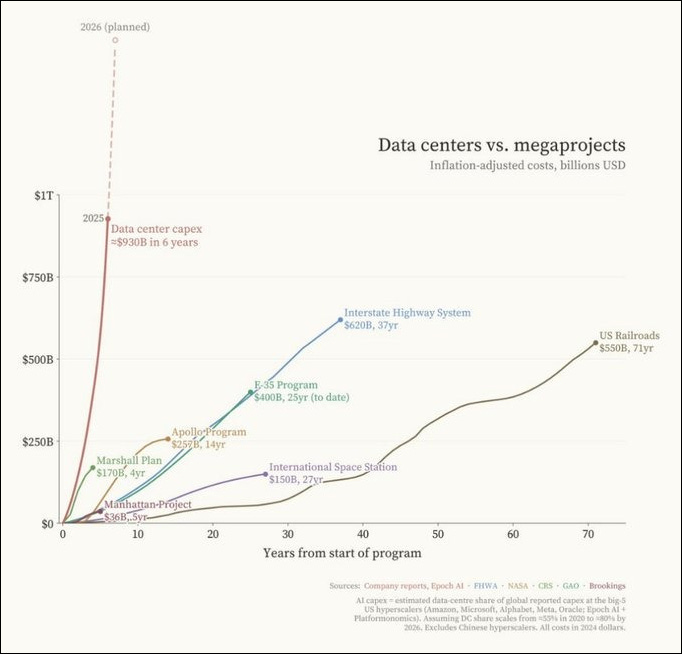

In any case, NVDA’s numbers should be good enough to confirm to the market that the AI infrastructure build-out is still in full swing and on par with some of humanities largest building projects:

I would even go as far as saying that the current AI infrastructure building boom is on par with the Roman Roads build-out some over 2000 years ago, but unfortunately data is slightly fuzzy back in that period 😉

Breadth in yesterday’s session was leaning strongly bullish (see dashboard) and the chart of the S&P 500 would visually suggest that the “correction” may be already over:

Even, let me repeat that, EVEN, European stocks are showing signs of life again, and the SXXP only needs a few basis points to become extremely constructive:

Probably also helpful to multi-asset portfolios yesterday was that bond yields started coming of their recent highs (US 10 Year Yield below),

which helped a strongly battered bond market (proxied via 20+ Year Treasury Bond ETF below):

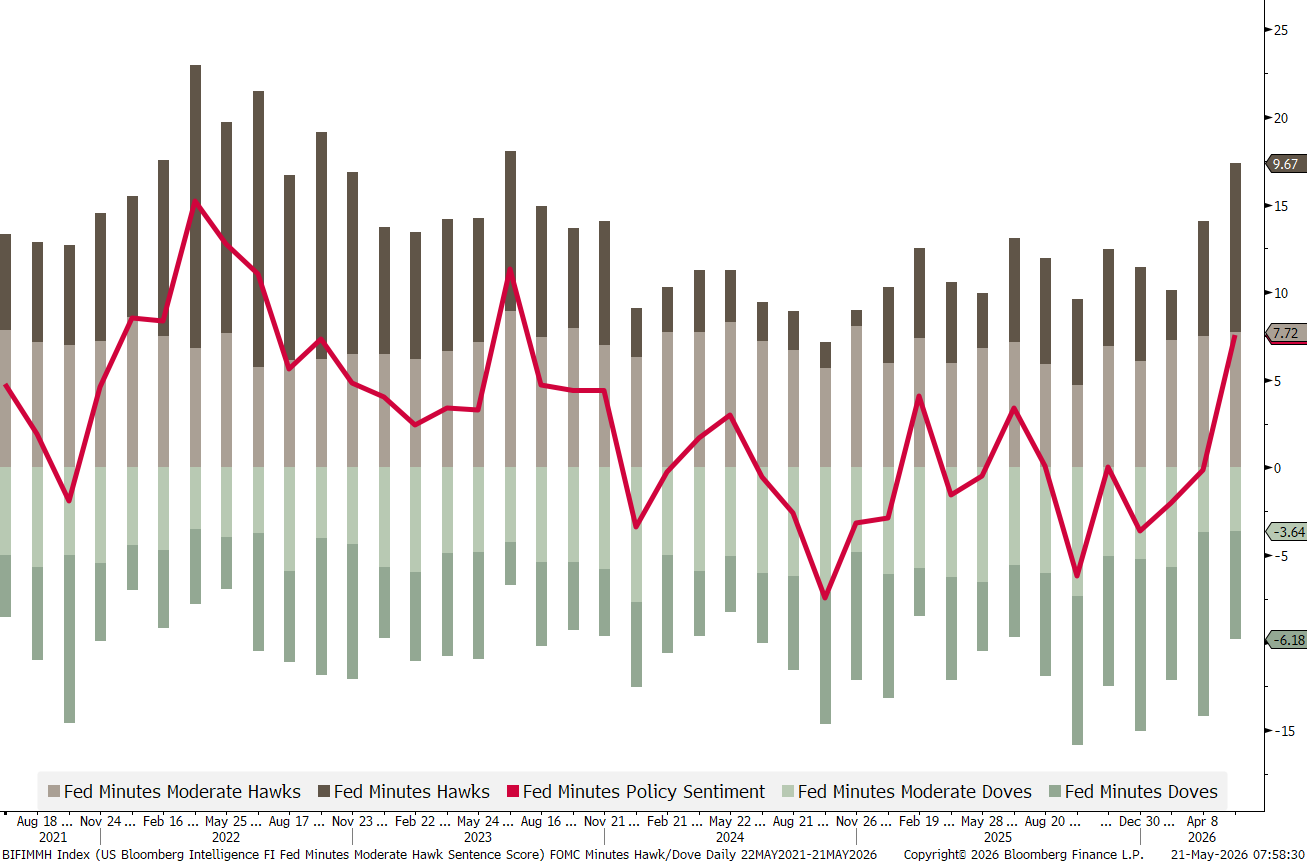

Funnily enough, it was probably a hawkish sounding Fed that brought bond yields lower, which brings us already to today’s chart of the day:

The Fed released minutes from their April 29th FOMC meeting yesterday, and as the chart below shows, the dovish (greenish) and hawkish (greyish) word counts in the sentences, leaned to the most hawkish interpretation (red line) since 2023.

This was well received by the bond vigilantes, which appreciated the fact that the Fed does NOT seem to let inflation get out of hand, in turn pushing bond yields lower.

US Initial Jobless Claims

US Philadelphia Fed Manufacturing Index

Global Flash PMIs (US / Eurozone / UK / Japan)

QuiCQ n’ dirty - This is the way!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG