The Q - Daily Edition

Countdown

"The first ten million years were the worst. And the second ten million... they were the worst too. The third ten million I didn't enjoy at all. After that, I went into a bit of a decline."

— Marvin, in Douglas Adams’s Hitchhikers Guide to the Galaxy

Markets seem a bit rudderless at the moment, slave to the next Presidential post on social media, which then minutes later is denied by the Iranian regime that according to the next presidential social post does not exist anymore …

Yesterday, Iran rejected the US-proposed 15-point plan, instead laying out its own conditions in a 5-point plan;

(1) halt the killing of Iranian officials;

(2) means to make sure no other war is wage against it;

(3) reparations for the war;

(4) an end to all hostilities;

(5) Iran’s “exercise of sovereignty over the Strait of Hormuz.”

The probability that Washington would accept these terms in exchange for a ceasefire is roughly equal to the likelihood that Tehran would have accepted the original US proposal…zero. Even though, interestingly enough, Iran didn't claim a right to nuclear enrichment or ballistic missiles.

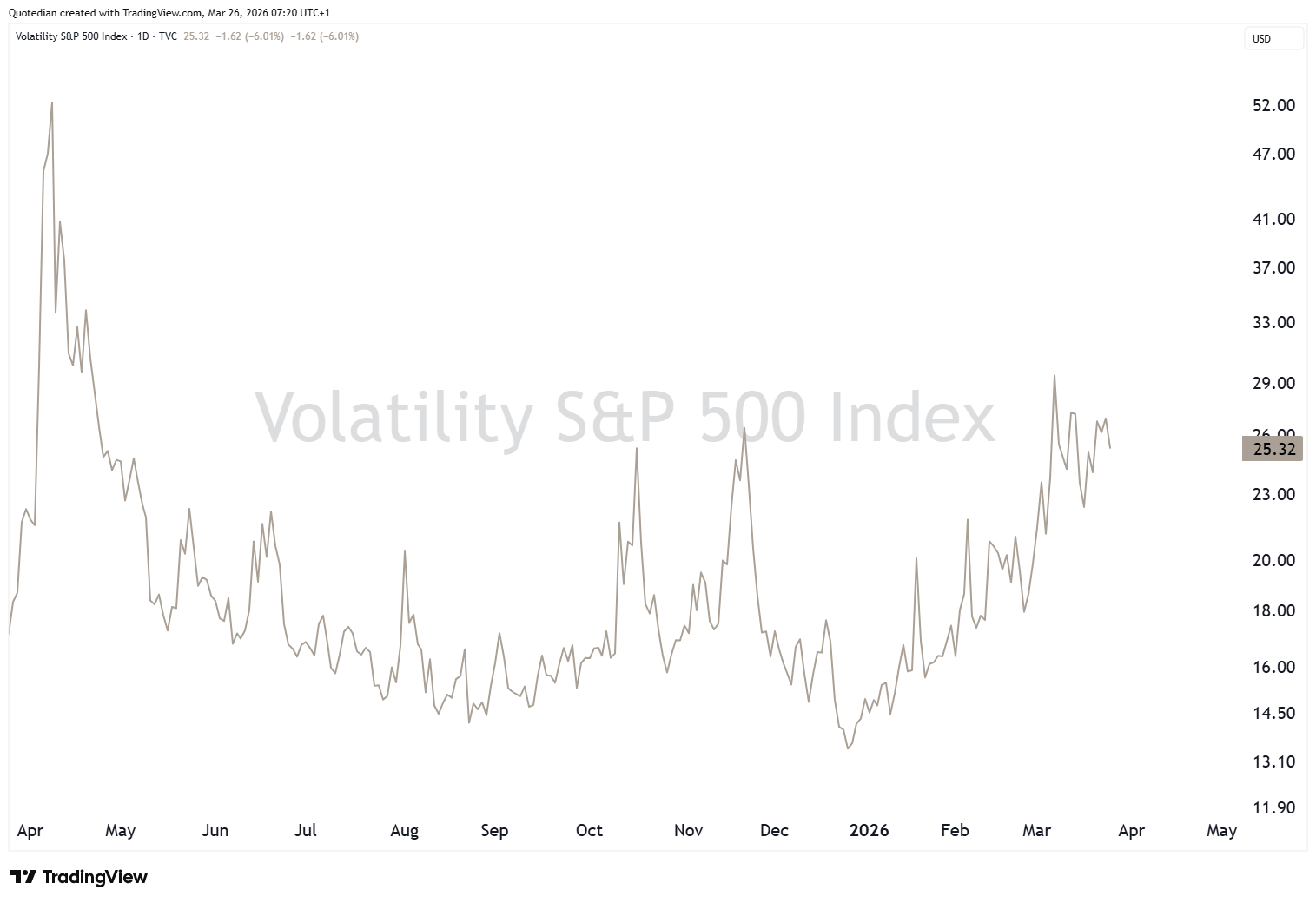

Given the back-and-forth, it is no wonder that volatility in equities,

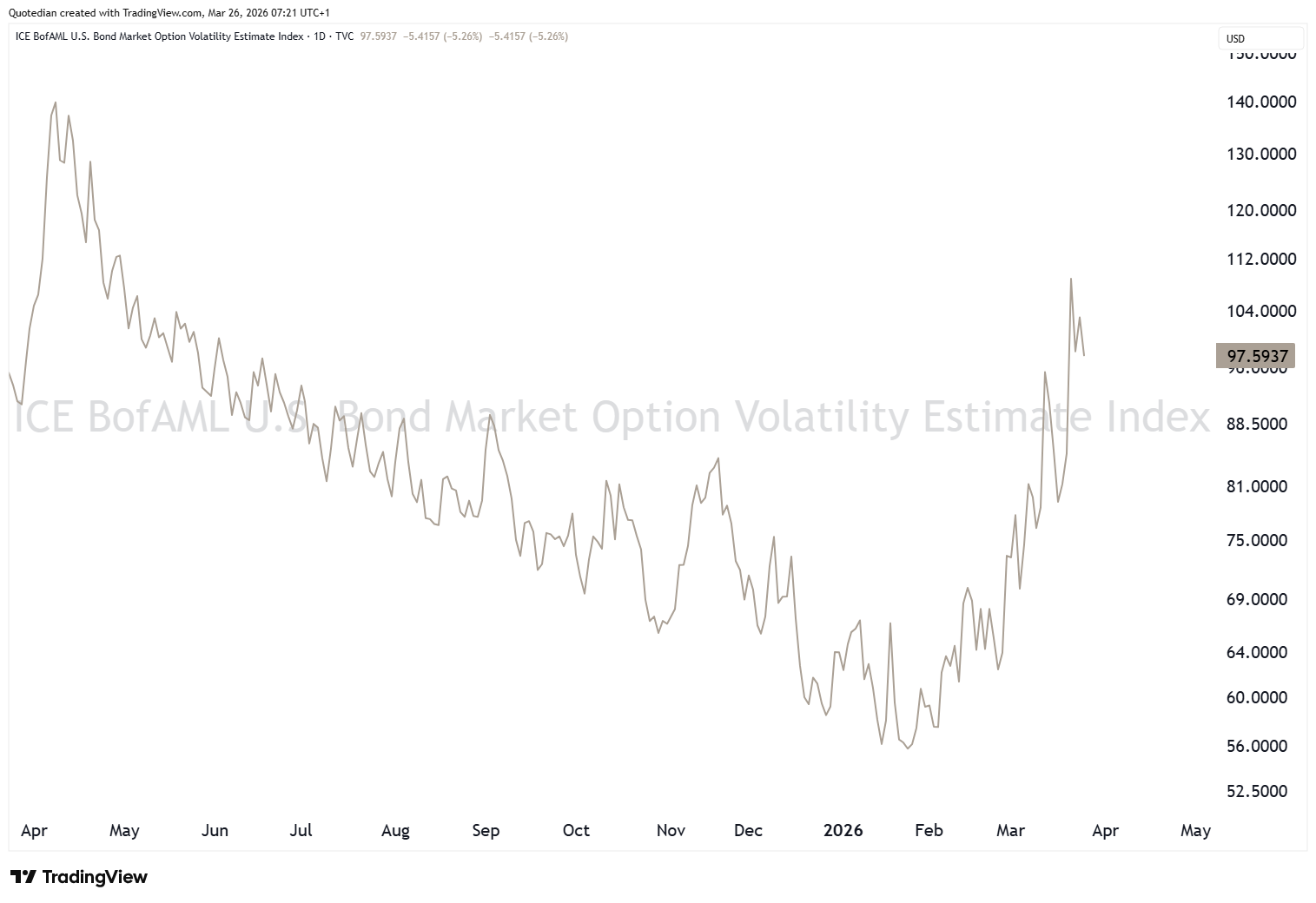

AND bonds,

remains elevated.

And here we are ticking towards Trump’s self-imposed 5-day five deadline, with volatility elevated as just seen, but still some eerie relative calm.

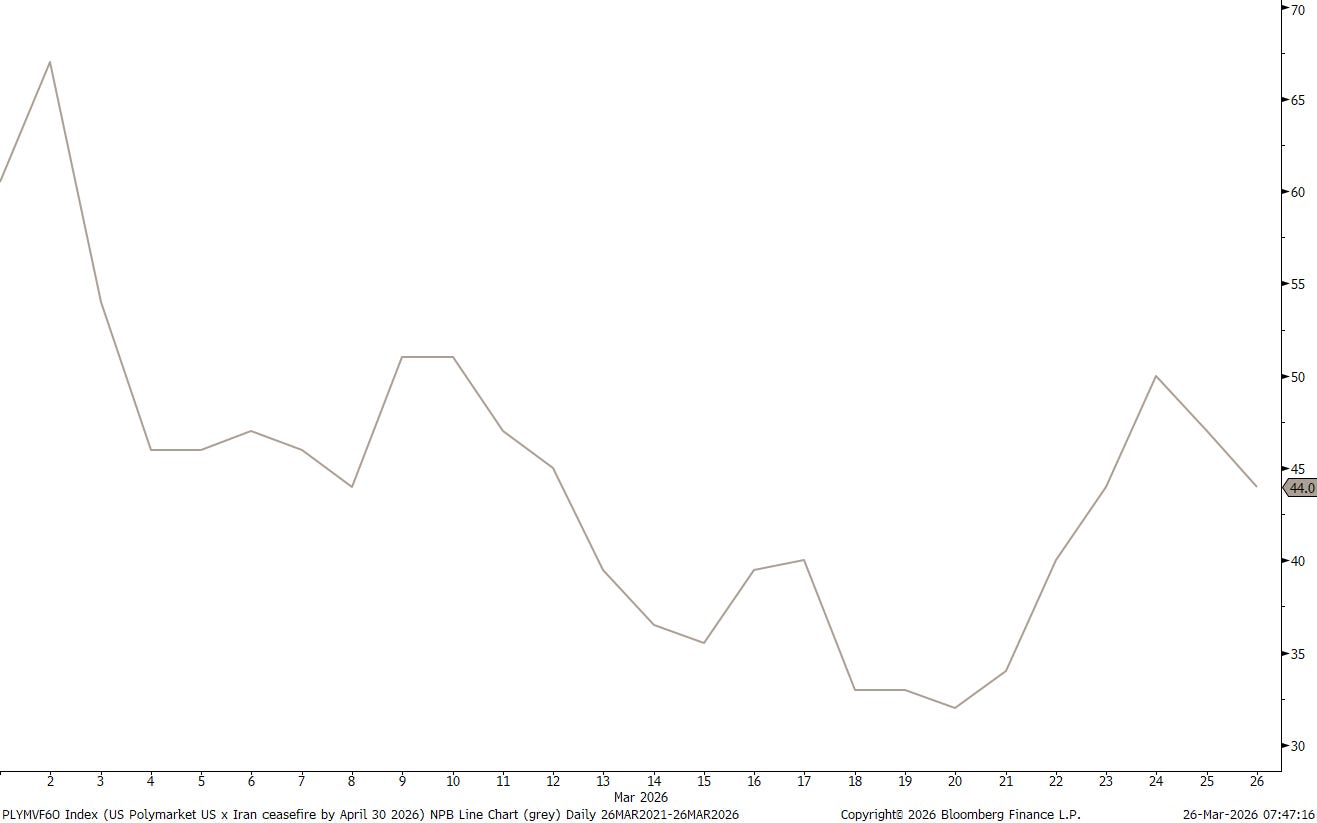

Maybe the Polymarket bet on a US x Iran ceasefire by April 30th at close to 50-50 is a tell sign for investors’ indecisiveness:

The S&P 500 continues to trade within its ‘box’, we have been observing for a while now, but notably has yesterday also been rejected at its 200-day MA yesterday:

Maybe we are in for a forming of the right shoulder in a classical shoulder-head-shoulder pattern?

A bit too early to speculate on that…

European stocks rebounded ‘better’ the first three sessions of this week, but of course had also been beaten down substantial more than their US cousins

BUT, but, but, of note and to be held in high honour of European equity markets, is the SXXP still trading above its 200-day MA!

Meanwhile, Asian markets are trading mostly softer this morning, lead by the Chinese (HK & Mainland) equity complex. Though all eyes on India, where markets are closed today, as news reports of panic gasoline buying are in crescendo:

The trouble here: Whilst there is no burning tyres in the streets (yet), there is a perception crisis layered on top of a very real supply vulnerability. The self-fulfilling prophecy dynamic — panic creates the very shortage people feared — is textbook commodity behavioural economics. Let’s stay tuned on this one …

In bond markets, US Treasury yields have relaxed a tad from their Monday and Tuesday panic peaks, which is a first good news for equity markets too:

However, we are still only a few pips away from a new cycle closing high …

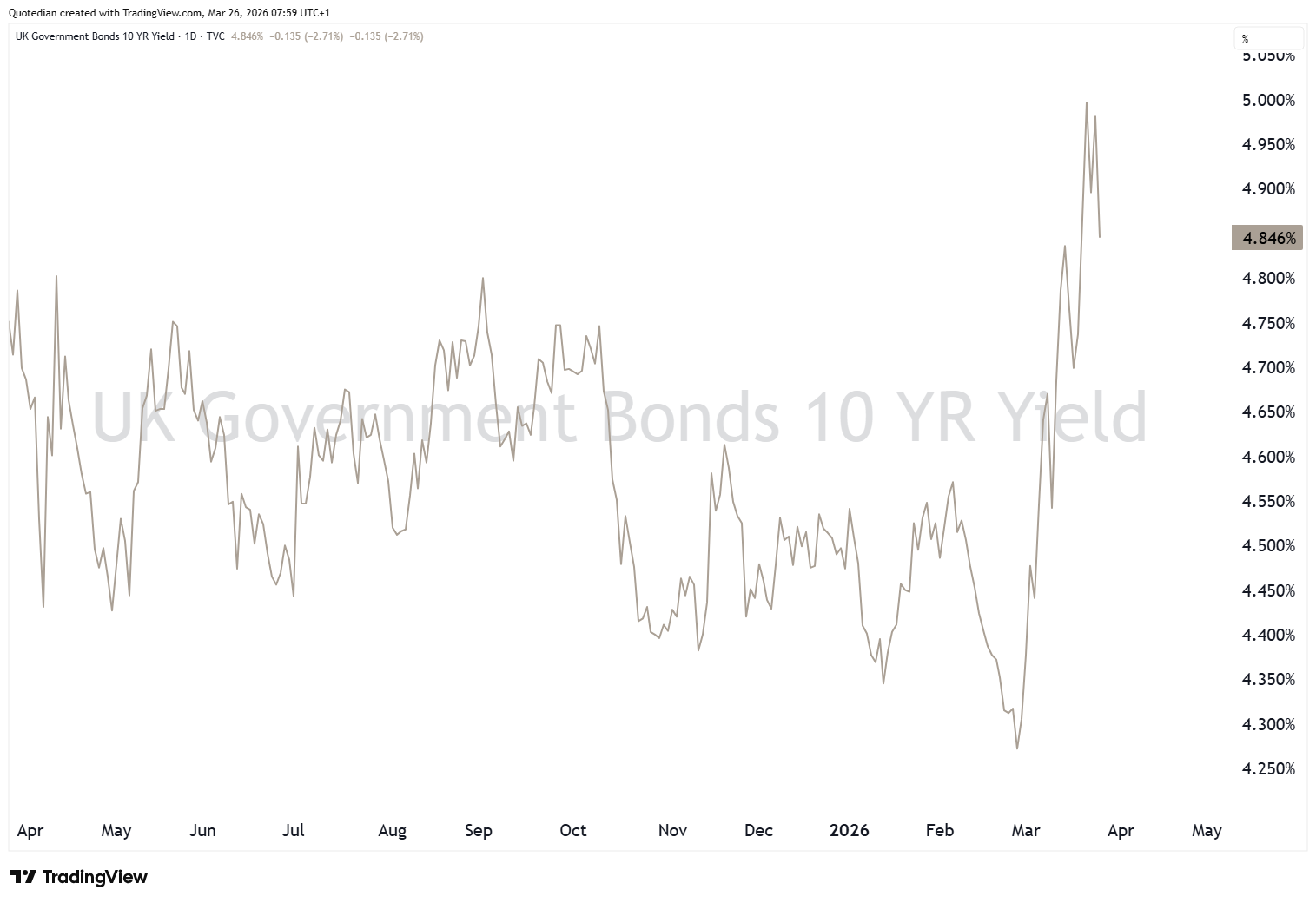

But an even louder sigh of relieve can heard from the (should I say: current?) UK government, which was on the brink of yet another Truss-moment at the beginning of the week:

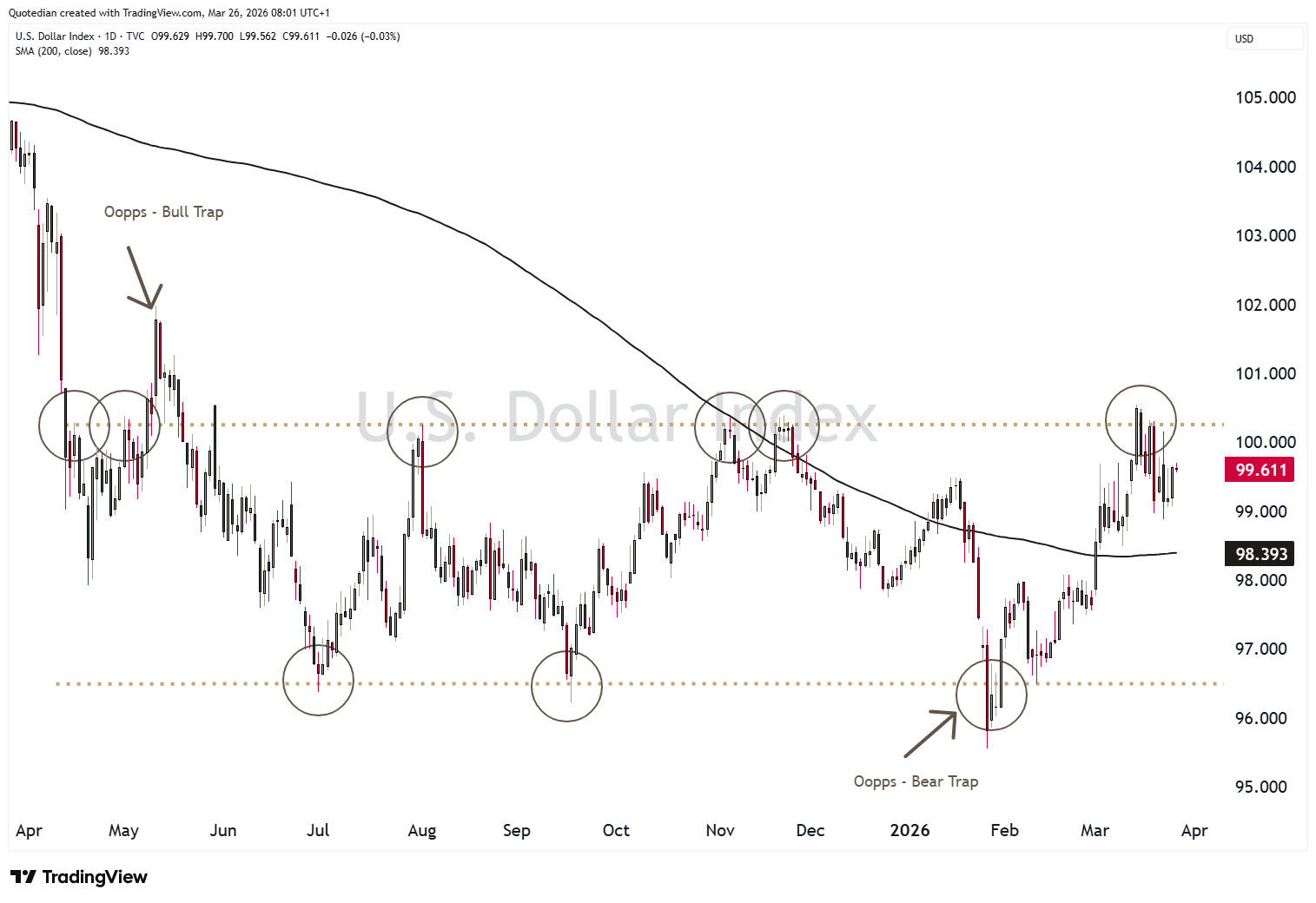

The US Dollar remains range stuck and I insist, given the depth of the geopolitical crisis, the lack of additional strength is disappointing:

Oil (Brent below) is obviously a broken chart, not only due to the impact from the news flow described further up, but probably also due to market manipulation, where of rumours have increased noticeably over the past week or so.

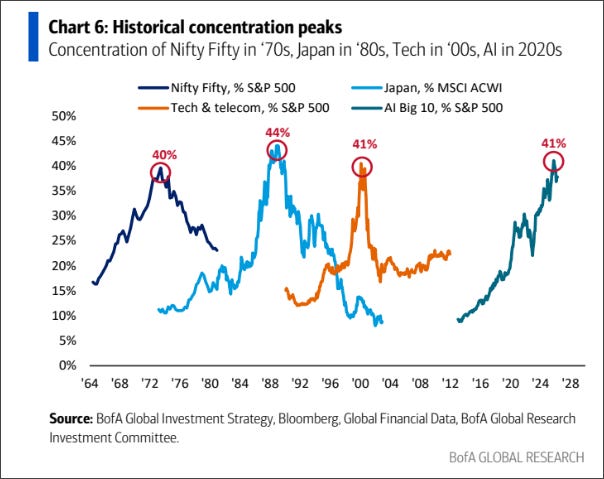

Good chart below from the fine folks at BofA. It compares the current concentration of the 10 largest AI-involved stocks to previous famous notorious concentration peaks.

As Trump’s five-day deadline approaches (due tomorrow) anything can really happen over the next hours. Betting markets see split chances for an off-ramp on either side of the conflict, but equity markets are trying to move higher. They may achieve a relieve rally, but longer-term damage has likely been done and will be a headwind over the coming months.

ECONOMIC DATA

US Initial Jobless Claims — 13:30 CET. Exp. 211K vs 205K prior. 4-wk avg 210.75K.

US Continuing Claims — 13:30 CET. Prior 1,857K. Proxy for outstanding unemployment; uptick last week.

EIA Natural Gas Storage — 14:30 CET. Exp. -49Bcf vs +35Bcf prior. Massive swing on Hormuz LNG disruption.

CENTRAL BANKS & SPEAKERS

ECB — Lagarde keynote — 09:45 CET. “The ECB and Its Watchers” Conference, Frankfurt. Oil-vs-growth framing is the signal.

No scheduled Fed speakers today. Next FOMC: 5–6 May.

AUCTIONS

US 4-Week Bill — 15:30 CET. Prior yield 3.615%.

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG