QuiCQ 29/05/2024

Waiting for Godot

QuiCQ poll instead of the usual PDF-file for download in this space:

“The test of success is not what you do when you are on top. Success is how high you bounce when you hit the bottom”

— General Geroge S. Patton

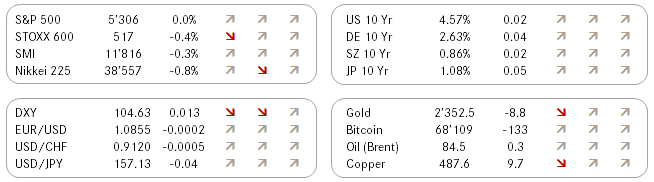

We all have heard how undervalued the Japanese Yen is (and has been for a while now). By measure of Purchasing Power Parity (PPP), via the Big Mac-Method for example, the JPY is 48% undervalued versus the US Dollar:

However, in currencies, even worse than for stock markets, valuations are NOT a timing tool, i.e. valuations do not matter until they do.

However, the rubber band might be getting a bit overstretched as Japanese yields have finally started rising (see JGB 10year yield in in-set graph below). This means, that the spread between US 10 year yields and Japanese 10-year yields (red line) has been contracting and at the same time diverging (black arrow) from the previously high correlation to the USD/JPY (grey line) cross rate. How much longer?