The Q - Daily Edition

Be Careful What You Wish For

"There are only two tragedies in life: one is not getting what one wants, and the other is getting it."

— Oscar Wilde

And today’s winner in the category “Be careful what you wish for” is…. drumroll…. longer drumroll….. TADA!!

But with the US President’s vocal-expression-organ and his finger-tips-stuck-on-social-media-apps this was just one announcement communication post “thing” of many yesterday he felt compelled to share with the world yesterday.

For our purposed (making money) probably the immediately most important one came shortly after the market close:

How did the market react? Well, as with anything that becomes a routine, such as TACO TUESDAYS, the marginal propensity of eating yet another TACO on yet another TUESDAY diminished noticeably.

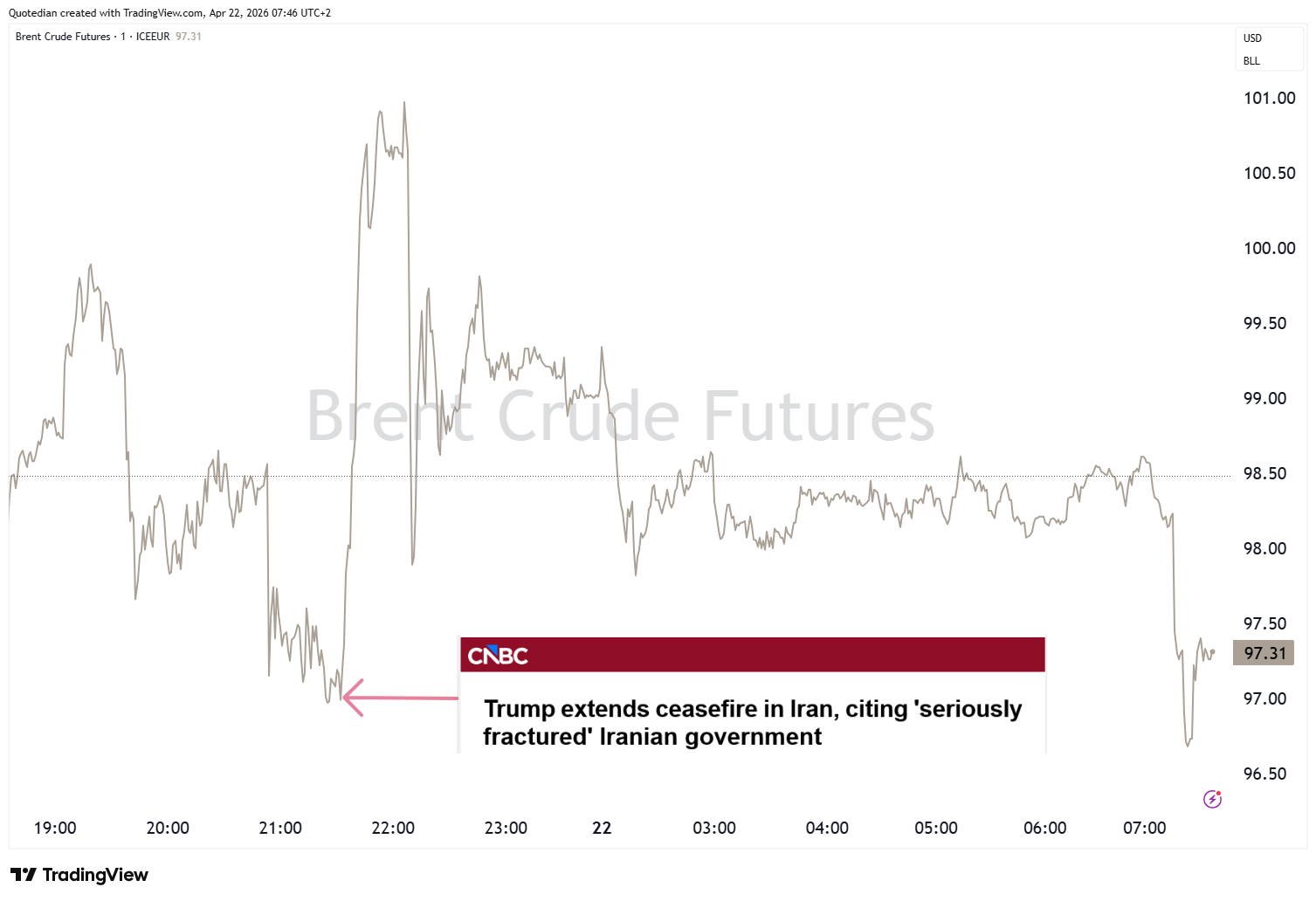

Oil prices, for example, did not go down on the announced ‘permanent ceasefire’, but rather up, showing investors’ main worry being a prolonged closure of the Strait of Hormuz (SoH):

Admittedly, prices have come down to where they were in the meantime, yet, the market knee-jerk reaction is still a tell sign.

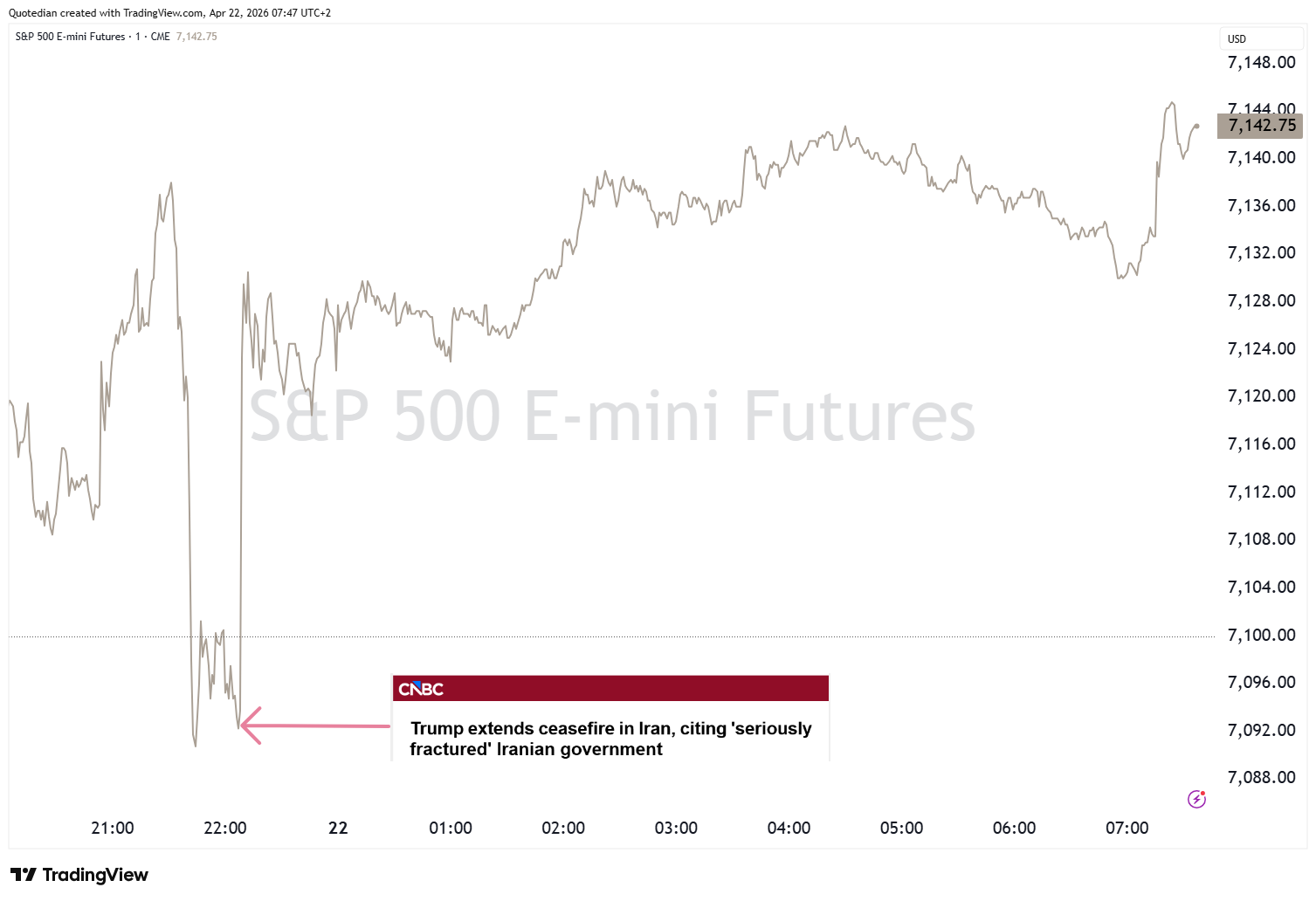

Equity markets did jump, but only about half a percentage point right back to where they started worrying about the original deadline approaching:

Zooming out to the daily chart, the S&P 500 can definitely do with a pause after the second fastest move from oversold (RSI <30) to overbought (RSI >70) since 1950, as we had shown in Monday’s weekly Quotedian (“The Spice Must Flow”):

Breadth (advancers/decliners) was about 1:2 on the S&P yesterday, though it is noticable that 28 stocks hit a new 52-week high versus only 4 sitting at new 52-week lows.

For European markets, the 52-Week Hi/Lo ratio was nearly identical even though the STOXX 600 was down nearly a percent:

In Asia, it looks like the Nikkei 225 may be able to close at a new ATH in a few minutes:

Though the broader TOPIX index (1650 stocks) may be signalling a warning with a negative divergence to the Nikkei:

Little to report on the currency and commodity front other than oil which we already covered, so let’s move right on into the next section.

You know I like to say “there’s always a bull market somewhere”, hence with major global benchmarks hardly making any net progress over the past six months, it is satisfying to know you could have been invested in US Micro Cap stocks, which are up 85% over the past 12-months,

beating their mega/large-cap cousins by a wide margin:

Or, there has also been a bull market of note in Chinese ‘venture enterprises, with the ChiNext Index doubling over the past year:

That’s good and nice, you will say, but what is this knowledge worth if you cannot invest into these areas, right? Wrong!

Choose the iShares Microcap ETF (IWC) for US micro cap or the VanEck ChiNext ETF (CNXT) for the Chinese venture stocks.

De nada.

Quiet day ahead in terms of economic data, was nothing meaningful being reported out of the US.

CPI, PPI and RPI have already been reported in the UK a few minutes ago, generally ‘surprising’ to the upside.

Busy on the earnings front though, with ABB, Boeing, GE Vernova, Vertiv, AT&T, ServiceNow, IBM, Kinder Morgan, Lam Research, Tesla and Texas Instruments only a tight selection of a much wider area of names reporting today.

And to finish, we have another winner today, this time in the category “WTF”:

Oh, wait, same guy again …

May the Trend Be With You!!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG