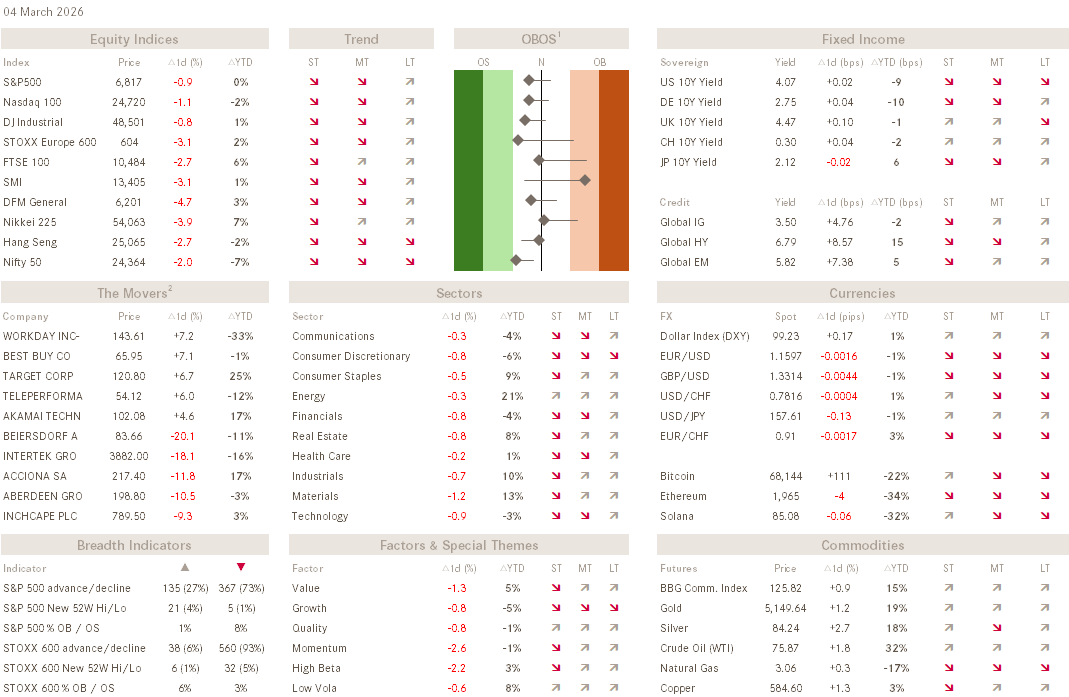

The Q - Daily Edition

04/03/2026

Good Morning,

Today, you get to vote for your own favourite Quote, which is in reference to today’s Chart-of-the-Day (COTD, see below). The choices are:

There is always a bull market somewhere

and

Never let a good crisis go to waste

Realisation started settling in on the second trading day since the Iran war started, that this may not be over in 72 hours.

Accordingly, stock markets around the globe continued to sell-off:

But not all markets are being treated equally…. Europe (SXXP) is being hit hard on increasing energy costs,

whilst the US (S&P 500), which is largely energy self-sufficient, has seen a much smaller fall-out:

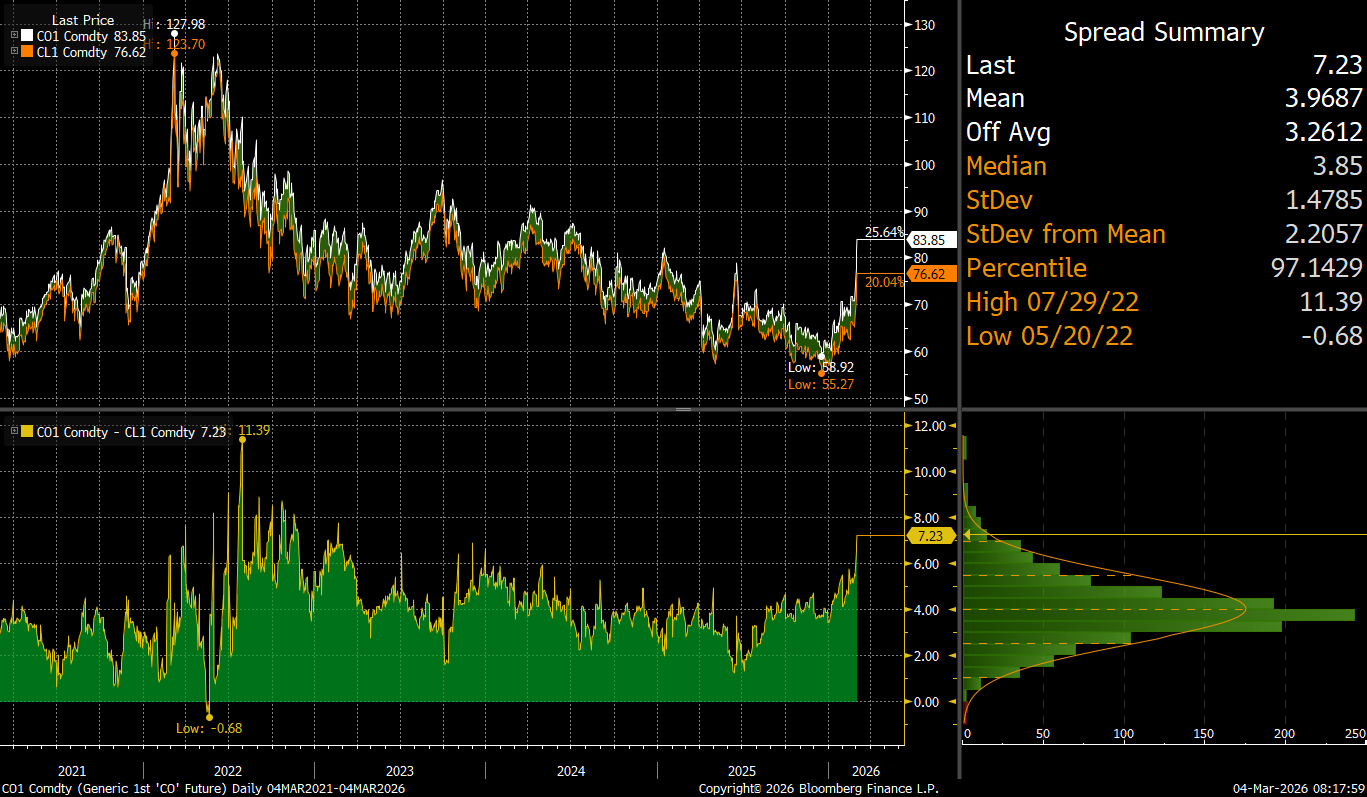

This energy-cost difference is not least seen in that widening Brent-WTI spread (lower clip) I already touched upon in the weekly Quotedian issued last Monday (click here):

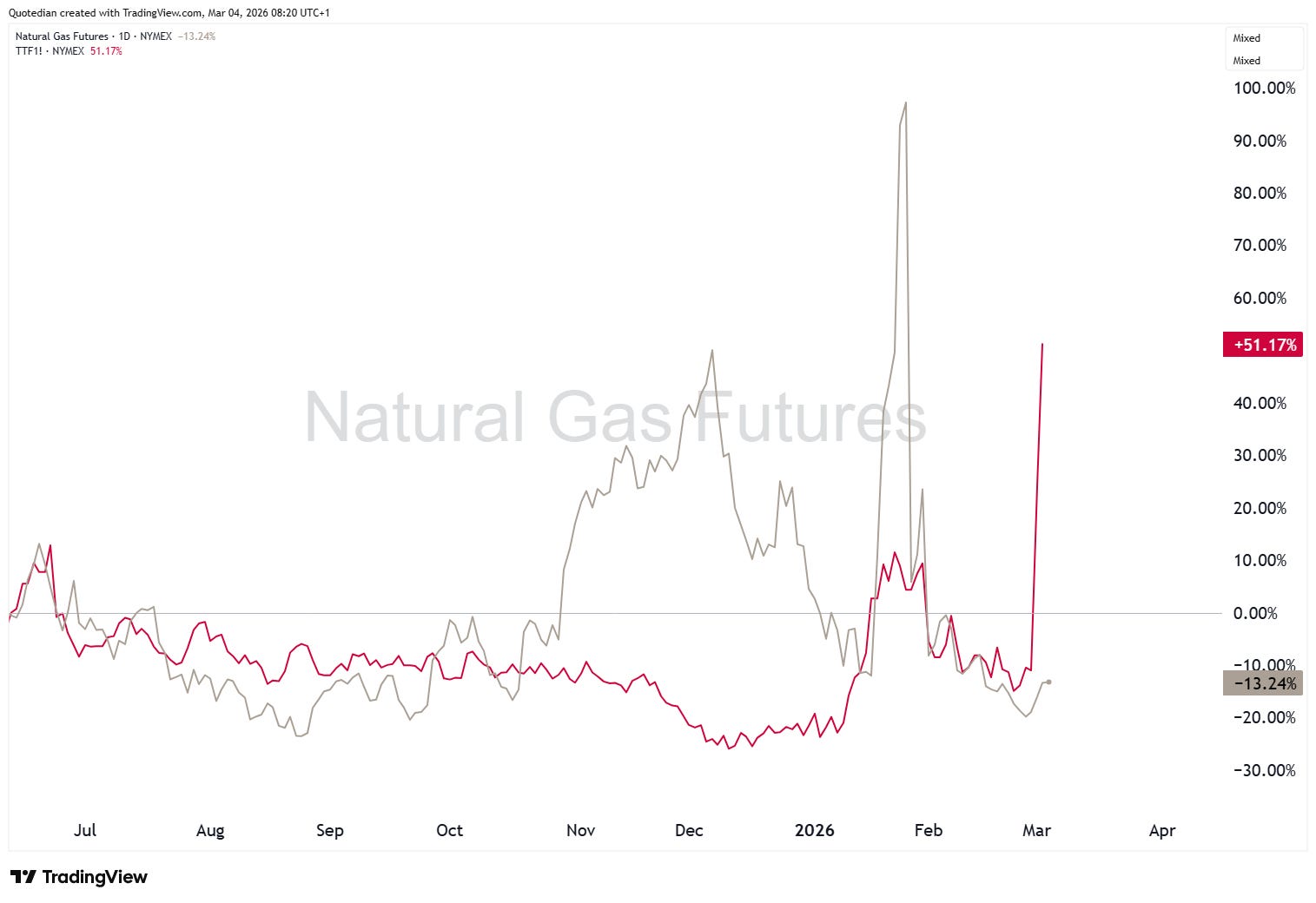

Even more visible is that energy-cost at the natural gas price level, where Dutch NG has exploded higher whilst the Henry Hub version (US) is keeping its calm:

Crude oil prices exploded higher yesterday, until assurance from President Trump that they will escort ships through the Strait of Hormuz gave short-term relief to price pressures. HOWEVER, this morning the market seems to remember that a handful of terrorists (or liberation fighters, pick your definition) in flip-flops where able to keep the Strait closed for a prolonged period of time. Imagine what the IRGC (Islamic Revolutionary Guard Corps) could do with a couple of rockets and drones. Hence, the oil price is shooting higher this morning:

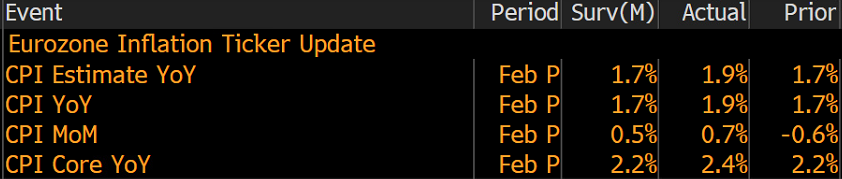

As were the demise and prospect of higher energy prices not already enough in Europe, we also got inflation readings which were above expectations … and this before the impact of fore-mentioned energy prices:

Whilst Headline inflation at 1.9% is still below the ECB’s two percent target, the Core reading ticked in at 2.4%.

The impact on European yields, below proxied via the German 10-year Bund was immediate:

I fear that the bond market riots may only be in its early innings, especially if I am right about the impact of possible likely nearly-guaranteed supply chain disruptions…

May the Trend be with You!

Today:

🇨🇭 Switzerland CPI (Feb) — next update due today; Jan was +0.1% YoY, barely above zero. Key for SNB rate path

🇪🇺 Eurozone Unemployment (Jan) + Italy GDP (Q4, final)

🇺🇸 ADP Employment Change (Feb) — 8:15am ET, cons. 49K vs prior 22K; first NFP preview

🇺🇸 ISM Services PMI (Feb) — 10:00am ET, cons. 53.5 vs 53.8; watch Employment sub-index for payrolls clues

🇺🇸 Fed Beige Book — 2:00pm ET; qualitative read on hiring, tariffs, business sentiment ahead of March 18-19 FOMC

🇺🇸 Broadcom (AVGO) earnings AMC — EPS est. $1.88; AI infrastructure bellwether, last quarter beat by 13%

🇺🇸 Also reporting: Abercrombie & Fitch (ANF), Bath & Body Works (BBWI), Veeva Systems (VEEV), Wix (WIX) (BMO)

Separately, in China the 15th 5-year plan is in ‘discussion’ (simplified):

🇨🇳 China “Two Sessions” (Mar 4-11):

China’s annual parliamentary meetings open today, but this year’s edition is special: the 15th Five-Year Plan (2026-2030) will be formally unveiled — Beijing’s economic roadmap for the next half-decade

Premier Li Qiang delivers the Government Work Report tomorrow (Mar 5) — watch for the GDP growth target (likely lowered to ~4.5-5%) and fiscal spending plans

Key themes: tech self-sufficiency (AI, quantum, 6G), boosting domestic consumption, and navigating US-China trade friction

First FYP launch since 2021 — historically a strong signal for which sectors get policy support (and capital) for years to come

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG